Value Investor: Three stocks with a silver lining

With the current media coverage of the Medibank Private float and Japara Healthcare's strong ASX debut in April, it is clear companies that benefit from Australia's ageing population are attractive to investors. However, buying a theme is dangerous if due regard to underlying value is ignored.

We examine three stocks that should benefit from the ageing population.

Fleetwood Corporation (ASX: FWD), a provider of caravans and portable accommodation, should benefit from the trend for grey nomads to buy the company's caravans and set off around Australia on the Big Trip.

However in recent times, its businesses have struggled.

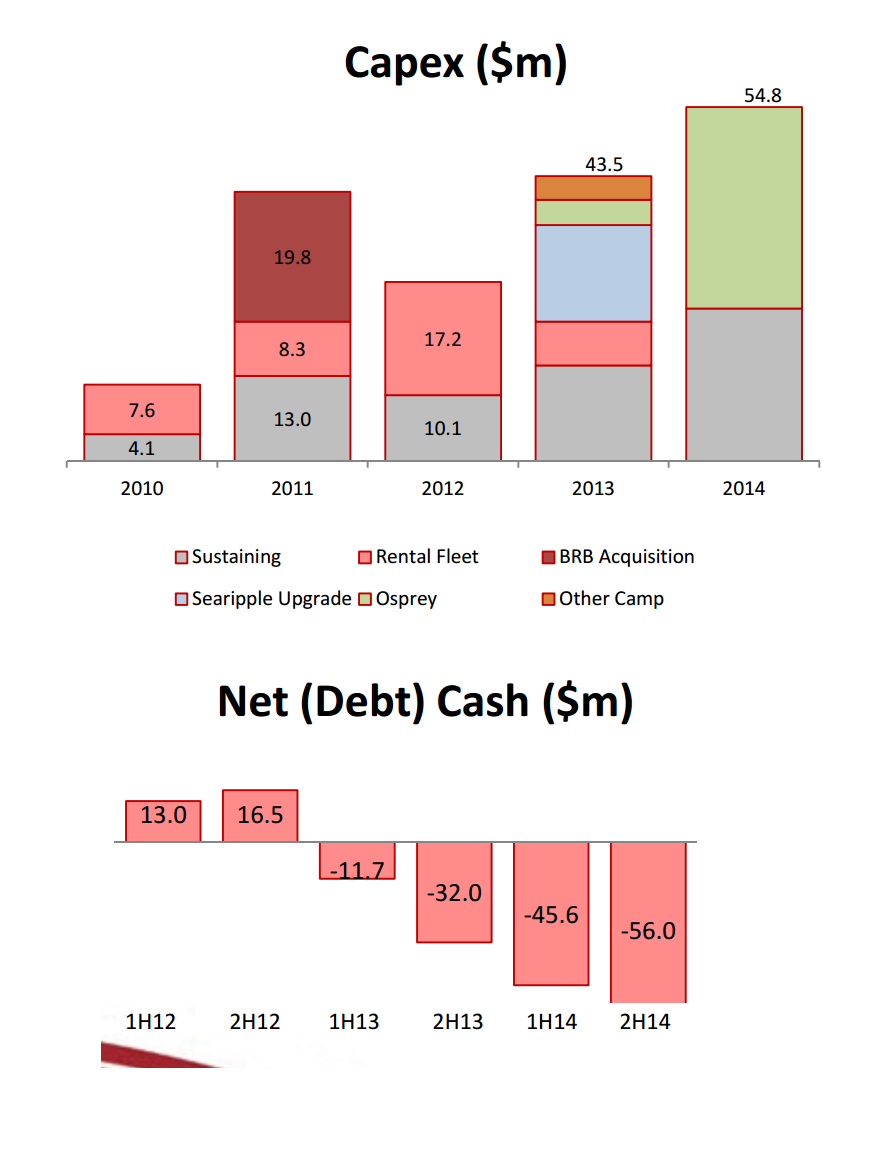

Fleetwood's accommodation business is suffering due to soft trading conditions in resources. The Karratha market appears to remain in a state of oversupply, with its Searipple Village dropping to a low of 40 per cent occupancy over the year.

The expansion at Gladstone, aimed at workers on local LNG projects, remains on hold as the reduction in demand has also impacted room rates.

Meanwhile, demand for recreational vehicles remain subdued due to poor consumer sentiment.

In the recent fiscal 2014 result, Fleetwood experienced strengthening demand from the education sector, which contributed to 10 per cent revenue growth. However, earnings margins were crunched, contracting from 7.3 to 1.5 per cent.

Management is restructuring its caravan production business, such as broadening supply from Asia to reduce costs and improve margins.

Fleetwood has increased capital expenditure on construction in recent years, with 2014 particularly dominated by Osprey, a government project for a WA accommodation village for service workers at Port Hedland.

However, this has been funded by increased debt levels (see below).

Figure 1 – Fleetwood Capex and Net Debt Levels

Source: Fleetwood

We adopt a forecast sustainable return on equity of 10 per cent and a high required return of 15.5 per cent given the rising gearing. We derive a fiscal 2014 valuation of $1.88. Fleetwood is trading below its intrinsic value.

Primary Health Care (ASX: PRY), a medical centre operator with pathology, diagnostic imaging and health technology services, is in a solid position to benefit from increasing demand for medical services from an older population.

Primary's strategy relies on organic growth, supported by margin gains afforded by economies of scale. This is assisted by strong cost controls and operating efficiencies.

This drove a solid fiscal 2014 result, with net profit after tax rising 8.3 per cent to $163 million. Earnings from pathology and imaging rose around 6 per cent while the core medical centres business ticked over at 4 per cent.

The proposed $7 Medicare co-payment may affect earnings, with possible reductions in demand for pathology and medical centre services. This highlights Primary's exposure to regulatory risk.

We adopt a forecast sustainable return on equity of 9 per cent and a required return of 12 per cent to derive a fiscal 2014 valuation of $3.73. Primary is currently trading above valuation.

Also leveraged to increasing medical expenditure is Ramsay Health Care (ASX: RHC), the largest operator of private hospitals in Australia.

Ramsay Health Care should benefit from increasing private health insurance membership, driven by government initiatives designed to decrease the burden on public finances, such as the Medicare levy and the private health insurance rebate.

It delivered yet another strong financial result for fiscal 2014, with net profit after tax from Ramsay Health Care's core business up 19 per cent to $346.2m, with solid revenue growth of 17.6 per cent. Also positive was earnings margins expanding 20 basis points to 11.8 per cent.

The recent acquisition of Generale de Sante SA will make Ramsay Health Care the largest private hospital operator in France. Ramsay Health Care has also successfully brought its business model to the UK, Indonesia and Malaysia.

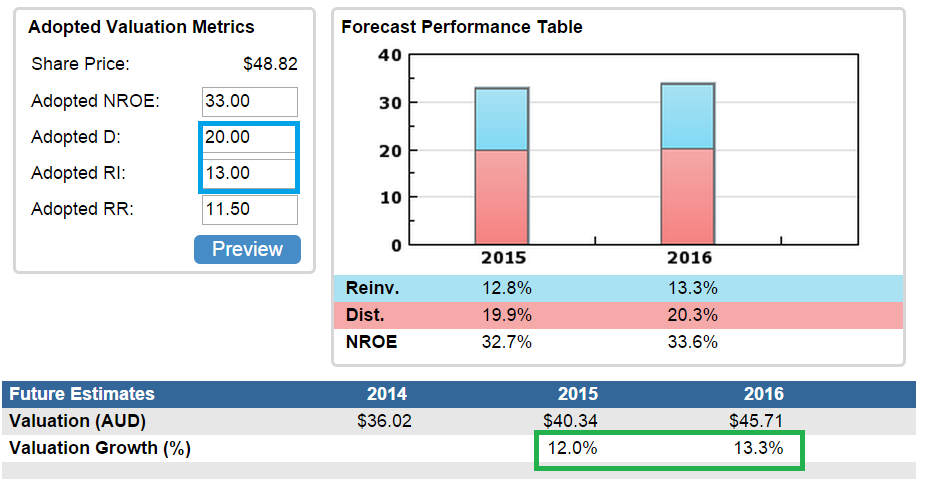

From RHC we expect consistently high profitability, with return on equity averaging 25 per cent in the last five years.

We adopt a forecast return on equity of 33 per cent and a low required return of 11.5 per cent, reflecting its quality and track record.

The reinvestment rate combined with strong return on equity allows Ramsay Health Care to compound intrinsic value at double digits (green).

Figure 2 – RHC Future Valuation

Source: StocksInValue

With a fiscal 2014 valuation of $36, Ramsay Health Care is trading significantly above value, even after the recent market correction. This reflects the record of solid financial performance and the eagerness of investors to ride the ageing population trend.

By Brian Soh, Equities Analyst, with insights from John Abernethy of Clime Asset Management. StocksInValue provides valuations and quality ratings of 400 ASX-listed companies and equities research, insights and macro strategy. For a no obligation FREE trial, please visit StocksInValue.com.au or call 1300 136 225.