Value Investor: Newcrest is not so golden

Newcrest Mining (ASX:NCM) is the ASX's largest goldminer and one of the world's largest by market capitalisation and gold reserves. Unfortunately it not only has a particularly poor record of operational problems and production downgrades but is also controversial.

The ‘first strike' against the remuneration report at the recent AGM occurred after shareholders protested at chief executive Sandeep Biswas' base salary, which is larger than that of the chief executives of BHP Billiton and Rio Tinto. It was a sign the board does not understand the expectations of shareholders.

Newcrest was also recently fined $1.2 million for a breach of the disclosure provisions of the Corporations Act and currently faces a class action by shareholders disgruntled by the ASX announcement of June 7, 2013, when Newcrest:

- Downgraded its fiscal 2014 gold production forecast

- Wrote off all $3.8 billion of goodwill on its balance sheet

- Impaired the book value of its mining operations by $2.2bn

- Said it would not pay a final dividend for fiscal 2013.

A disaster!

Similarly, Newcrest's record of financial underperformance does not inspire confidence.

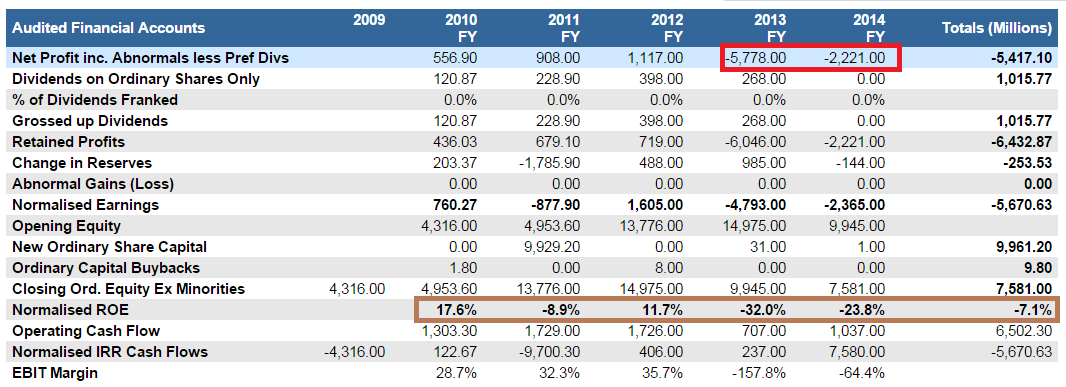

Source: StocksInValue

Return on equity has been positive in only two of the last five years (brown box above). Asset writedowns and restructuring costs (after tax) of $6.2bn and $2.7bn in the last two years caused losses (red), and no dividends were paid in the last financial year.

New chief executive Sandeep Biswas started in July. Can he turn Newcrest around?

Newcrest's key assets are Cadia and Lihir, two of the world's 10 largest known gold deposits. This gives Newcrest a long reserve life relative to peers and should be a competitive advantage.

There is no doubt Cadia is a world-class asset. Its all-in sustaining cost for the most recent quarter was $207/oz. With the gold price above $1,100/oz, we can see the significant cash generation potential of this asset, with room for production growth and further cost reduction.

In contrast, Lihir's production performance has disappointed, largely reflecting its technically difficult location and mismanagement of risks and problems.

Lihir has been in production for 17 years and is still problematic, implying the problems are semi-permanent. There are no easy fixes.

While there was improvement in total gold production (up 14 per cent) and cost reduction (down 24 per cent) in fiscal 2014, our take is that substantial uncertainty remains around Lihir's future volumes, costs and cashflows. Management is vague on the timing of and steps towards improvement. Further capital investment could be required.

This brings our attention to the higher than desirable debt levels (for a goldminer) with net debt to equity at 52 per cent. Should the volatile, unpredictable gold price fall precipitously, this might see Newcrest resort to a dilutive equity raising.

Gearing has trended higher due to the conjunction of fluctuating operating cashflows, reflecting the lower gold price and poor production performance, with major investment (over $4 bn) in Cadia East and the Lihir processing plant.

Both investments are now largely complete and should become free cashflow generators. Newcrest turned free cashflow-positive in fiscal 2014 for the first time in three years.

The intention is to use free cashflows to retire debt and eventually return to paying dividends. Newcrest repaid $US100m of debt on schedule in the September quarter, with the gold price at US$1,200/oz.

Newcrest can cover upcoming debt repayments scheduled over the next few years as long as the gold price remains above this level. At the time of writing, the price had fallen to US$1,195 on the strength of the US dollar.

Historically, there has been a fairly strong correlation between the US dollar and gold prices, though it is not perfect and there have been periods when both have rallied.

The safest course is to understand it will be harder for gold to rally in a world of US dollar strength, and Newcrest is at risk of an equity raising if the gold price keeps falling. Increased gearing and a writedown of Lihir's book value could also occur.

Ultimately, Newcrest remains mainly a play on the gold price and, therefore, a cyclical or speculative trade only. To own the stock, you need to be bullish on the gold price.

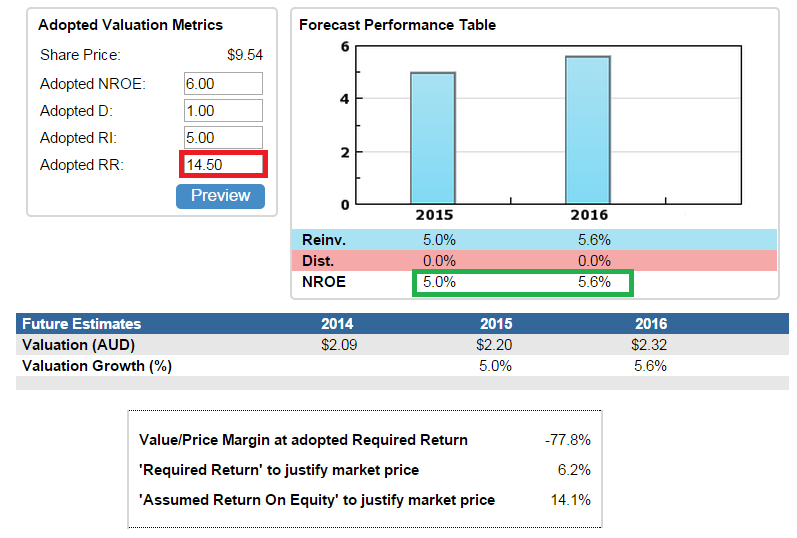

We adopt a moderate required return of 14.5 per cent (red below), reflecting operational uncertainty and gearing levels. We would need to see progress on debt reduction in outstanding debts to adopt a lower RR.

Figure 2 – Newcrest's Future Valuation

Source: StocksInValue

Our forecast sustainable return on equity of 6 per cent is marginally above consensus (green) and still we can only justify a $2.20 valuation -- dollars below the share price. We could adopt a ROE of up to 14 per cent, which is way above sustainable profitability, and Newcrest would still be overvalued.

Everything needs to go right for Newcrest -- gold price, currency, production and costs -- just to justify the current share price. On the probabilities, it looks seriously overvalued.

By Brian Soh and David Walker, Equities Analysts. StocksInValue provides valuations and quality ratings of 400 ASX-listed companies and equities research, insights and macro strategy. For a no obligation FREE trial, please visit StocksInValue.com.au or call 1300 136 225.