Two forces that are guiding markets

Two events caught my attention this week because they help explain the forces we are going to see in the market during coming months.

The first concerned BHP. The Big Australian produced an operating profit that was a little below expectations and, of course, it had to write down of the capital value of its US tax losses because of President Trump's reduced corporate tax rates. But when I first looked at the result I thought it wasn't too bad because the forces that pushed the operating profit down were in fact measures that would assist in future profits, including major works at Olympic Dam and extensions at Chile copper.

Moreover, the company repeated its forecast that it would achieve $US2 billion in productivity gains in the next 18 months, and it went even further forecasting a 10 per cent reduction in Australian operating costs in the period to 2022. As I wrote last week technology, and especially explosives technology, is transforming the economics of mining.

And yet, after the BHP report the market knocked the stock down by about 5 per cent because clearly the analysts were annoyed that their forecasts were not met, albeit for special reasons.

The next day they thought better of it and the stock recovered some of the lost ground. This is a nervous market that does not like adverse reports that don't meet expectations in the short term – no matter what the reason. It will therefore also offer opportunities where good stock is marked down as part of this process.

The second event to catch my eye was when I started early one day to see that the US 10-year bond rate was about steady and Wall Street shares were higher. No action there. But I was wrong. I came back a couple of hours later to discover that the market had slumped and the 10-year bond rate was at 2.94 per cent, which is tantalisingly close to the 3 per cent mark that the chartists believe signals a major bear market in bond prices as yields rise.

The reason for the sudden change was a speech by the new Federal Reserve Chairman Jerome Powell suggesting that US official interest rates were likely to rise. Goodness me. Myself, and hundreds of other commentators around the world have been forecasting rises in official US rates for months, and yet as it moved closer to reality it smashed the market.

In a strange way it's the same story as BHP. What we have is a market that is like a highly trained racehorse that keeps winning as long as nothing goes wrong. There is no margin for error, because the risk of adverse events is not priced into share prices and we have a situation where there is a strong US economy that is about to be made a lot stronger as a result of massive stimulation by the Trump administration.

And that stimulation will require a lot of money, most of which will be borrowed at a time when the Federal Reserve is cutting back its support of the bond market. So, interest rates are likely to rise. The danger is that in the US these higher rates will damage parts of the American economy, and that certainly is not priced into shares. The biggest single danger is a fall in asset prices. Already the US 10-year bond rate has doubled in 19 months, which means bond prices have been savaged.

The Wall Street sudden reversal is an indication that the American stock market hasn't really prepared itself for the new interest rate era. And, of course, that applies to other parts of the world, in particular in Japan and Europe.

Here in Australia we are in an unusual position because we have just been through a major building boom which is now stalling. Our banks have a swag of interest-only loans which will start to mature, and borrowers will be forced to convert them to loans that require greater repayments. That is going to put further pressure on the housing market.

In that environment, higher interest rates will be incredibly dangerous. Accordingly, I doubt whether official rates are set to rise but they will rise as a result of the increase in global interest rates. All other things being equal close to steady official interest rates should put downward pressure on our dollar, but I have been saying that for a while and the sheer magnitude of the debt raising required in the US has in fact weakened the American currency against Australia's.

Refocusing on miners

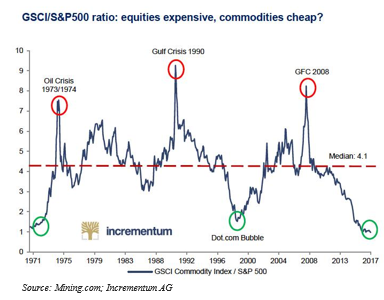

One of the oddities of global share markets is that the biggest rises have been in non-mining shares. A graph crossed my path during the week comparing the GSCI (the Commodities Price Index) and non-mining shares via the S&P 500, and it is clear that miners have not participated. As far as Australia is concerned, our biggest market is China.

China is planning massive investments to reduce pollution and increase electrification and that will require major battery investments. That will cause a substantial demand for our minerals and particularly those that are closely linked to batteries and electrification, including nickel, lithium, copper, graphite, and cobalt. So, we have a stock market where one segment has not enjoyed the rises of other segments, and that segment is an important part of the Australian market. If there is a global correction in shares miners will not escape, and if China keeps up its current levels of demand the miners will recover more quickly.

The above graph tells that the mining bulls reckon that their time is coming and that investment in miners will be a counter cyclical protection.

In particular, the vast amount of debt in the world – currently estimated at $US225 trillion – and the fact that all countries are looking for a lower currency to help their trade, means we could get a flight to hard assets. Normally that means gold, but it can extend to other minerals. Indeed, the rush of speculative money into bitcoin and other digital currencies was in some way driven by an exodus from paper currencies.

If the bitcoin market continues to fall, a lot of that money may shift to gold because there is no doubt that there is a portion of the capital market that believes that real assets like gold are going to have their day again.

So, in looking at your equity portfolio, examine your mining exposure and be aware that while there are no certainties in the world there is a strong body of thought in the world that miners, including second rank miners, are going to perform better than the stocks that have risen so strongly in global markets over the last two years.