Trump spooks markets, and Buffett bails on retail

Robert Gottliebsen

Trump spooks markets, and Buffett bails on retail

We are coming closer to crunch time in the Trump administration. Within the next month or so I think we will have a much better idea as to whether Trump is akin to President Nixon or to President Reagan.

And which way we go will have the most enormous effect on the US stock, bond and currency markets, which until now have been supremely confident that President Trump is akin to Reagan rather than Nixon. It's going to be bumpy, but I think the Trump measures will re-emerge and what is happening in China is likely to be more important for parts of the Australian market.

And I also want to underline what Warren Buffett is saying about retailers. Buffett is not always right, but his warning signs have a chilly aura about them. And, finally, I want to relate my experience of talking to a young couple about superannuation and housing.

President Reagan and President Nixon both came from the right side of the Republican Party. Nixon was a master at organising the bureaucracy and his second term looked set for a successful presidency.

Reagan was a fantastic marketer but had very little idea of the inner workings of the system. However, he put around him an excellent group of people and then marketed their recommendations. He was a brilliant President, from a Republican point of view. Nixon fell over because, while in theory he could have delivered, he had a basic ethical flaw which displayed itself in the Watergate affair and eventually led his impeachment.

Trump is a combination of the two. He has adopted the Reagan philosophy of putting around him good people and, like Reagan, he doesn't have a deep understanding of the inner workings of the political machine. Indeed, he wants to drain the public service swamp.

But the great fear is that, unlike Reagan, he has dangerous Russian-linked baggage – perhaps an ethical weakness on the disclosure side – which will eventually consume him. It was one thing to have the early Russian rumours, but another to sack the FBI director and then to appear to have leaked sensitive material to the Russians about terror.

The market dangers from Trump

I am not in the business of making judgements of what President Trump has done, but I am in the business of warning readers that if he gets badly wounded and the market believes he can't introduce his tax cuts, develop his infrastructure plans, suck back the overseas money into the US and kick-start American investment, then Wall Street is headed for a considerable fall.

This week we saw money flooding out of US shares into bonds, pushing down yields. It was a warning of what might happen.

Interpreting what is taking place in Washington is difficult because the press and the public service hate Trump with a passion, so a lot of the reports are biased. On the other hand, although Trump has appointed good people to key posts, the vast rump of the top levels of the public service have lost their jobs and have not been replaced. This makes policy making and implementation that much more difficult. At the same time there are clear indications that the US economy is slowing, particularly in motor sales.

I had thought that Trump would push through his agenda, but each time the Russian stories get worse I become more nervous. As you read the reports that come out in the coming weeks, relate them to that basic market criteria but also remember that Trump will not give up on his agenda and he will push again.

China, Buffett and the global retail crunch

But while all the daily media will focus on Trump, for Australia the fact that next October/November China will hold the 19th Communist party congress – an event held every five years – may prove to be even more important. Premier Xi Jinping will want to stamp his authority on the congress, and that will require a strong Chinese share market. We are seeing China starting to ease monetary conditions in preparation for the congress, which is a huge event. That should flow into the iron ore and copper prices and, in turn, to our miners. This is an early alert.

As readers will know I have been apprehensive about the retail sector for some time because, frankly, I don't believe they have adapted their databases to the sophistication that Amazon is going to bring to the market. And even in the US, where Amazon has been around for years, there are clear signs of trouble ahead.

But that warning was really underlined by the remarks of Warren Buffett at the recent Berkshire Hathaway annual meeting in Nebraska, where he forecast that in 10 years the retail industry will look nothing like it does now. His partner Charlie Munger chipped in that it would be very unpleasant if the Buffett fund was now in the department store business.

Accordingly, Berkshire Hathaway has sold its $US900 million stake in Walmart stock and switched it into airlines. Buffett says that retail is “too tough” in the age of Amazon. He has had a number of retail forays over the years and many of them have performed poorly, which underlined Buffett's decision to exit.

The Amazon thrust comes as US retailers have announced closures of almost 3200 stores so far this year, and Credit Suisse estimates that by the end of 2017 8600 stores will have been shut – by far the largest on record. The stores are closing not only because of ecommerce, but also because of shifting trends on how people are spending their money.

Entertainment, restaurants and technology are winning in the US, and clothing and accessories are on the decline. As the slump in Oroton shows, Australia cannot be insulated from these trends, so watch very carefully your retail investments. I certainly have only a small exposure. The retail shopping centre area will be affected. Some centres will adapt well to the change but others will be in real trouble. Picking the winners is easy when you are talking about centres like Chadstone, but it's much harder as you move down the market. The graph below illustrates just how dramatic and wide spread US store closures are.

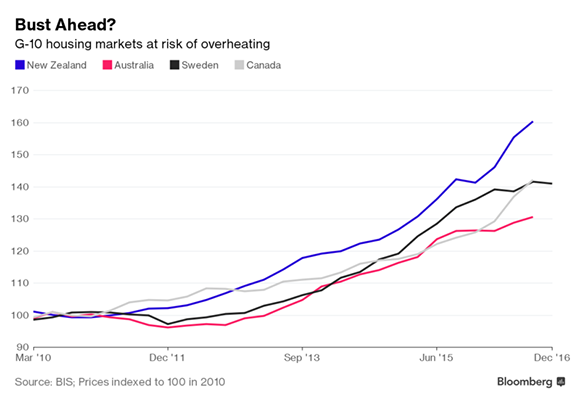

Superannuation and the housing market

During the week I was talking to a young couple about superannuation and housing. They were not far from entering the market for a first home and I was surprised that they only knew the basics about what was in the Federal Budget. It was a reminder that young people have stopped reading newspapers and watching television, and have divorced themselves from superannuation.

I went through the plan and it became apparent to the couple that each could invest $15,000 in their superannuation between July 1 and June 30 next year. They could extract that money from July 1, 2018, but depending on the detail of the legislation might put extra amounts in 2018 and 2019 before they buy their first house.

They have all the problems of where to live, given the constraints of high inner-suburb prices, but the superannuation takes them that little bit closer. But at this stage the measure is not well known, at least on my survey of one.

Meanwhile, as I have been predicting, all the various measures attacking housing is starting to bite and the market, at least in some areas, has gone off the boil. That's exactly what the regulators wanted. In a year or two it might be a good opportunity to buy in a non-boom market.

Last week

Shane Oliver, AMP Capital

Investment markets and key developments over the past week

- Most global share markets fell over the last week on the back of the political crisis around President Trump. Australian shares are now down by around 4 per cent from their high earlier this month and have been hit by the weak global lead combined with pressure on the banks as a result of the Budget's bank levy along with expectations for slowing credit growth and weakness in retailers on the back of weak retail sales and fears around the competitive threat from Amazon. Chinese shares managed to buck the global trend and see a small gain. Reflecting the risk off environment bond yields generally fell, but commodity prices mostly rose helped by a falling US dollar. The weaker $US and good jobs data also helped support a small bounce in the $A.

- The standard narrative at present seems to be that the “Trump trade” has driven the surge in global share markets since the US election and that this will now reverse because of the political crises now surrounding Trump. This is too simplistic and likely to be wrong. First the main reason for the rally in share markets since last November has been the improvement in economic conditions and surging profits that has occurred globally and not just in the US and which had little to do with Trump. Second, the political crisis around Trump won't necessarily stop the pro-business reform agenda of the Republican's. In fact, unless things become terminal for Trump quickly it's more likely to speed it up.

- There is no doubt that the political risks around President Trump worsened further over the last week with increasing talk of impeachment and concern that it will impact the Republican's tax reform agenda. However, it's a lot more complicated than that:

- First impeachment is determined by the House of Representatives and can be for whatever reason the majority of the House decides and conviction, say removal from office, is determined by the Senate and requires a two thirds majority.

- At present Republican's control the House with a 21 seat majority and won't vote for impeachment unless it's clear that Trump committed a crime (and so far it isn't obvious that he has) and/or support for him amongst Republican voters (currently over 80 per cent) collapses.

- However, Trump's overall poll support is so low that if it does not improve the Democrats will gain control of the House at the November 2018 mid-term elections and they will likely vote to impeach him (they hate him and will almost certainly find something to base it on much like the Republican Congress found reason to impeach President Clinton) and then it's a question of whether Trump can get enough support amongst Republican Senators to head off a two thirds Senate vote to remove him from office (Clinton was not removed from office because Democrat and some Republican senators did not support the move to do so).

- This is all a 2019 and beyond story anyway, but the point is that Republican's only have a window out to November next year to get through the tax cuts/reforms they agree with Trump should happen. So if anything, all of this just speeds up the urgency to get tax reform done because after the mid-terms they probably won't be able to.

- Now there is another way for the Vice President and Cabinet to remove a President from office under the 25th Amendment of the Constitution which is aimed at dealing with a President who has become mentally incapable. While some may claim this one is a no brainer, Vice President Pence is a long, long way from doing this.

- The bottom line is that while the noise around Trump and particularly the FBI/Russia scandal will go on for while it does not mean that tax reform is dead in the water. In fact, unless it becomes obvious that Trump has committed a crime resulting in the Republican's themselves moving to impeach him, it's more likely to speed up tax reform and other measures that do not require any Democrat support in the Senate. On this front work on tax reform is continuing including in the Senate and Trump's infrastructure plan (which is likely to be around leveraging up Federal spending and encouraging states to privatise their assets and recycle the proceeds) looks likely to be announced soon.

- The impact of past impeachments on the US share market is mixed and proves little. The unfolding of the Watergate scandal through 1973-74 occurred at the time of a near 50 per cent fall in US shares but this was largely due to stagflation at the time. (Out of interest President Nixon resigned before he was impeached.) President Clinton's impeachment had little share market impact but it was in the midst of the tech bull market.

- Share markets have had a great run and are due a decent 5 per cent or so correction as a degree of investor complacency (as indicated by an ultra-low VIX reading last week) has set in and the latest scandal around Trump may just be the trigger. North Korea risks are another potential trigger and after all it is May (“sell in May and go away…”). Australian shares are down 4 per cent from their high early this month, but global shares are only down 2 per cent or so. However, providing the current Trump scandal largely blows over for now allowing tax reform to continue its unlikely to derail share markets beyond any short term correction. Valuations are reasonable – particularly for share markets outside the US, global growth is looking healthier, profits are rising (by around 14-15 per cent y-o-y in the US and Japan and by 24 per cent y-o-y in Europe) and global monetary conditions remain supportive of shares.

- It seems to have been a week for political scandals. Aside from those around Trump, a corruption scandal has engulfed Brazilian President Temer highlighting that big risks remain around Brazil and allegations have emerged regarding Japanese PM Abe (although he is likely to survive them).

Major global economic events and implications

- US economic data was mostly good. Housing starts fell in April but driven by volatile multis and a further increase in the already strong NAHB homebuilders index points to strong housing conditions going forward. While the New York regional manufacturing conditions index fell in May it rose in the Philadelphia region and industrial production rose sharply in April. Meanwhile, jobless claims remain at their lowest since the early 1970s. All of this is consistent with the Fed hiking rates again next month. The political noise around Trump will only impact the Fed if shares and economic conditions deteriorate significantly and that looks unlikely.

- The Japanese economy accelerated to 0.5 per cent quarter on quarter in the March quarter driven by consumption and trade taking annual growth to 1.6 per cent year on year. This was the fifth consecutive quarter of growth, the first such run in 11 years.

- Chinese data for industrial production, retail sales and fixed asset investment slowed in April consistent with other data indicating that recent policy tightening is impacting. Our view remains that GDP growth will track back from March quarter growth of 6.9 per cent year on year to around 6.5 per cent. The Chinese authorities have little tolerance for a sharp slowing in growth and policy makers are already showing signs of easing up on the policy brake. Meanwhile property price growth seems to have stabilised around 0.5 per cent a month over the last few months, but is still slowing in Tier 1 cities.

Australian economic events and implications

- Australian data was mixed. Jobs growth was strong again in April and forward looking jobs indicators point to continuing strength ahead, but consumer confidence fell and wages growth remained at a record low of just 1.9 per cent year on year.

- While the good jobs numbers will help keep the RBA on hold for now regarding interest rates the continuing weakness in wages growth is a concern and highlights ongoing downwards risks to growth, inflation and the revenue assumptions underpinning the Government's projection of a return to a budget surplus by 2020-21. With unemployment and underemployment remaining in excess of 14 per cent it's hard to see what will turn wages growth up any time soon. So while our base case is that interest rates have bottomed, if the RBA is going to do anything on interest rates this year it will more likely be another cut than a hike. Particularly if property price growth slows.

Shane Oliver is head of investment strategy and chief economist at AMP Capital.

Next Week

Craig James, CommSec

Reserve Bank to the rescue

- If it wasn't for the Reserve Bank, the upcoming week would be quite dull. But there are three speeches by Reserve Bank officials in the coming week.

- The week kicks off on Monday when the Commonwealth Bank releases the April business sales indicator, a measure of economy-wide spending.

- On Tuesday the Reserve Bank Deputy Governor Guy Debelle is set to deliver a speech entitled “How I Learned to Stop Worrying and Love the Basis”– at the BIS Symposium: CIP – RIP? in Basel, Switzerland. While entertainingly worded, the speech probably won't drive financial markets.

- Also on Tuesday the Housing Industry Association releases the “Population and Residential Building Hotspots Report 2017” while Roy Morgan and ANZ release the usual weekly measure of consumer confidence. Confidence levels have fallen after the Federal Budget.

- On Wednesday the Australian Bureau of Statistics (ABS) releases data on Construction Work Done. The data contains estimates of residential, commercial and engineering work completed in the March quarter. The residential work figures will feed in directly to the calculation of economic growth in the quarter.

- In the December quarter construction work done fell by 0.2 per cent in real (inflation-adjusted) terms after falling by 4.4 per cent in the September quarter. Work done is down by 7.8 per cent on a year ago. Public sector construction work fell by 1.6 per cent in the quarter while private sector activity rose by 0.2 per cent.

- But residential building rose by 1.1 per cent in the December quarter and was up by 5.7 per cent over the year. Alterations & additions rose by 2.1 per cent in the quarter while new residential work rose by 1.0 per cent.

- On Thursday the ABS will release detailed job market estimates for April. The main interest is in the geographic and demographic break-up of the data. Participation rates amongst young people have proven historically low in recent years. In contrast, more seniors have been actively looking for work.

- Also on Thursday two Reserve Bank officials are scheduled to deliver speeches. Michele Bullock, Assistant Governor (Financial System), delivers a speech at Australia's Biggest Business Morning Tea 2017 in Sydney. And on the same day – eight hours later – Guy Debelle, Deputy Governor, delivers opening comments at the launch of the FX Global Code in London.

Overseas: Quiet week also in the US

- Not only is it a quiet week for economic data in Australia – the US also has a strangely thin schedule of economic events.

- The week begins on Tuesday with data on new home sales to be released for April. In March, annualised sales rose 5.8 per cent to 621,000 – one of the highest results in nine years. The inventory of new homes for sale fell to 5.2-months' supply, down from 5.4 months at the end of February.

- In the US on Wednesday, the Federal Reserve releases minutes of the last policymaking committee held over May 2 and 3. Pricing has been wavering on the likelihood of further rate hikes in 2017. The minutes will highlight the economic variables that policymakers are watching most closely.

- Also in the US on Wednesday the usual weekly data on mortgage applications is released together with data on existing home sales and the Federal Housing Finance Agency (FHFA) housing price index.

- In March, existing home sales hit decade highs, up 4.4 per cent to a seasonally adjusted annual rate of 5.71 million units. At the current sales pace, unsold inventory is at a 3.8-months' supply. Economists estimate that six months' supply is more indicative of a balanced market.

- On Thursday in the US the usual weekly data on claims for unemployment insurance is released.

- And on Friday in the US, the April data on durable goods orders is released – a key measure of business investment. In March, orders were up 0.9 per cent – the third straight monthly gain.

- Also on Friday the second (preliminary) estimate of US economic growth for the March quarter is released. “Advance” data suggested the economy only grew at a 0.7 per cent annualised pace in the March quarter. But weaker inventories cut 0.9 percentage points (pp) from growth with government spending subtracting 0.3pp. Still, output in the quarter was around 2 per cent above a year ago – a solid, sustainable rate of growth when you consider that personal spending was also soft in the quarter.

Financial markets

- One of the most remarkable features of financial markets over 2017 has been the lack of volatility. That is, up to now. Overnight in the US the so-called “fear gauge” – the CBOE Volatility Index (Vix) – rose by over 46 per cent. In contrast, in early May the Vix had hit the lowest levels in 23 years. Up to yesterday, investors have seemingly ignored events like missile tests by North Korea, rate hikes in the US and military action taken against Syria, But now investors are taking notice about the political travails of President Trump. Former FBI Director James Comey is due to testify next week.

- The absence of volatility up to now wasn't confined to the US, Australian cash rates haven't budged in 2017 and 90-day bank bill yields have moved by just 8 basis points since the start of the years, from 1.74 per cent to 1.82 per cent.

- Have Sydney property prices peaked? The CoreLogic daily price series peaked on April 11 and in just over a month prices have retreated by 1.6 per cent. Melbourne home prices have also eased 1.3 per cent from highs.

Craig James is chief economist at CommSec.

Readings & Viewings

It was a bumpy week on the global markets, largely thanks to billionaire, former reality TV star and now US President Donald Trump. He's not the only President in the firing line, and the Brazilian stock market is showing major signs of strain.

But we all know, as investors, to ignore the short-term market noise. Of course, there's plenty of noise out there in the retail space about Amazon. If you had invested $5000 into Amazon 20 years ago, here's what you have in your kitty today.

As we mentioned above, Warren Buffett isn't taking any prisoners when it comes to retail. He's switching more cash into an area he once warned investors to avoid.

How Air New Zealand is experimenting with augmented reality.

Meanwhile, Microsoft founder Bill Gates took to Twitter this week to share some life advice with new college graduates.

7/ Meanwhile, surround yourself with people who challenge you, teach you, and push you to be your best self. As @MelindaGates does for me.

— Bill Gates (@BillGates) May 15, 2017

Also turning to Twitter was a co-founder of the social network, but in a different way.

Staying in the online space, according to Bloomberg the digital marketplace site Etsy could soon be on the IPO market.

Hedge funds are betting $1 billion on Snap to drop.

Volkswagen's CEO is in a criminal probe.

Changing pace, and over in the UK, Lloyd's Banking is finally out of government hands, eight years after being bailed out.

And it seems that despite Brexit, the amount of new office space hitting the London market is soaring. Now, that's likely to be a problem amid fears of a looming business exodus.

Ireland has stolen another asset from the UK.

Grazie, Italia! Italy is giving away more than 100 of its castles.

Japan's economy is rapidly “warming”. The Japanese have the hots for Kiwis, and if you didn't know, Apples now come from India.

What a trade-off for the Brits. Would we in Australia rather this?

That was a close one. Or still is. We certainly want to keep this in check:

And finally, Americans are a little late to this party, but they have now arrived. Welcome to the debt high club.

Could Hollywood save the day? Michael Moore hopes to bring down President Trump. The Fahrenheit 9/11 filmmaker is well across Trumponomics; after all, he did predict Trump's presidency.