Trump and our miners

Robert Gottliebsen

Trump and our miners

This week I had the pleasure of lunch with Sandeep Biswas at the Melbourne Mining Club. Sandeep is the chief executive of Newcrest Mining and as I listened to him, I began to realise we are developing a multi-strata resources industry in the wake of the terrible times the industry has been through in recent years.

But before we discuss these strategic alternatives, which clearly affect BHP Billiton and Rio Tinto, I want to talk again about Donald Trump.

This has been the week of Trump disenchantment, when markets began to question whether the refugee gymnastics indicate that he will be unable to pull off his dramatic US revolution.

The surface manifestation of those doubts came in the bond markets, and we saw bond yields start to fall early in the week. But then across my desk came a fascinating extract from a new research paper from several economists, including Thomas Piketty, that reveals that the bottom 50 per cent's share of income in the United States is "collapsing".

In the US, between 1978 and 2015, the income share of the bottom 50 per cent fell from 20 per cent to 12 per cent. Total real income for that group actually fell 1 per cent during the period.

That's not the case elsewhere. In China – where there also has been a marked rise in income inequality – the bottom 50 per cent saw their income go up by 401 per cent; not surprising given the industrialisation of the world's second-largest economy. Even in developed France the bottom 50 per cent saw their income grow by 39 per cent.

President Trump was elected on a promise to help what he said were "forgotten Americans". And they love what he is doing.

Nevertheless we are going to see a lot more market fluctuations because of the totally unconventional way Trump is approaching the presidency. We could never imagine a US president reading the law in public to influence judges. Who would have imagined a company taking its business away from the president's daughter being given a presidential blast that sent its share price down.

We are going to have a lot more of these adventures.

But for the share market a key issue is whether Trump will actually be able to reduce the US tax rate substantially, and whether that will convert to a dramatic rise in American industrialisation and a flood of money into the US.

I believe he will pull this off, but I must emphasise that those that have a different point of view have validity. The jury is out. (Although, the market is coming around to my view, and late in the week bond yields firmed and shares rose.)

Three majors, three pathways

What happens in the US has a big longer-term impact on commodity demand in our resources industry, which brings me to the strategy of Biswas at Newcrest. First and foremost Newcrest is a play on the gold price. But there is more to the company than that.

Sandeep's background is technology and innovation, and he cut his teeth on improving the productivity at Mount Isa and Western Mining. And later he was recruited by Rio Tinto to run the alumina business.

He believes that increasingly mining companies are going to need to extract from more difficult ore bodies, often deeper. This culture of technology innovation is what has enabled Newcrest to make sense of the Lihir gold/copper deposits in New Guinea. And it has transformed the Cadia deposits in NSW. A similar approach will be required in the enormous Wafi-Golpu deposits in Papua New Guinea where Newcrest has used its exploration skills to uncover a massive new gold-copper deposit under the original reserves. But there is still a lot of work to be done.

Basically, the Biswas strategy is to duplicate the old Western Mining strategy, which involved looking for ore deposits and finding ways to develop them. But he is using modern technology in a way not possible in the old WMC days. At the lunch he called on the industry to be more collaborative in developing new technologies. He ruled out major acquisitions by Newcrest, preferring instead to improve the productivity of exiting deposits and exploration. Of course, Newcrest would not rule out buying into small explorers who made a major find and needed a partner. This is old fashioned mining.

Fascinatingly, BHP has a different strategy. Yes, BHP is looking to use all the modern technologies to improve the productivity of its mines. But it is not an enthusiastic explorer for new deposits around the world. BHP (along with Rio) has just had a fantastic half-year, but it will be even better this year if the current prices hold. BHP is clearly going to distribute a lot of its spare cash to its shareholders.

But BHP's chairman, Jac Nasser, and chief executive Andrew Mackenzie were called up by Trump prior to his inauguration. Trump wants BHP to invest heavily in its US oil and gas reserves because he wants to develop energy in the US to support his infrastructure and industrial expansion plans. And the first installment has been this week's $2.9 billion commitment to develop the Mad Dog 2 field in the Gulf of Mexico. Of course, in the process it might send the price of oil and gas down.

And Trump offered the Big Australian the carrot of much lower tax rates in the US to entice BHP. We do not know just how much money BHP is going to commit to US development but my guess is that it will substantial. BHP is a long-term bull on oil prices. Meanwhile, the fact that China is reducing its electric arc furnace capacity (which uses scrap as a raw material) means that more iron ore will be needed to support steel production.

Understandably Rio was not wooed by President Trump and the clear message from Rio is that it's going to be in the business of rewarding its shareholders. The market was a bit disappointed at the latest cash distribution but it's clearly going to get bigger. The group does have some projects which may well be developed in the future but, after a terrible time following the Alcan acquisition, Rio wants to combine its much improved productivity and higher prices with unprecedented rewards to shareholders.

So there you have the three models:

Newcrest, with its emphasis on new operations and exploration via technology;

BHP, with mountains of cash and the enticement of US investments, and;

Rio Tinto, with lots of wonderful surprises for its shareholders. (And remember with Rio that although the returns in 2016 were excellent, they are set to be even better in 2017 if current prices hold.)

And another thing

And finally, AMP still has not really woken up to the fact that it missed the market. Challenger has built up a huge business on the back of annuities. That was AMP's bread and butter and they let a rival not only take their lunch but also show that the market was enormous. AMP was left with the dregs.

Bank-owned life offices like Colonial and MLC also missed the market. The disruptor, Challenger, rejoices every day that the traditional companies were asleep. In these days of fast movement what we have seen in life assurance will be repeated in many industries.

Readings and Viewings

Investment bubbles are rarer that we think and harder to spot, says the Economist's Buttonwood columnist. “There were many more occasions when markets doubled over three years; around 14 per cent of the total. After such rises, the markets dropped by half in the following year on fewer than one in 20 occasions … [O]n this basis, a sharp rise in a market is more of a buy signal than a sell indicator.”

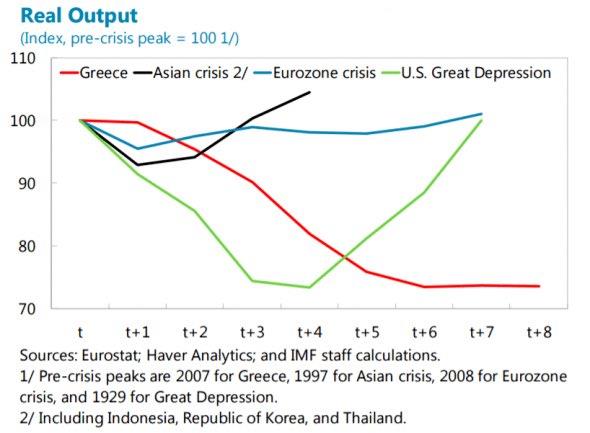

On Europe, we stumbled across this frightening IMF graph this week. 'T' shows the pre-crisis peak for several infamous crises, and then each ensuing year. Greece is eight years in with no uplift in sight.

Finance commentator Jim Rickards – best known for predicting the 2008 crisis – foresees trouble for China.

Radio National this week hosted British business journalist Paul Mason, who is trying to come to grips with, among other things, the effects of automation on capitalism.

Saturday Night Live has been making news with its Trump Administration spoofs. We think this one on Sean Spicer was particularly good.

Closer to home, Australia Post CEO Ahmed Fahour has been in the news this week over his extravagant $5.6 million annual salary, and now there's word he will be entitled to a $4.3 million retirement package. Over in the UK, Thomas Cook shareholders are revolting against a £1.6 million a year payout to boss Peter Fankhauser.

Elsewhere, this tequila shot had plenty of kick during the week as the world's largest maker of the fire liquid Mexico's Jose Cuervo raised $US900 million through an IPO. And like the liquid, the company's shares had an instant reaction as investors consumed the stock.

Meanwhile, Banco de Mexico raised official interest rates for a fourth time this week, by 50 basis points to 6.25 per cent, as the country faces low growth and high inflation and stares down economic threats from Donald Trump.

This week our analysts at Intelligent Investor revised their recommendation on Coca-Cola Amatil to SELL, citing ongoing declines across the soft drinks business. The news at Atlanta-based Coca-Cola Co. isn't any better, and Coke is officially slimming down.

Maybe Coca-Cola needs to think outside of the soft-drink can and take a leaf out of Domino's book. The pizza maker, having already experimented with delivery by drones, has now set up a pizza weddings registry.

Retailing has never been easy, and cosmetics giant L'Oréal has decided to bite the bullet and offload its subsidiary The Body Shop, bought from the late founder Anita Roddick a decade ago for £652 million.

Lastly, this beachfront property for sale in Seattle, Washington, has an interesting twist. It's a treehouse, and it's on the market for $US475,000. But, technically, it doesn't exist.

Last Week

Shane Oliver, AMP Capital

Investment markets and key developments over the past week

Global share markets rose over the last week helped by a combination of good economic data and announcements from President Trump progressing his deregulation and tax reform agenda. Bond yields mostly fell though helped along in Europe by dovish comments from ECB President Draghi. Commodity prices were mixed with oil down but metals up and iron ore at its highest since 2014. The US dollar rose and this saw the Australian dollar pull back.

The message from the first few weeks of Donald Trump's presidency is that while he and his administration is generating a lot of noise on a lot of issues as long as he continues to make periodic announcements progressing his pro-growth policies – rolling back Dodd-Frank, working towards a “phenomenal” tax plan, making “life good” for airlines, etc – then share markets will respond positively. So while all the noise around the travel ban, whether the Lindt Café siege was “underreported” (I was in Memphis on an Elvis pilgrimage at the time and the siege had plenty of coverage on US TV!), etc, is interesting, investors should continue to turn down all this noise when making investment decisions.

While unwinding the Dodd-Frank financial regulations will take time and face constraints (as it will likely require the support of 8 Democrat Senators, although it may be possible to find work arounds), tax reform is likely to proceed more quickly as Congress has already done significant work on it and it can pass through the Senate using budget reconciliation rules that only require a simple Senate majority – which the GOP has. It now looks likely that the Trump administration will submit a tax plan to Congress in a few weeks – this is almost certain to include a cut in the corporate tax rate (to 20 per cent or so) and possibly also a cut to personal income tax rates. It's less clear whether a “border adjustment tax” (rebating tax on exports and taxing imports) will be included. Taking the US corporate tax rate from 35 to 20 per cent will put massive pressure on Australia at 30 per cent and other countries to follow suit (the OECD average is around 25 per cent).

In Australia, the Reserve Bank left interest rates on hold as expected, but in its Statement on Monetary Policy made little significant changes to its growth and inflation outlook – seeing December quarter GDP growth rebound, growth averaging around 3 per cent over the next few years and inflation heading back to 2 per cent by year end. The Bank's post meeting statement, a speech by Governor Philip Lowe and the Statement on Monetary Policy all presented a relatively upbeat assessment on the economic outlook. While we have growth outlook, our view remains that it will take longer for inflation to return to target than the RBA is allowing, particularly with wages growth remaining at record lows and the Australian dollar trending higher. As a result we remain of the view that the RBA will cut rates again this year, probably in May after the next round of inflation data. Given the improving global growth and inflation outlook though and the desire to avoid adding to financial stability risks, our call for another RBA rate cut is a close one.

Surprisingly, the RBA's level of concern around the property market does not appear to have increased despite a further pick up in lending to property investors and rapid price growth in Sydney and Melbourne. This appears to partly reflect the RBA's assessment that lending standards have tightened, the supply of property is set to rise with longer than normal lags and that part of the recent upswing in investor credit may reflect investors paying for properties bought of the plan some time ago. There still remains a case for a precautionary lowering in APRA's 10 per cent investor credit growth limit though.

Major global economic events and implication

US job openings, hiring and quits remained basically unchanged at relatively high levels, jobless claims fell to ultra-low levels and the trade deficit narrowed slightly in December. 71 per cent of US S&P 500 companies have now reported December quarter profits with 75 per cent beating earnings expectations with an average surprise of 3.6 per cent and 51 per cent beating on revenue. Earnings are now expected to be up 6.3 per cent from a year ago.

Japanese data showed a slight fall in confidence and continuing weak wages growth but improved machinery orders, a rise in Japan's leading index and an ongoing decline in bankruptcies and the first annual rise in producer prices since March 2015.

Chinese foreign reserves fell below $US3 trillion for the first time since 2011 and are down from a high of $US4tn highlighting that China continues to see capital outflows and is using its reserves to slow the decline in the Renminbi (are you listening President Trump?).

The reserve banks of India and New Zealand both left interest rates on hold and both look to have a neutral stance for now but with the RBNZ penciling in one hike in 2019.

Australian economic events and implications

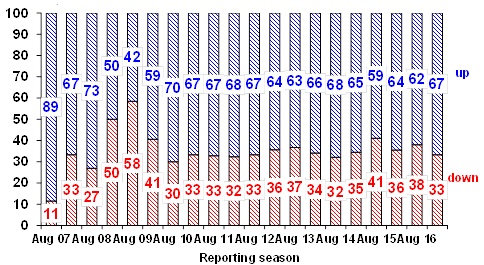

It's too early to read much into the December half profit reporting season because less than 20 major companies have reported to date. But so far so good with 67 per cent exceeding earnings expectations compared to a norm of 44 per cent, 67 per cent of companies seeing profits up from a year ago and a stronger than expected result from Rio Tinto confirming that the turnaround in resources sector profits is on track.

Chart 1: Australian profit results relative to market expectations (percentage of results)

Chart 2: Australian company profits relative to a year ago (percentage of companies)

- On the data front in Australia, December quarter retail sales volumes rebounded 0.9 per cent adding to confidence that consumer spending and hence GDP growth rebounded in the December quarter. While retail sales unexpectedly fell 0.1 per cent in the month of December, this reflected a sharp fall in hardware, building and garden supplies (possibly reflecting the wind down of Masters) so is unlikely to mean much. Meanwhile new home sales were flat in December according to the HIA but still appear to be tracing out a gradual downtrend since their high in 2015 and December housing finance commitments saw a slight swing back in favour of owner occupiers but not much given the strong gains in investor lending in prior months.

Shane Oliver is chief economist at AMP Capital.

Next Week

Craig James, CommSec

Bevy of indicators at home & abroad

In Australia, another bevy of economic indicators await investors in the coming week. There is also a solid list of ‘top shelf' economic indicators to wade through in the US. The Federal Reserve Chair, Janet Yellen, also delivers the semi-annual testimony to Congress. In China, inflation data is in focus on Tuesday.

In Australia, the week kicks off on Monday when the Bureau of Statistics (ABS) releases the Overseas Arrivals & Departures publication. This publication includes data on tourist arrivals and departures together with longer-term migration data.

Tourist arrivals fell by 0.7 per cent in November. And departures fell by 3.5 per cent. Arrivals were up 8.7 per cent on the year with departures up 3.3 per cent.

Also on Monday, data on credit and debit card lending will be released from the Reserve Bank. Compared with a year ago, the average credit card balance was up by just 0.3 per cent. In smoothed terms (12 month average) the average balance was down by 1.7 per cent.

On Tuesday, ANZ and Roy Morgan release weekly consumer sentiment survey results with the focus not just on sentiment but also on the gauge of inflation expectations.

Also on Tuesday, NAB releases its January business survey. There were solid readings posted in the December survey with trading conditions at the best levels in nine years.

Lending finance figures are also issued on Tuesday, covering new housing, lease, personal and business commitments made in December.

On Wednesday there is yet another reading on consumer confidence – this time the Westpac/Melbourne Institute survey. For the record, the Reserve Bank looks at both surveys to ensure it is well versed on how consumers are feeling.

Also on Wednesday the ABS recasts the data on new vehicle sales, expressing the figures in seasonally adjusted and trend terms. Sales were the second highest for any January month in January 2017.

On Thursday, the ABS issues the January employment report. In December employment rose by 13,500 after rising by 37,100 in November. Full-time jobs rose by 9,300 while part-time jobs rose by 4,200. In fact full-time employment lifted by 95,000 in the December quarter – the best result since the September quarter 2010.

We expect a more modest 5000 lift in jobs in January with the jobless rate unchanged at 5.8 per cent.

Overseas: Famine to feast in the US

There are ‘top shelf' US indicators and testimony from the Federal Reserve Chair in the coming week.

The week kicks off on Tuesday with the Federal Reserve Chair, Janet Yellen, to deliver semi-annual testimony on monetary policy. The Fed chief speaks to the Senate Banking Committee on Tuesday and then the House Financial Services committee on Wednesday.

Also the business optimism index from the National Federation of Independent Business (NFIB) is released on Tuesday with the producer price index (PPI) or the main measure of business inflation. Excluding food and energy, producer prices are up just 1.6 per cent over the year.

On Wednesday the consumer price index (CPI) is released alongside retail sales, industrial production, the NAHB housing market index and capital flows data. The core CPI (excludes food and energy) is expected to remain 2.2 per cent higher than a year ago. Non-auto retail sales may have lifted 0.4 per cent in January while production may have eased 0.1 per cent after an out-sized 0.8 per cent gain in December.

On Thursday, data on building permits and housing starts are released together with the influential Philadelphia Federal Reserve survey. Housing starts soared by over 11 per cent in December but they may have eased by 0.3 per cent in January. Also on Thursday the weekly data on new claims for unemployment insurance is issued.

On Friday the leading index for January is released with a 0.4 per cent lift tipped after the solid 0.5 per cent increase in December.

In China the National Bureau of Statistics releases inflation data on Tuesday. Currently producer prices are up 5.5 per cent on the year with consumer prices up 2.1 per cent.

Sharemarkets, interest rates, exchange rates and commodities

The Australian profit reporting season lifts into top gear in the coming week. On Monday, earnings are scheduled to be released by Newcrest, Ansell, Bendigo & Adelaide Bank, Aurizon, Amcor and JB Hi-Fi.

On Tuesday earnings announcements are expected from Challenger, Cochlear, GPT Group and Treasury Wine Estates.

Among those expected to report earnings on Wednesday are A2 Milk, Boral, CSL, Commonwealth Bank, Computershare, Domino's Pizza, Dexus Property, Inghams, Wesfarmers and Sonic Healthcare.

On Thursday, a raft of companies are expected to issue results including: Goodman Group, Mirvac, Origin Energy Telstra, Tatts Group, Star Entertainment, Sydney Airport, South32, Spark New Zealand, IPH Limited, Bapcor, Evolution Mining and Mineral Resources.

On Friday, ASX Group is amongst those listed to issue earnings with Duet, Mantra, Link and Abacus.

Craig James is chief economist at CommSec.