Three reasons to be optimistic about US household spending

The US economy continues to show signs of strength, with household spending improving over the past few months. There are a number of reasons to be optimistic about the outlook for US consumption, with wage growth expected to pick up, a stronger dollar and lower oil prices improving the purchasing power of US incomes.

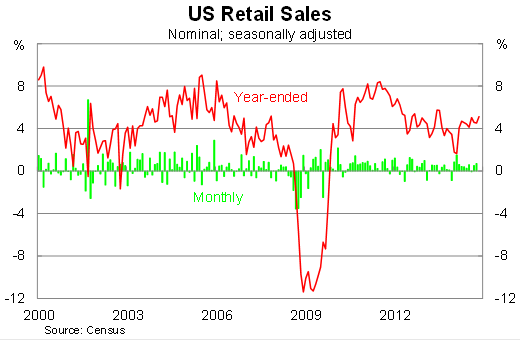

US retail sales rose by 0.7 per cent in November, beating market expectations, to be 5.1 per cent higher over the year. Household spending has picked up in the last couple of months (boosted by favourable revisions) and activity in October and November is currently 1 per cent higher than the September quarter average.

Sales of motor vehicles accounted for almost half the expansion during November. Motor vehicle sales climbed by 1.7 per cent in the month, to be 9.5 per cent higher over the year. Retail, excluding motor vehicles, rose by 0.5 per cent and annual growth is now running at its fastest pace since April 2012.

The value of gasoline sales fell by 0.8 per cent in November, reflecting the sharp decline in the oil price, which has directly improved the purchasing power of US homes and underpins the current recovery.

Spending on building materials increased by 1.4 per cent in the month and is now 7.8 per cent higher over the year. After a rough beginning to the year, spending on building materials has rebounded strongly, although the same cannot be said of broader measures of residential construction activity.

Improving labour market conditions continue to underpin household spending activity. Consumption though remains somewhat weaker than might be expected given the strongest employment growth in around 15 years.

That reflects a number of factors, including the fact that job creation has been concentrated in lower-paying positions. Unfortunately, high-paying jobs lost during the recession have been replaced by low-paying jobs during the recovery.

Wage growth more generally remains subdued and has weighed on household spending activity. Average hourly earnings have climbed just 2.1 per cent over the year on a nominal basis, with real growth only 0.3 per cent higher (following a sustained period where real average hourly earnings were declining).

There are three reasons to be optimistic about the outlook for household spending.

First, wage growth will begin to pick up as spare capacity continues to ease. At the rate that employment is growing, it will only be a matter of time before employers start competing for the best available talent, giving workers greater leverage and pushing wage growth to its highest level in years.

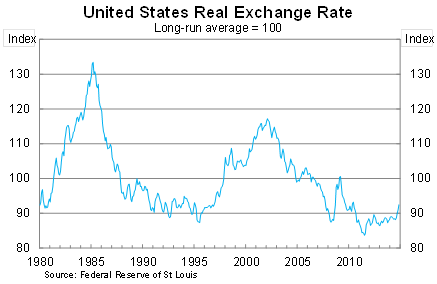

Second, a stronger US dollar will directly improve the purchasing power of US households. The real exchange rate has increased by 4.3 per cent over the past three months and is over 5 per cent higher over the year. This is supporting import growth and will continue to support household spending in the months ahead.

Third, as noted earlier oil and petrol prices are lower. As a necessity, spending on petrol is often insensitive to price shifts. As a result, weaker petrol prices will directly lift the purchasing power of US incomes. They'll have more money to buy food, clothes and household goods, while still consuming a similar level of petrol and other energy. It also helps reduce an important barrier to people finding new jobs or deciding to get back in the workforce.

From a rates perspective, this data provides just another example of the momentum the US economy has as we approach 2015. Not all sectors are booming -- the housing sector, for example, remains a concern -- but the economy is producing jobs at a record pace and that will begin to flow through to wage demands and eventually spending.

Perhaps the most important message we can take from this data -- in addition to the strong payrolls data -- is that the economy did not lose any momentum when the Federal Reserve ended its asset purchasing program. It might be too soon to say with any certainty, but it appears that the only people concerned about the end of asset purchases were market participants, the real economy didn't skip a beat.