Three forces that could trigger Australia's next recession

- {{x.value}}

{{ twilioFailed ? 'SMS Code Failed to Send…' : 'Enter verification code' }}

{{ completedStep1 ? 'Authentication & Security' : content.trialHeading.replace('{0}', user.FirstName) }}

{{ content.upgradeHeading.replace('{0}', user.FirstName) }}

The email address you entered is registered with InvestSMART

Please login to continue

We have sent you an email with the details of your registration.

Looks you are already a member. Please enter your password to proceed

{{ upgradeCTAText }}

Updating information

Please wait ...

Your membership to InvestSMART Group recently failed to renew.

Please make sure your payment details are up to date to continue your membership.

Having trouble renewing?

Please contact Member Services on support@investsmart.com.au or 1300 880 160

You've recently updated your payment details.

It may take a few minutes to update your subscription details, during this time you will not be able to view locked content.

If you are still having trouble viewing content after 10 minutes, try logging out of your account and logging back in.

Still having trouble viewing content?

Please contact Member Services on support@investsmart.com.au or 1300 880 160

Please click on the ACTIVATE button to activate your Intelligent Investor 15-day free trial

Please click on the ACTIVATE button to finalise your membership

Unsuccessful registration

Registration for this event is available only to Eureka Report members. View our membership page for more information.

Registration for this event is available only to Intelligent Investor members. View our membership page for more information.

- You are already registered for this event.

- This event is already full.

- Please select a quantity for at least one ticket.

- {{ i }}

Forgotten password

Please enter your email address below to request a new password

- Verify your email address by clicking on the link we sent to {{user.Email}}

- You now have free access, we look forward to helping you on your financial journey.

Could Australia experience a recession in the next few years? Absolutely.

Is it probable? Not yet, but let's explore how it might unfold.

Speculating about a recession is fraught with difficulties. For one they are very rarely predicted -- and almost never by central banks -- because they are by their very nature extreme outcomes. Those who do predict recessions are often viewed as crackpots, though when they get it right they get to have their 15 minutes of fame.

Nevertheless, it's important to understand the risks facing the Australian economy. Firstly, it provides an opportunity to safeguard the system against future shocks. Secondly, it leaves policymakers in a better position to formulate monetary or fiscal policy. Thirdly, it allows us to learn from our mistakes if things do turn pear shaped.

If Australia does suffer a recession in the next few years it will most likely begin in one of three areas: the property market, our major banks or our mining sector. If I was a betting man I'd put my money on either the property market or the mining sector, with the financial sector suffering a second-order shock.

Each of these sectors is systemically important to the Australian economy and our financial system. More importantly each of these sectors faces distinct headwinds over the next few years.

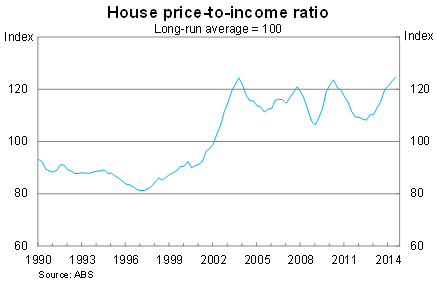

Property prices in Australia are elevated by global standards and widely considered absurd by leading international experts. We pay a premium for our property, regardless of location, and our high debt burden leaves us vulnerable to an income shock.

If it wasn't already obvious, yesterday's GDP release made it official: Australia is suffering from an income recession (An income recession spells more gloom for Australia, December 3). Nevertheless, property prices continue to climb, underpinned by the highest level of investor activity on record.

This can be explained, in part, by low interest rates but it's hard to see this persisting as real wages decline. If income growth remains weak over the next few years, households will begin tightening their belts, and taking on high levels of debt will no longer appeal (regardless of interest rates).

It's foolish to predict a house price crash -- many have tried -- but it's important to remember that Australian property prices have already suffered three downturns over the past decade. Structurally the market is much weaker now that it was during the 1990s and 2000s and any downturn is likely to be greater now that income growth is so weak.

Whatever happens to the property sector will also happen to the banking sector (albeit with a delay), that's why the banking system remains vulnerable to a second round shock.

Our banking system is wildly imbalanced by any conceivable international benchmark. Consider for example that Australia has three of the biggest 20 banks in the world for market capitalisation. We also have four banks that sit among the world's top 40 banks for total assets.

It's some achievement when you consider that Australia's big four banks have almost no presence outside of the domestic market. You'd struggle to find too many Americans or Poms who have heard of NAB or Westpac; the same cannot be said for most of the other banks on the list.

How has this happened? A combination of loose lending standards -- combined with ill-considered tax policies and Australia's love of property -- has created the perfect environment for rapid asset creation. Australia's big four banks are among the most leveraged in the world and only recently the Commonwealth Bank and Westpac were more leveraged than Lehman Brothers was just before it collapsed.

A sufficient shock to the property market would have lasting effects on the banking sector. In the best case scenario their profitability takes a hit and they pull back on housing and business investment. In the worst case scenario we discover that each of the big four are not only too big to fail but also too big to save.

As for the mining sector, the issue is well known: we all know that mining investment will collapse but we have no idea about either the timing or the magnitude of the downturn.

The Reserve Bank's current outlook is based on the idea that they have the timing right. It believes that the non-mining sector -- including exports and residential investment -- will pick-up to sufficiently offset the hole left by mining investment.

There is considerable uncertainty surrounding that outlook and mounting speculation that the non-mining sector simply does not have the necessary momentum. But the risks from the mining sector are broader than that and come back to our reliance on Chinese investment to generate domestic growth.

Increasingly there is evidence that China is also trying to rebalance its economy away from infrastructure and property investment towards exports and consumption.

It's a smart move but a difficult one to pull off. China has arguably the biggest housing bubble in the world. Estimates of house price-to-income ratios are between 15 and 40 times income in some of the major cities -- dwarfing even Australia's most expensive areas.

Floor space per capita in China has surpassed 30 square metres, rocketing past the level in Japan during 1988 prior to its property collapse. Housing construction has been rapid, largely due to urbanisation, but annual population growth has slowed to just 0.5 per cent and China's population should peak in the next 10 to 15 years.

China had a clear choice -- either it suffers a massive property crash or it tries to rebalance the economy and mitigate any damage. So far it appears to have made the right choice.

But it's the wrong choice for Australia. Besides iron ore and coal, Australia doesn't produce anything that China wants. As China's infrastructure boom subsides, so does Australia's economic fortunes.

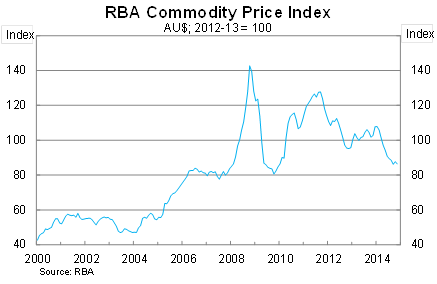

We're already seeing this play out through lower commodity prices, which have squeezed margins and threaten the viability of every iron ore miner in the country not named Rio Tinto or BHP Billiton. When the shakeout is complete, they may be the last two standing.

Obviously much of this is speculation; the Australian economy may rebalance more quickly than commonly expected and absorb any weakness in the mining sector. The property market may prove more resilient than currently feared; a correction kicked further down the road.

But these are the areas that market participants should be focused on. Are there any cracks in the property or mining sectors? What is China doing? And what are the implications for the financial sector?

The reality is that while a recession is far from certain, it is more likely now that it has been at any point since the early 1990s. Understanding the likely causes will help us address the issue but also ensure that these imbalances don't happen again.

Our property and mining sectors are the most likely candidates and both are risky propositions at the current time. Both need suffer only a minor shock to stagger the broader economy and that's where market participants should be focused as 2014 draws to a close.