The Week in Review: March 16, 2018

There's more to go on Trump's tariffs

Investment markets and key developments over the past week

- Share markets were a bit messy over the last week as worries about US trade barriers continued, particularly in relation to China. US and Eurozone shares fell, Chinese were flat and Japanese shares rose. Australian shares also fell not helped by the soft US lead but also the start of the Banking Royal Commission and the Labor Party's policy to cut back on access to franking credits. Bond yields generally fell, as did oil and metal prices along with the $A.

- The events over the last week highlight that there is more to go on the tariffs from President Trump. Ongoing personnel changes in his team (Rex Tillerson leaving, CIA director Mike Pompeo replacing him and Larry Kudlow replacing Gary Cohn) on balance suggest less opposition to further moves on tariffs notably against China. While it would be wrong to read too much into the Democratic win in the special election in Pennsylvania (as the candidate was a very lite Democrat) it's consistent with a Democratic “wave” forming to retake control of the House in the mid-terms all of which puts more pressure on Trump to appeal to his base (and they like tariffs!). And the Administration is continuing to work on a package of tariffs and investment restrictions regarding China's alleged theft of US intellectual property. We remain of the view that there won't be a global trade war and Trump will use his Art of the Deal/go in hard approach to try and reach a settlement with China to which the Chinese are likely to be responsive to some degree as they know there is an issue. But it's clear that trade will be a source of volatility and a risk to watch for some time to come.

- On the positive side in the US though, the Senate passed a bill to reduce the impact of the Dodd-Frank financial regulations on smaller banks. it's yet to go through the House but there's a good chance it or something similar will.

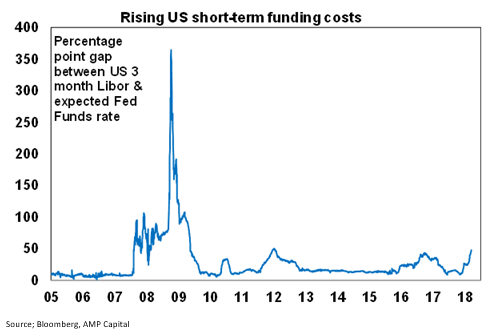

- Should we worry about the blow out in US short term money market rates? During the global financial crisis stress in money and credit markets showed up in a blowout in the spread between interbank lending rates (as measured by 3-month Libor rates) and the expected Fed Funds rate (as measured by the Overnight Indexed Swap or OIS rate) as banks grew reluctant to lend to each other with this ultimately driving a credit crunch and a big increase in bank funding costs (and of course “out of cycle” mortgage rate increases in Australia). Since late last year we have been seeing a rise in the same spread with the gap between 3-month Libor and the expected Fed Funds rate rising from 10 basis points in November to around 46 basis points now. This in turn has also caused an increase in money market borrowing costs in Australia. So far the rise in the US Libor/OIS spread is trivial compared to what happened at the time of the GFC and unlike back then it does not reflect banking and credit stresses. Rather the drivers have been increased US Treasury borrowing following the lifting of the debt ceiling early this year, US companies repatriating funds to the US in response to tax reform and money market participants trying to protect against a faster Fed. So don't worry – it's not a GFC re-run! However, the longer it lasts the more it will affect bank funding costs which could result in some (albeit minor) upward pressure on variable mortgage rates (maybe for investors?), partially offsetting recent cuts in some fixed mortgage rates.

- In Australia, taxation is clearly shaping up as a major policy difference ahead of the next Federal election with Labor adding the removal of access to franking credits for Australian's who pay little or no tax to already announced policies to raise the top marginal tax rate, restrict access to negative gearing and halve the capital gains tax discount. For what it's worth the proposed change on franking credits does make some sense as dividend imputation was meant to remove the double taxation of dividends, not compensate people for tax already paid when they are not paying any tax on dividend income anyway. But it will affect a lot of self-funded retirees who have come to rely on franking credits (particularly less well-off retirees because they won't have tax to offset it against). The tax changes if introduced will also drive significant impacts on various asset classes with lots of cross currents: the increase in top marginal tax rates will likely drive greater use of negative gearing across all assets; but the changes to negative gearing will benefit new housing and other assets but would be very negative for existing housing; and the changes to dividend imputation would be negative for high dividend yielding highly franked shares but positive for other shares and other assets including housing as those affected re-allocate their investments. That said the ALP still has to get elected and the next election could be a year or more away.

Major global economic events and implications

- While US retail sales disappointed again in February, the tax cuts, strong jobs growth and high consumer confidence point to a bounce in March. Meanwhile, small business confidence rose to its highest since 1983, regional manufacturing conditions indexes remain very strong as does the NAHB home builders index. Although, core CPI inflation remained at 1.8 per cent year on year in February, it's been running above a 2 per cent pace for the last six months and producer and import price inflation continues to move higher. All of which keeps the Fed on track to raise rates again in the week ahead.

- ECB President Mario Draghi's comments over the last week highlighted ongoing uncertainty about when inflation will return to target particularly as the rise in the Euro weighs on inflation. He is still clearly in no hurry to start exiting easy money.

- Chinese economic activity data for January and February continued to defy expectations for a slowdown. While retail sales slowed a bit, growth in investment and industrial production actually accelerated which when combined with trade data suggests that growth may actually have picked up a bit so far this year. All of which likely emboldens President Xi Jinping in pushing on with his reform agenda, which over the last week has been facilitated by National People's Congress agreeing to a restructuring of the government (including a merger of bank and insurance regulators).

Australian economic events and implications

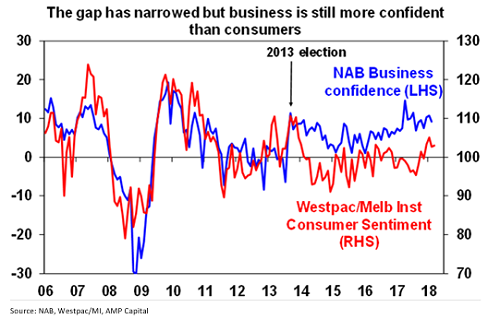

- In Australia, the gap between consumer and business confidence remains with record business conditions and just a small fall in business confidence in February and flat consumer confidence. The gap is likely to remain until wages growth picks up. Meanwhile housing finance commitments remain weak with a fall in owner occupier lending and a bounce in investor loans but after only after several months of falls.

Shane Oliver is Chief Economist at AMP Capital

Share this article and show your support