The Week in Review: June 1, 2018

Italian turmoil and US trade rattle markets.

Investment markets and key developments over the past week

- The past week saw financial markets dominated yet again by geopolitical developments with first the turmoil in Italy and then US trade announcements rattling share markets with most falling and driving down bond yields (except in Italy of course) as investors sought safe havens. Commodity prices were mixed with copper up slightly but oil and iron ore down. Despite the volatility in markets the $A rose slightly as the $US pulled back.

- Trade war worries back to the fore again with Trump announcing that tariffs and investment restrictions on China will be formalised on June 15 and 30 respectively and start soon thereafter and that US exemptions for the EU, Mexico and Canada to the steel and aluminium tariffs announced earlier this year are ending. These moves are concerning and heighten the risk of a global trade war, but both need to be put in some context. First, the measures regarding China are the same as those flagged on March 22nd which were due to be formalised by May 22nd but were then put on hold after the start of successful negotiations with China two weeks ago. Trump appears to be taking a tough stance again to nullify domestic criticism he has gone too easy on China, but it also looks like a negotiating tactic designed to get more out of China ahead of another round of talks. The risk is that China feels it can no longer trust Trump. But solving this issue was never going to be smooth, it will take time and Trump's volatile nature along with divisions on the US side will continue to add to noise.

- Second, the commencement of tariffs on steel and aluminium from the EU, Mexico and Canada is (like all protectionism) dumb economics particularly at a time when the US is already operating at close to full capacity. But it's worth putting all these tariffs in context: steel & aluminium imports are less than 2 per cent of US imports (and less than that is affected as many countries including Australia are exempted) and $50 billion of Chinese imports are also less than 2 per cent of US imports so taken together it's a non-event compared to the 1929 or 1971 tariff hikes of 20 per cent and 10 per cent respectively that covered most imports. A proportional response is expected on steel and aluminium but it's only going to have a significant global economic impact if it triggers multiple rounds of tit for tat tariff hikes across a broad range of products. The bottom line is that while the risks have escalated we are still a long way from a full-blown trade war globally and Trump is likely wary of pushing too hard here for fear of a backlash from US workers who will have to pay more at Walmart and see their jobs go at Harley Davidson, Boeing, etc.

- Early election likely averted in Italy with the Five Star Movement and Northern League back on track to form government, but it's likely to remain messy. The Finance Minister may not be so anti-euro but the agenda for fiscal expansion and hence the likelihood of conflict with the European Union remains high. As a result, Italian bonds and shares are likely to remain under pressure for a sometime yet as investors fear that the ECB won't be able to support Italian bonds, the economic outlook deteriorates, and they worry that their investments will fall in value if Italy exits the euro. Uncertainty about Italy is likely to continue to weigh on the euro and Eurozone shares and as we saw with the Eurozone debt crisis a few years ago this can also weigh on global and Australian shares because it raises concerns about growth in the world's third largest economic block after the US and China. So Italy at just 1.9 per cent of global GDP can have an outsized impact on markets just like Greece at just 0.3 per cent did during the Grexit crises.

- However, two things are worth noting. First, ultimately Italy is likely to remain in the euro because it's too hard to leave given it would involve a sharp collapse in the value of the “new” Lira, a run on the banks, capital flight and a further sharp rise in Italian bond yields and a majority of Italians support it. But as we saw with Greece and Syriza a few years ago it can take a while (and a sharp rise in Italian bond yields) to get to this point. Second, the risk of contagion to other countries like Spain, Portugal, Ireland and Greece is now low given they are seeing stronger economic conditions, lower unemployment and reduced budget deficits and popular support across for the euro is high across Eurozone countries at over 70 per cent.

- Spanish bond yields have also seen a rise (albeit they are a long way behind Italian yields). This partly reflects misplaced contagion worries but it also partly reflects worries about the Spanish Government following a scandal and the risk of a new election. However, Spain's commitment to the euro is not at risk even if there is a change of government. The Socialists who have led the charge for a change of government support the euro, and Ciudadanos which polls suggest would gain most from an early election also supports the euro. Along with the governing People's Party these three pro euro parties garner two thirds popular support and the euro sceptic Podemos only gets around 17 per cent support. So forget about contagion from Italy to Spain.

- Trade wars, Itexit fears and the investment cycle. A big debate in the investment world is always about where are we in the investment cycle. This is particularly the case at present in relation to the US economy and share market where the cycle is more mature. A normal cycle would see growth continue at high levels, spare capacity recede and inflation and other signs of excess continue to build driving monetary policy ultimately into tight territory and setting the scene for the next major bear market and economic downswing. However, as we have seen ever since the GFC this has all been a long time coming as various events have slowed the build-up in growth and excesses. Geopolitical shocks such as a trade war or an escalation of worries around an Itexit could have the same impact in cooling growth, pushing bond yields back down and ultimately extending the day of reckoning for the global economic upswing.

Major global economic events and implications

- Another week of strong US data. Consumer confidence remains about as high as it ever gets, personal spending growth was solid in April, home prices are continuing to rise, regional business conditions indicators rose in May, the goods trade deficit unexpectedly improved in April and labour market data remains strong. The April core private final consumption deflator was unchanged at 1.8 per cent year on year but is running at 2 per cent on a three and six-month annualised basis which is right on the Fed's inflation target. This is all consistent with the Fed continuing to raise interest rates with the next move this month.

- Eurozone economic sentiment slipped in May, but it's still strong. Meanwhile unemployment came in at 8.5 per cent in April which was down from 8.6 per cent in March and May core inflation bounced back to 1.1 per cent yoy. Italian risks may not stop the ECB from starting to taper its quantitative easing program in the December quarter, but it adds to confidence that it will not be raising interest rates until second half next year at the earliest.

- Japan saw strong labour market data and a rise in consumer confidence but weaker than expected production.

- Chinese business conditions PMIs for May were flat or rose a bit consistent with continuing solid growth.

- Indian March quarter GDP growth came in at a strong 7.7 per cent yoy – surpassing China's growth rate of 6.8 per cent yoy.

Australian economic events and implications

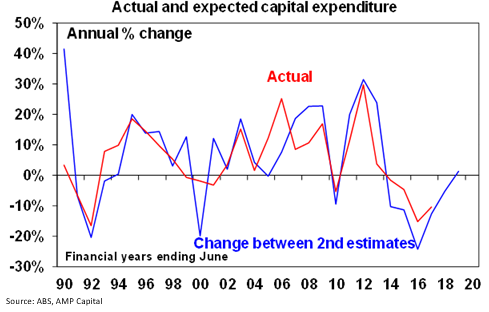

- Australian economic data was on the soft side with a fall in building approvals, continuing moderate credit growth, a continuing fall in home prices and a softer than expected rise in business investment for the March quarter. Investment plans are showing improvement, but it's gradual with investment plans for 2018-19 only up 1.4 per cent on those for 2017-18. At least they are no longer plunging though, so the drag on growth from investment is over.

- Capital city dwelling prices continued to slip in May falling by 0.2 per cent month on month and 1.1 per cent year on year. Prices have now fallen for seven months in a row and Sydney is continuing to lead the way down. Our assessment remains that home prices in Sydney and Melbourne have more downside ahead thanks to tightening bank lending conditions, rising supply, falling capital growth expectations causing buyers to hold back and slowing foreign buying. In the absence of much higher unemployment or higher interest rates, price declines are likely to remain gradual and this is also consistent with auction clearance rates which have slowed but not collapsed. Our expectations are for Sydney and Melbourne prices to fall 6 per cent or so this year, another 5 per cent next year and around 2-3 per cent in 2020. Prices in Perth and Darwin look close to the bottom and moderate growth is expected in other capitals. Overall, Sydney and Melbourne are likely to see a top to bottom fall of around 15 per cent spread out to 2020, but for national average prices the top to bottom fall is likely to be around 5 per cent.

- The increase in the minimum wage by 3.5 per cent from July will help wages growth, but only a bit. This increase is only fractionally stronger than last years 3.3 per cent rise which helped wages growth tick up from 1.9 per cent to 2.1 per cent. With unemployment and underemployment remaining very high at around 14 per cent it's hard to see underlying wages growth picking up much so our guess is that the 3.5 per cent minimum wage increase will just help keep wages growth ticking along at 2.1 per cent. Pumping up minimum wages won't jump start stronger underlying wages growth because to get that we need to see a much tighter labour market and that needs stronger growth. The risk is that it makes low income workers relatively less attractive further boosting automation and offshoring.

Shane Oliver is the Chief Economist at AMP Capital.

Share this article and show your support