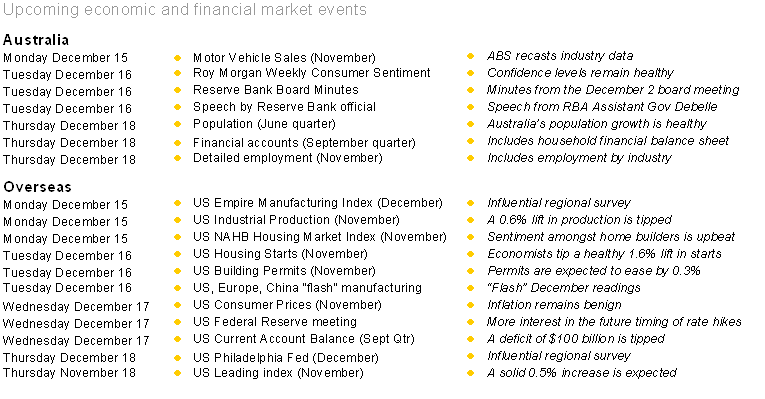

The Week Ahead

Central banks and flash manufacturing dominates the calendar

Christmas is almost upon us and while most of the top shelf economic indicators have been released, it doesn't mean that investors can rest easy. The Reserve Bank dominates the domestic economic calendar, while in the US the Federal Reserve meeting will garner the most attention. In addition flash manufacturing gauges are released across China, Europe and US on Tuesday.

In Australia, the week kicks off on Monday when the Bureau of Statistics recasts industry data on new car sales in seasonally adjusted and trend terms. The industry data revealed that 92,232 vehicles were sold in November, down 2.2 per cent on a year ago.

On Tuesday, Roy Morgan and ANZ release the weekly consumer confidence reading alongside the Reserve Bank board minutes of the last board meeting. Usually there are few surprises, but analysts will dissect the report to make sure -- particularly when it comes to comments on the Australian dollar. And to cap it all off, the Reserve Bank Assistant Governor, Guy Debelle, delivers a speech on Tuesday.

On Wednesday, November data on imports of goods is released. This is one of the timeliest economic indicators, providing insights into business and personal spending.

And on Thursday the ABS issues a number of economic indicators: the quarterly financial accounts, detailed employment data and the latest demographic statistics or population data. Australia possesses one of the fastest population growth rates in the western world at 1.69 per cent. Population growth is healthy and, in a longer-term sense, rising, underpinned by migration. If more people are coming to Australia, that means greater demand for houses, cars and retail items. Clearly faster population growth is good news for builders and retailers.

The quarterly financial accounts includes a raft of statistics such as overseas holdings of shares and bonds and the cash and share holdings of households and superannuation funds. While the detailed employment data release on Thursday will include the latest estimates of employment by industry.

Overseas: US data and global ‘flash' manufacturing in focus

In the US, the week begins on Monday with the release of the closely-watched Empire State manufacturing survey. On the same day, capital flows data, industrial production and the National Association of Home Builders index are expected. A modest lift in the builders' activity index is tipped. Industrial production is expected to rebound, lifting by 0.6 per cent in November after the 0.1 per cent slide in October. Similarly the Empire State index is expected to show an ongoing improvement.

On Tuesday, data on housing starts and building permits are released. Economists expect that starts to have lifted by 0.8 per cent in October after a sizeable 6.3 per cent increase in September. Similarly, a 0.9 per cent lift in building permits is tipped.

Also on Tuesday, the Markit organisation will release mid-month or ‘flash' manufacturing indexes for China, European countries and the US.

On Wednesday, the focus will shift to the US Federal Reserve board meeting, with the rate decision handed down 6am Sydney time on Thursday morning. While the US cash rate is not going to shift anytime soon, investor focus will be on the Janet Yellen news conference that takes place half an hour after the decision is released.

Also on Wednesday, the main measure of economy wide inflation (the consumer price index) is released. Economists expect that the CPI fell by 0.1 per cent in November with annual inflation of just 1.6 per cent -- giving the Federal Reserve ample time before needing to lift interest rates. If volatile items like food and energy are excluded, prices are likely to have risen by just 0.2 per cent in November.

On Thursday, the influential Philadelphia Federal Reserve survey, the leading index and ‘flash' manufacturing gauge are released. The usual data on claims for unemployment insurance is also issued.

Sharemarket, interest rates, currencies and commodities

There are still a couple of weeks before the end of the year and it is already clear that the number of new listings on the sharemarket have exceeded those of 2013 and likely to surpass the frenzied equity raisings in 2011 (85 IPOs). So far in 2014 (to December 8), 85 new IPOs have been recorded and another 23 are expected over the remainder of December (or in the near future). In 2013 there were 54 IPOs, while 46 IPO's were priced in 2012.

No doubt the improvement in the global economy, stronger domestic conditions and stable interest rates have contributed to lifting investor sentiment.

If you had invested and held all the IPOs this year, returns would equate to 9.5 per cent compared with 8.1 per cent in 2013 and 2.1 per cent in 2012.