The US is accelerating down the recovery road

There was more good economic news coming out of the US overnight, with industrial production surging and capacity utilisation closing in on its pre-crisis levels. It provides further evidence that the US economy maintained its momentum after the Federal Reserve finished its asset purchasing program and indicates that the economy is well placed to begin 2015 on a strong note.

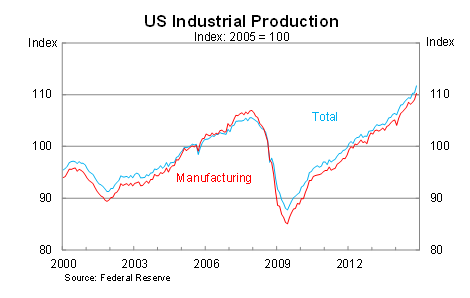

Industrial production rose by 1.3 per cent in November, easily beating expectations, to be 5.2 per cent higher over the year. In the past three months, production has increased by 2.2 per cent and is now 5.9 per cent above its pre-crisis peak.

Manufacturing production -- the biggest subcomponent -- rose by 1.1 per cent in November and is 5.1 per cent higher over the year. Mining production eased slightly in the month but has surged by 9.3 per cent over the past year.

Most of the subcomponents posted strong gains in November. Business equipment production was up 1.2 per cent; consumer goods production gained 2.5 per cent; electric and gas utilities production rose by 5.1 per cent in the month.

Obviously growth won't remain at these levels -- industrial production simply doesn't post these gains consistently in any developed country -- but it sends a strong signal about the current state of the US economy. There might remain areas of concern -- wages and productivity chief among them -- but increasingly the US economy appears poised for a breakout that could support global activity over the next couple of years.

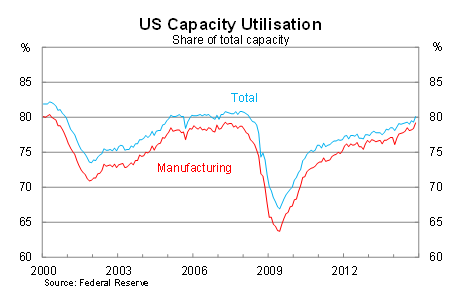

There also remains scope for production to ramp up further. Measures of capacity utilisation rose in November but remain below their pre-crisis levels, indicating that there remains significant spare capacity across the US economy.

Job creation might be running at its strongest level in around 15 years but there are still millions of Americans desperately seeking new jobs and factories and offices that are still not being utilised. This will begin to change though as the recovery intensifies; wage demands will begin to rise and high capacity utilisation will prompt greater non-residential and equipment investment.

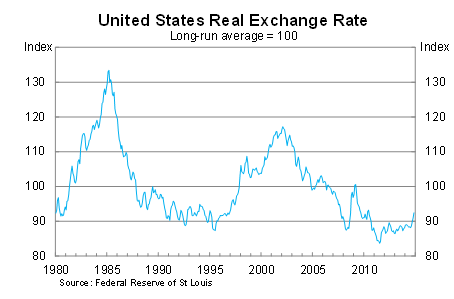

Of course, such strength -- or at least relative strength compared with major trading partners -- comes at a cost. In this case the US real exchange rate has surged to its highest level in over four years.

That's good news for US consumers -- since it directly increases its purchasing power -- but it potentially creates a stiff headwind for US companies, particularly those in vigorous competition with foreign businesses.

Australia has been a chief beneficiary of this development, with the Australian dollar falling by 12.5 per cent against the US dollar since the end of June on the back of softer commodity prices and US economic strength.

On balance, this is a very good report from the US and continues its run of strong recent data. Retail sales data released last week were also strong, while the US jobs market continues its recent good form (The jobs boom paves the way for a US rate rise; December 8).

As a result, the Federal Reserve remains on track for a rate hike by mid next year. A lot will depend on how inflation develops, it remains subdued at present, but with capacity utilisation rising and the unemployment rate falling it is only a matter of time before wage demands begin to pick up.

The higher US dollar might delay a rate hike somewhat by weighing on inflation but I still see some scope for an earlier rate rise if the US economy continues to outperform expectations over the next couple of months.