The UK's soft inflation blessing

In the UK, annual inflation fell to its lowest level in 12 years during November, with lower oil prices offering an early Christmas present for consumers. Nevertheless, the UK economy is well placed to begin 2015 on a high and should continue to grow at a solid pace over the next 12 months.

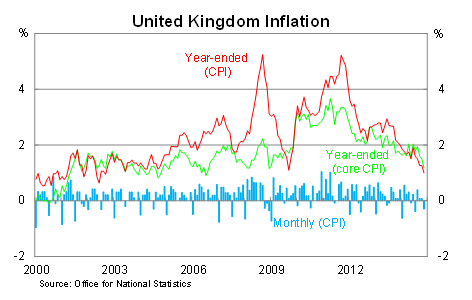

Inflation fell by 0.3 per cent in November, missing market expectations, to be 1 per cent higher over the year. Annual inflation has moderated from 1.9 per cent back in June and is now expected to dip below 1.0 per cent in the next few months.

Core inflation -- which excludes volatile items such as energy, food, alcohol and tobacco -- fell by 0.1 per cent and is now 1.2 per cent higher over the year. Similar to the headline measure, core inflation has eased considerably since June.

Most subcomponents for inflation fell during November but the general easing in inflation since June has been attributed to the rapid decline in oil prices. That has helped create inflation figures which during normal times would be viewed as dangerously low.

However, recent developments appear to be a positive for UK consumers, increasing their purchasing power, and could prove beneficial to the broader economy in the medium term.

Fuel consumption is generally fairly unresponsive to changes in prices, which means that lower petrol prices effectively make consumers richer. It's a little like receiving a tax cut.

According to the Bank of England Financial Stability Report, "lower oil prices appear likely to provide support to global activity". The main beneficiaries will be countries that, on net, import oil and that will boost real incomes. Obviously this is partially offset globally by lower incomes to net oil exporters.

The BoE does not believe that the fall in oil prices poses an immediate, significant risk to financial stability. But they acknowledge that a persistent episode of low oil prices could "impact the ability of some, such as US shale oil and gas exploration firms, to service their debt". These firms account for 13 per cent of outstanding debt in US high-yield bond markets.

From the perspective of the BoE, recent developments give it more room to move. Back in June, when annual headline inflation was running at 2 per cent and employment growth had surprised the bank on the upside, it appeared as though a rate hike by the end of this year was possible.

Obviously that hasn't come to pass and with annual inflation now well below the bank's 2 per cent annual target, it appears unlikely that the BoE will need to make a move in the first half of next year.

The outlook for inflation will be tied to a mixture of oil prices and domestic wage considerations. The former is obviously volatile but even a stabilising of prices will see inflation -- whether it be in UK, the US or even Australia -- shift back towards more normal levels.

Back in November, the BoE estimated that inflation should return gradually towards the bank's 2 per cent target (Bright prospects for the UK despite Europe's gloom; November 13). The result today does little to change that.

“We do not expect a rapid return of inflation to the target,” BoE governor Mark Carney said in November. “Although they are not permanent, the forces subduing inflation today are likely to persist for some time.”

Wages, in my opinion, remain the chief concern -- for inflation, consumer spending and the long-term health of the UK economy. Real wage growth continues to disappoint in the UK, indicating that productivity remains weak and that there is still some spare capacity throughout their economy.

On balance though, economic activity in the UK remains solid and the country appears likely to begin 2015 on a strong note. Softer inflation is probably a blessing in disguise, ensuring that wage demands are well established before the BoE begins policy normalisation. But we shouldn't expect any movement on that front until the second half of next year.