The three 2017 danger points

Robert Gottliebsen

The three 2017 danger points

Stockmarkets are basking in the glow of the likely resurgence in the US and the fact that China is not falling over. These two base trends have boosted commodity prices and miners and sent the American market to new records. And the global bull market goes further. CNN Money has alerted me to eight other markets that are roaring ahead apart from the US and Australia.

Canada – Toronto's TSX index up 31 per cent since January

UK – FTSE 100 index up 23 per cent since February

Germany – Dax up 22 per cent since February

Netherlands – AEX index up 20 per cent since February

Norway – All-share index up 31 per cent since January

Greece – Athex Composite up 50 per cent since February

Russia – Micex index up 31 per cent and RTS index up 67 per cent since January

Argentina – Merval index up 87 per cent since mid-January

Brazil – iBovespa up 66 per cent since mid-January

China – Shanghai and Hong Kong up 23 and 31 per cent since early 2016

Japan – Nikkei up 22 per cent since June

Saudi Arabia – All Share index up 28 per cent since October.

Returning to the heart of it all – the US – what is not widely discussed in the politically correct media is that a lot of talent is being paraded before President-elect Trump so it looks like he is going to be surrounded by good people, although naturally it is too early to tell.

And coming out of Trump's office are clear signals that the Trump administration is going to be a pro-business government that is going to fulfill a swag of its promises. Those promises will be led by the creation of jobs in the Middle America ‘wastelands' created by the movement of jobs out of the US.

If Trump can't deliver on this promise then the hostility in Middle America will rise dramatically because, in voting for Trump, they went against the party they normally support (the Democrats) because Trump offered them hope which no other party could.

Creating those jobs is going to mean some unpleasant encounters with Mexico and China, and Australia has a clear vested interest in the way the China negotiation proceeds. But my guess is that the whole thing will be managed without hysterics and the extra investment funded by bringing American corporate money back home, albeit it at lower tax rates. So that will make us all feel good.

Yet, we sense that we are headed into a year or two of great volatility. There will be periods, like now, where everything looks good and there will be periods where we will feel like jumping off a cliff. It is really important to prepare for this sort of volatility because if you don't you will be tempted to overextend in boom times and sell out when there looks to be no hope. So today I want to isolate three possible events that could trip up the beautiful honeymoon market we are now experiencing.

Europe's weakest link

My first pick as to a potential crisis event that could interrupt our good market times is our old friend Italy. As we all well know, the Italian economy is in a mess and in normal markets Italian bonds would be high-yielding. But European Central Bank President Mario Draghi keeps buying Italian bonds, so yields remain low. But on December 4 Italy will hold a major referendum to determine whether there should be fundamental changes to the constitution. The current Prime Minister Renzi has said that if the Italian community doesn't approve the changes he will resign. The polls say they are likely to be rejected. We have seen in Brexit and the US that pollsters are not very accurate. But Italians are famous for calling it as they see it so the polls may be correct, in which case Italy could be without a prime minister. The way will then be open for the far right movement to move into Italy and take it out of both the euro and/or the eurozone. Italy would devalue its currency and that would enable it to pay its debts, albeit in Italian currency. But Italy might also default on its loans including $344 billion owed to Germany.

All the ingredients are there for a major European crisis and, remember, if Italy runs into trouble it is a far more serious situation than Greece because Italy is in the 'too big to fail' category. The Italian sharemarket is holding but it's down about 25 per cent over the past year. Any instability among Italian banks will infect Europe and, in particular, Deutsche Bank. So Italy is my No.1 world danger point for the next six months.

Bannon and the banks

The second danger point takes us back to the US. Everyone has forgotten that during the election campaign Trump took an anti-Wall Street stance and in particular advocated breaking up the big banks by reinstating the Glass-Steagall Act. Markets were petrified by such actions, which is why there was so much nervousness ahead of the Trump election. But after the election it has simply been forgotten and everyone believes this will be a promise that Trump will ignore.

The market might be right but Trump's chief strategist is Steve Bannon, who has been a regular Wall Street critic and was very critical of the banking community over the 2008 Global Financial Crisis. As long as Bannon remains close to Trump – and there is no sign that he won't – then Trump will be regularly reminded of his promise to bust up the banks. Bank stocks are one of the leaders in the revival of the US market. JP Morgan, Goldman Sachs, Bank of America and even Wells Fargo have all done well. Once Donald Trump is inaugurated, then in his first 100 days he will make it very clear what his first actions will be and my guess is that he will set about doing them. But breaking up America's top banks will not be seen kindly by the market.

China

The third risk is of course China. Trump is going to try an accord with President Putin which will almost certainly see America back Russia's claim to Crimea and parts of the Ukraine. The Trump focus in the Middle East will be against Islamic State, and Russia and America will work together against them. But there is no such affinity with China. Indeed some of the messages coming out of America is that while Trump plans to reduce American defence outlays in Europe, he is planning to increase them in Asia.

If he goes ahead with those plans he will almost certainly move to increase tariff rates on Chinese goods, and if that happens then our stockmarket will get hit because of the likely effects on commodity exports, although the rise in the US dollar puts Trump behind the line.

My hope is that firstly none of these danger points come to pass and that no others appear on the horizon. And if that happens then global sharemarkets are set for a further big rise. But my guess is on volatility, which means that one of the above dangers (or some other danger) maybe be converted into a crisis. But the crisis will pass, so making money in 2017 will be buying shares when there looks to be no hope and selling them when everything looks good.

Readings and Viewings

As always, there were many news snippets during the week that caught our attention. Here's just a few to read and view.

The New York Times' top figures sat down with the US President-elect this week for a wide-ranging interview. Here's the full transcript. "JOURNALIST: I came here thinking you'd be awed and overwhelmed by this job, but I feel like you are getting very comfortable with it. TRUMP: I feel comfortable. I feel comfortable. I am awed by the job, as anybody would be, but I honestly, Tom, I feel so comfortable..."

The reflections on Obama's presidency have begun: “Imagine the reaction if Barack Obama had been caught in Kennedy- or Clinton-style bedroom scandals, or even if he'd spoken publicly in the style of Carter's 'malaise' speech ... Any of the above would have led to the door closing on African-American politicians at the national level for a long time, a generation maybe.”

And Democratic Party election post-mortems are in full train: "How Democrats killed their populist soul – Post-Watergate liberals stopped fighting monopoly power..."

There's now unrest in Iceland, and it's about Iceland … the grocery group.

Speaking of grocery groups, it seems little is the operative word at Lidl when it comes to employee pay. The group still has plans to expand into Australia, following Aldi's lead, we believe.

Meanwhile, New Zealand milk company Synlait has made a quiet entry onto the Australian Securities Exchange, listing on the ASX on Friday.

So has medical marijuana company Zelda Therapeutics, which raised $4 million in September.

The exclusive Medallion Fund – available to just 300 investors, scientists all – is now up to $US55 billion in profit. “Even after all these years they've managed to fend off copycats.”

A Chinese company has found a way to make money in the Chernobyl exclusion zone – a solar farm!

But oil is where the action is, especially in Nigeria with more than 200 firms bidding for a piece of the country's crude action.

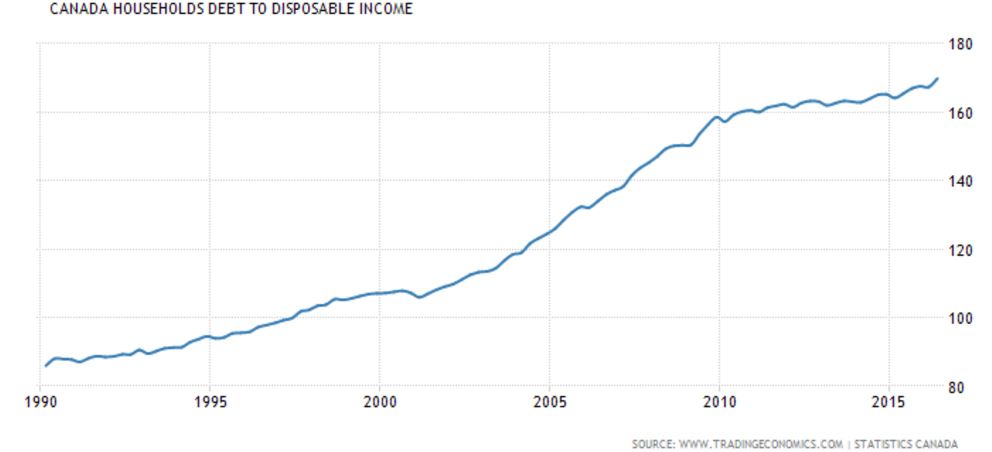

Similar to Australia, Canadians are struggling under rising private debt.

Dating apps are making us pair off on the basis of looks only: “The lack of mixed-attractiveness couples marks a troubling trend.”

A top award for single malts has Tasmania's whisky industry booming.

In 2018, Canadians could see a woman's face on their currency other than the Queen's.

But India's big-banknote ban is still not going as well as its architects had hoped.

America's first viral image – from 1863. "A century-and-a-half later, the revolting visual still steals the breath."

And lastly, Mitchell Sneddon's recipe of the week: “This is full of flavour and if you make extra green rice can be used for simple meals later in the week.”

Last Week

Shane Oliver, AMP Capital

Investment markets and key developments over the past week

The past week saw the rally in advanced country shares continue helped by good global data, rising commodity prices and ongoing optimism regarding President elect Trump's stimulus plans. The main drag is the continuing rise in the US dollar which has broken out to its highest level against an average of major currencies since 2003. Despite this emerging market shares had a bit of a bounce and commodity prices rose making the latest bout of US dollar strength more positive than seen in say 2014. Higher prices for bulks, metals and energy saw resources shares lead the charge higher in Australian shares over the last week. Despite the rising US dollar, the Australian dollar rose slightly helped along by higher commodity prices. Bond yields continued to rise in the US and Australia.

Brexit, Trump, Le Pen ... or is Europe different? Naturally after the recent experience in the UK and US which is indicative of a resurgent nationalist backlash against the pro-globalisation establishment there is a fear that Europe will go the same way. But there are several reasons for thinking that Europe is different – that a populist driven break up won't happen. First, Europe does not have the same issues with inequality that has driven the "leftist" backlash in the UK and US. It has always been well to the left of Anglo countries. Second, the maximum risk point in the eurozone was arguably just after the eurozone debt crisis a few years ago when austerity and unemployment were at their peak. Third, despite the media excitement the increase in support for the euro-sceptic populists following Brexit, Trump, etc, has not really been overwhelming. Support for Le Pen and the National Front in France has been stuck around 25 per cent. The Five Star Movement in Italy looks to have peaked in the polls and polls less than the governing party. Alternative for Deutschland only gets about 15 per cent support. Finally, support in mainland Europe for the EU and Euro is high. Perhaps the two main pressure points in Europe are the migration crisis and austerity – but the migration crisis is abating and austerity looks to be over with the European Commission even recommending recently that member countries adopt a more expansionary stance. Risks are high though and the December 4 Austrian presidential election and Italian Senate referendum could add to fears about a break up. But the evidence suggests that Europe is not the same as the UK and the US and that bouts of share market weakness on eurozone breakup fears should be seen as buying opportunities.

The soap opera about Australia's AAA sovereign rating is back on again, but does it really matter? While the surge in bulk commodity prices should boost corporate tax revenue this looks like being offset by lower personal tax collections due to lower wages growth so yet another budget blow out is possible. Meanwhile S&P has Australia on negative outlook and has warned of a downgrade if there is any further delay in return to balance by 2020-21. Given the continuous delays of recent years and Australia's continuing dependence on foreign capital the odds of a downgrade are high. But would it matter? First based on other countries that have been downgraded it's 50/50 as to whether borrowing costs would actually rise in response to a downgrade. Italy and Spain have lower ratings than Australia and yet have lower borrowing costs. And in any case if mortgage rates do rise in response to a downgrade the Reserve Bank of Australia (RBA) can always cut the official interest rate in order to bring them back down to where it wants them. In fact the main blow from a downgrade would be what it tells us about the deterioration in the quality of economic policy making in Australia.

Australian mortgage rates on the way back up? The past week has seen several lenders raise fixed rate mortgage rates. This is a natural reaction to the back up in bond yields which drive the funding costs for fixed rate mortgages. Major bank variable rates are at risk of out of cycle increases but it's hard to see them rising significantly any time soon as we don't see the RBA raising the cash rate until 2018 (see below).

Major global economic events and implication

US economic data remained solid. The Markit manufacturing conditions PMI, consumer sentiment, durable goods orders and existing home sales all rose more than expected. December quarter GDP growth is currently tracking around 3.5 per cent annualised and the US money market is now pricing in a 100 per cent probability of a December Fed rate hike.

Eurozone business conditions PMIs also rose further in November and are tracking at levels consistent with a pick-up in GDP growth to around 2 per cent. Consumer confidence also rose.

Japan's manufacturing PMI slipped slightly in November but remains well up from mid-year lows, and inflation rose, but core inflation remains very weak at just 0.2 per cent year-on-year.

Australian economic events and implications

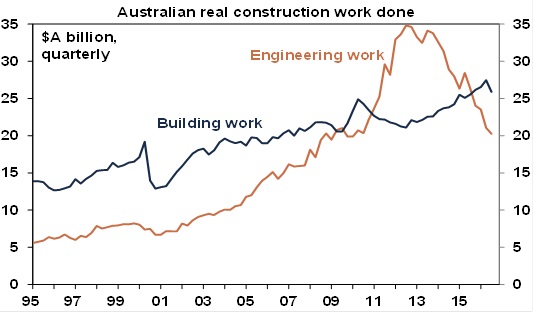

An upbeat RBA versus a possible slump in September quarter GDP growth ... what gives? Assistant RBA Governor Kent painted a relatively upbeat view of the economic outlook similar to that portrayed by Governor Lowe the week before. By contrast September quarter construction activity fell much more than expected and along with likely weak net export volumes and soft retail sales points to weak, possibly even slightly negative, September quarter GDP growth, which if reported in early December will no doubt reinvigorate concerns about the Australian economy. However, while the RBA may be a bit too upbeat I wouldn't read too much into likely soft September quarter GDP because it will be payback for much stronger than expected growth over the year to the June quarter of 3.3 per cent. And looking forward the ramp up in resource export volumes has further to go, approvals data point to a bounce back in dwelling construction and strengthening non-dwelling investment, mining investment is getting close to a bottom with engineering work back to around its long term trend (see chart), recent retail sales data have improved and the rebound in commodity prices tells us that the income recession is over. Given the possible September quarter soft patch in growth and downside risks in inflation we are still allowing for one more interest rate cut next year but overall growth is likely to be around 3 per cent in 2017 which will help set the scene for a likely RBA rate hike in 2018.

Source: ABS, AMP Capital

Shane Oliver is head of investment strategy and chief economist at AMP Capital.

Next Week

Savanth Sebastian, Commsec

Business investment and retail sales to dominate domestic interest

A new month beckons and that means the release of top tier economic data – not just in Australia but also in the US. In Australia the focus will be on the quarterly business investment survey (Thursday) and retail trade (Friday). And in the US, it is time again for another batch of jobs data (Friday).

In Australia the week kicks off on Tuesday with the weekly consumer sentiment survey. Household sentiment remains in a healthy place and should support activity in the lead up to Christmas.

On Wednesday, the Housing Industry Association releases figures on new home sales, while the Reserve Bank releases the 'Financial Aggregates' report for October, which includes money supply measures and private sector credit (loans outstanding). We expect that credit rose by 0.4 per cent in October to be up around 5.5 per cent over the year.

Also on the Wednesday the Australian Bureau of Statistics (ABS) will issue data on building approvals for October. The data represents the collated information of approvals by local councils to build new homes and commercial buildings. Given the 'lumpy' nature of apartment approvals the data does tend to be volatile.

On Thursday, the Performance of Manufacturing index, home prices and private capital expenditure data are issued. The manufacturing sector should continue to expand supported by the lower Australian dollar.

In terms of home prices, the Spring selling season is well and truly in swing. Auction clearance rates are holding at around 75-80 per cent, particularly across the eastern seaboard. In September capital city home prices rose by 0.5 per cent to be up 7.5 per cent on a year ago. According to the CoreLogic Daily home price index, Australian prices should rise by around 0.3 per cent in November. Once again it seems Sydney home prices continue be the key driver, potentially up another 1 per cent in November. Yet regional prices look to only be up just over 1 per cent over the year – highlighting the diversity of housing activity across regions.

Also on Thursday, the ABS will release the September quarter estimates on business investment. This data is also an input into the calculation of economic growth. But also insightful are the estimates of planned investment for the coming year.

Overall we expect that investment remained soft in the quarter, reflecting the ongoing winding down of the mining construction boom. However the recent surge in commodity prices – if sustained – is certainly encouraging for the sector over the medium term. The Reserve Bank will be interested in estimates of non-mining investment.

On Friday, the ABS will issue data on retail trade. Retail spending has shown some encouraging signs over the past couple of months. Retail spending rose by 0.6 per cent higher in September, to be up 3.3 per cent over the year – a four-month high. More importantly, non-food retailing has risen by 1.5 per cent in the past two months – the strongest two-month result in 20 months. Similarly a 0.6 per cent lift in spending is expected in October.

US employment under the spotlight

Most investors will be focused on the US jobs figures (Friday). But there is also key Chinese manufacturing data to digest.

The week kicks off on Monday in the US with the release of the influential regional survey on Dallas manufacturing activity. A modest lift in activity is expected for the November result.

On Tuesday, data on US economic growth, home prices and consumer confidence are slated for release. The September quarter growth reading may be revised up from 2.9 to 3 per cent, while home prices may have lifted at a 5.3 per cent annual pace and confidence is expected to rise from 98.6 to 100.0 in November.

On Wednesday in the US, the ADP national employment report is released with the personal income/spending data, Chicago Purchasing Manager index, pending home sales and weekly figures on housing finance. The ADP series will garner the most interest, give it is the fore-runner to the 'official' jobs report and is expected to show a 160,000 gain in private sector jobs in November.

Also on Wednesday, the Federal Reserve will release the Beige Book – anecdotal views on how the economy is tracking across the 12 Federal Reserve districts. The report is likely to be more upbeat ahead of the anticipated December rate hike.

On Thursday, the Challenger series on job layoffs is issued together with construction spending data, the ISM manufacturing index and the usual weekly data on claims for unemployment insurance. Construction spending is expected to have lifted by 0.5 per cent while the manufacturing gauge should show a modest improvement from 51.9 to 52.0 in November. Any reading above 50 indicates expansion in the manufacturing sector.

In China on Thursday, the National Bureau of Statistics releases purchasing manager surveys for both the manufacturing and services sectors. The private sector Caixin purchasing manager index for manufacturing is also issued.

On Friday, arguably the most important of the week's economic data is released – the US non-farm payrolls or monthly employment report. After the healthy October result – 161,000 lift in jobs – employment is expected to have strengthened even further in November, with forecasts of a lift 175,000 in jobs. Economists expect that the unemployment rate held at the seemingly “full employment rate” of 4.9 per cent. As always the interest will be in whether the tight job market shows up in higher wages.

Savanth Sebastian is an economist at Commsec.