The rates game is about to change

| Summary: Low rates are continuing to define the global economy and markets, but the game in both the US and Europe may end sooner than many expect. |

Key take-out: It's when one delves deeper into the economic data that the true growth picture emerges, and that points to limited rate rises. |

Key beneficiaries: General investors. Category: Economics and Investment Strategy. |

When you watch events taking place in the economic community that don't make sense, you know that eventually there is going to be a break.

The trick is to pick up an early signal, even though you mightn't have the timing right. About the stupidest game I have seen in my life is the current global money market high jinx that sees negative interest rates on European and other country bonds totalling $US13 trillion, and US 10-year bonds selling last night at around 1.54 per cent.

We know that the game has got to end but it now has so much momentum, and global institutions have their strategies wedded to playing the game, that it looks like it is going to go on forever. And then you see something silly happen that makes you realise that our global institutions are not all that bright, and this game may end a lot quicker than we first thought.

The US labour market statistics in August showed a rate of growth that disappointed the market and, of course, in conventional terms that means that interest rates must stay low and the expected rate increase in September is off the agenda. Future rate rises seem unlikely. A classic textbook page in the current game.

Looking behind the jobs data

But then you look a little deeper and you find that the reason why the US wages growth disappointed in August was that there was an upward blip in the number of highly paid American workers who retired. These highly paid people are often the most productive in the country (as many Eureka readers know, that is rarely recognised in Australia) and so the increase in retirement affected productivity. Once you eliminate the early retirements, wages growth was increasing roughly on track. What is happening is that the institutions are wedded to the game and don't want it to end, and so they don't look too hard at any events that tell them that the end is coming quicker than they thought.

As you all know, I have been a fan of the US growth momentum but it is slower than many expected, so I am reluctant to forecast big rises in American interest rates. I certainly don't get into a quarter-by-quarter lottery prediction game, but I think we are going to see limited rate rises faster than the market expects.

So imagine my joy when I ran across a commentary from Goldman Sachs which points out that, in its view, the normal global industrial recovery cycle of events is on track. Goldman Sachs believes that it won't be long before our banks and other financial institutions begin to accelerate leverage and increase the velocity of money because the destructive global debt deflation cycle is drawing to a close. As part of this upward trend, it says industrial metals appear to have bottomed late last year and have risen significantly.

We have also seen consistent improvement in US consumer demand. China, at the G20, underlined its determination to foster growth. That means that, contrary to the widely held view; we are set to see US rate rises and the continuation of current higher commodity prices.

I certainly don't believe that we are on the brink of any global boom, and I am not in the business of predicting the exact timing, but we all need to be aware that any turnaround along the lines Goldman Sachs is predicting will have important repercussions over a wide area of securities.

A couple of increases in the US Federal Reserve cash rate would send bond prices into a spiral and cause some considerable losses. In Europe where, perhaps surprisingly, there are also signs of a pick-up, it would damage the negative interest rate game being played by so many institutions. Losses would be severe.

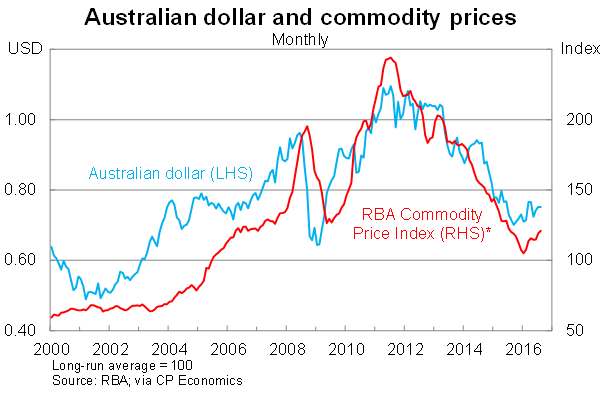

The good news for Australia is that resource exporters would increase their revenue, but the bad news is that the Australian dollar would almost certainly rise in these circumstances. I asked Eureka Report's economics commentator Callam Pickering to prepare me a graph of the Australian dollar and commodity index, and you can see they are mirror images. That rise in the dollar would not help our share market.

Moreover, the Australian share market is very much orientated towards yield and any rise in global interest rates would affect those shares unless our Reserve Bank made big cuts, which is not likely under the higher US rate scenario. And we are seeing higher GDP growth, which underlines the likelihood of no immediate rate cuts. We got a whiff of this trend over the last week when Sydney Airport and Transurban shares fell back faster than the market.

Long-term interest bearing portfolios would be affected. Because I don't think the overall rise is going to be spectacular, the damage will be on the margin, but we have been living in this low interest rate environment for a long time and what Goldman Sachs is alerting us to is that the time when it is reversed is coming closer. I should emphasise that Goldman Sachs' view is somewhat different from what the Commonwealth Bank predicted last week. I included the CBA predictions in my coverage last Saturday. The Commonwealth Bank's predictions are very much in line with world thinking, but it is important for all of us to put at the back of our mind that global conditions can change, so make sure your portfolio is not completely wedded to the CBA view of future events.

Making sense of the oil story

These days' iron ore and LNG dominate the Australian export economy. And LNG is closely linked to the oil price. All the indicators we see show us that there is an increase in the supply of iron ore coming and the Chinese look like cutting back steel demand.

BHP has been warning for some time that it does not believe that the iron ore price is set to catapult into a boom. But the oil price is a different story. Some of you might remember that last year I discussed the role of Vladimir Putin in trying to bring together the Middle Eastern oil producers to get the price up. He concluded that before there could be a coordinated approach in the Middle East, the Islamic State territory problem had to be resolved.

Putin has bought together Iran, Iraq and Syria to help eliminate the Islamic State control over vast areas of the Middle East. But Iran, Iraq and Syria are not good friends with the Saudis because the Saudi leadership is Sunni, so bringing them together on oil production is not easy. Putin arranged one deal with the Saudis at the beginning of 2016 but it fell over. Not discouraged, at the G20 he did another Saudi deal, albeit tentative. Because he has become the major Middle Eastern military power, replacing the US, in time there will be a degree of cooperation, but not until Iran brings it production close to capacity.

The Russians desperately need an oil price rise because their economy is based on the oil price. I think the Russians are going to achieve their goal and, for what it is worth, BHP has a similar view on oil. That is good news for LNG producers like Origin, Santos and Woodside.