The rate rise mirage is fading away

The Reserve Bank of Australia has maintained its neutral stance on policy but there remains considerable uncertainty surrounding the economic outlook. The perception that the bank will raise rates next year appears increasingly without merit and the economy is set for another year of below-trend growth.

The RBA monthly board minutes are often a mixed bag. They occasionally provide additional insight into the central bank's thinking but more often than not they simply communicate a dated view of the economy.

Since the meeting took place, we've had some interesting data but nothing that qualifies as a game-changer. Not that we'd expect the RBA to do much as the year winds down anyway (perhaps with the exception of introducing macroprudential policies).

So far this month we've received disappointing labour force data. The unemployment rate climbed to 6.2 per cent -- a twelve year high -- and employment growth was revised down significantly by the ABS.

Meanwhile, investor activity in the housing market continues to strengthen -- accounting for 50 per cent of new mortgages -- and is now well above the level that gave the RBA cause for concern a few months ago.

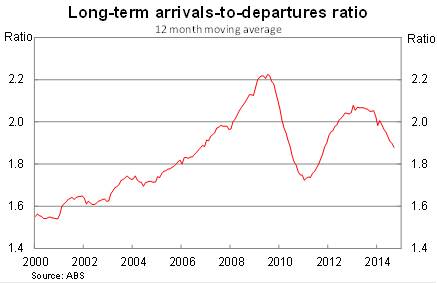

Overseas arrivals is widely considered a less important indicator of the Australian economy but it contains some interesting information. For example, migration levels continue to ease, which may not seem like a big deal until you remember that population growth has been the dominant source of real GDP growth in Australia since the onset of the global financial crisis.

Perhaps the most surprising development is that Japan is once again back in recession. That's the fourth one in the past seven years for those who like to keep track. It's not entirely their fault -- real GDP per capita or worker has performed reasonably well during that period -- but it's not a great sign for countries such as Australia where Japan remains a major trading partner.

As I noted earlier, none of these factors are necessarily a game changer but they are worth remembering. The subtle shift in our immigration rates, in particular, is the type of development that could catch some analysts off-guard.

As for the RBA, it believes that the economy is developing broadly as expected. Low interest rates continue to support activity -- particularly residential investment -- but inflation is likely to remain well within the bank's 2 to 3 per cent target band over the foreseeable future.

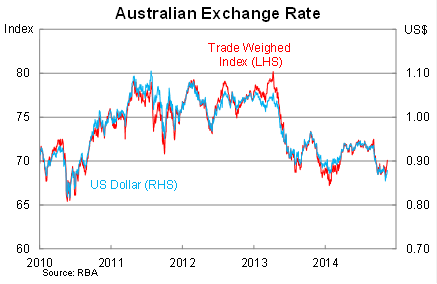

The RBA noted that “the Australian dollar remained above most estimates of its fundamental value, particularly given the further declines in key commodity prices over the course of the year to date”.

Despite recent declines -- particularly against the US dollar -- the trade-weighted index is actually higher now than it was in January this year.

I remain surprised by this given the Australian dollars' historical relationship with commodity prices -- which have declined by 13 per cent since the beginning of the year -- but that decoupling is unlikely to persist in the long-term. I still expect the dollar will fall significantly over the next couple of years but the longer this situation persists, the greater the likelihood that the economy fails to rebalance.

The reality though is that nothing is certain and there remains an unusually high level of uncertainty surrounding the RBA's forecasts. Mining investment in particular is difficult to read and could actually deteriorate more quickly than commonly believed due to a sharp fall in commodity prices.

That heightened uncertainty is beginning to weave its way into the outlook for some market economists. For months I was one of the few economists urging the bank to lower interest rates but just yesterday Credit Suisse suggested that the cash rate needed to be below 2 per cent.

Other banks, notably Goldman Sachs and Deutsche Bank, have not dismissed the possibility of a further cut. This is in stark contrast to recent months when every surveyed economist believed that the next move would be up.

The Australian economy remains in a tentative position. Risks are everywhere but the combination of weak mining investment, declining real wages and heightened unemployment makes it hard for me to believe that the bank will raise rates next year. Add in the sharp fall in the terms-of-trade and it is difficult to see the Australian economy experiencing anything besides below-trend growth for years to come.