The good news in commodities

Summary: The IMF suggests the commodities slump could hold growth lower for longer in the commodity exporting nations. But demand for commodities hasn't collapsed – all we're witnessing is a price correction. Export volumes are strong, so investors shouldn't get carried away by assertions that global trade has collapsed. |

Key take-out: While weaker commodity prices do have an impact, without an actual fall in demand (driven by global recession), they generally don't make a large or sustained hit on real growth. |

Key beneficiaries: General investors. Category: Commodities, economy. |

As I write, global markets had been taking a beating, not withstanding a modest gain on Wall Street overnight and decent gains for our market today. Although to be fair, there is nothing to say that by the time you read this, the rebound hasn't spread to Europe, or that the US will put in a strong session tonight. Swings have been huge, and as one strategist lamented “it's unpredictable chaos”. Amen.

Even so, global concerns are the worry of the moment and I've already written a number of pieces over the last month on some of these concerns. Of particular relevance for the perennially underperforming Aussie market is the commodities slump and the idea that this will smash commodity exporters. This is actually just another part of the key, dominant, macro theme currently – the China slowdown story, which is now morphing into a broader commodity/emerging market crisis story.

With that in mind, I want to take up a few points on the International Monetary Fund's (IMF) latest World Economic Outlook, which has done much to add fuel to these market concerns. This isn't unusual; the IMF did this repeatedly throughout the European debt crisis and elsewhere.

The IMF's research suggests that the commodities slump could hold growth lower for longer in the commodity exporting nations – in the emerging markets and even in Australia.

To my mind this is quite an alarmist comment and one without merit. Keep in mind, when considering any long-term investment decision, that in making that assertion, the IMF has made one critical omission. An omission that renders many if not all of its conclusions inaccurate.

The omission is that unlike previous commodity corrections, this one isn't demand induced and it isn't associated with a global recession nor higher interest rates. Demand for commodities hasn't actually collapsed – whether that be for crude oil, iron ore, aluminium or copper etc. That changes the analysis quite a bit.

All that we're witnessing is a price correction. A slump, as I discussed last week, that occurs with very little change in global economic growth conditions or prospects (see Global growth fears are unfounded, September 23). No doubt the IMF will revise down its growth forecasts soon. Despite that, global growth is actually quite healthy – bouncing around a fairly normal trend.

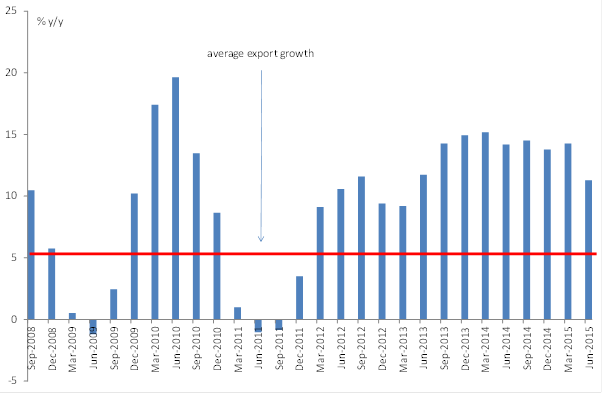

Chart 1: Demand for Australia's bulk commodities is strong (exports)

You can get a sense of what I'm saying when you look at chart 1. It shows demand for commodities – the export volumes of Australia's key bulk commodities – and shows them growing at a solid clip despite the plunge in prices.

Total export volumes are strong too and that's the same in other commodity exporting nations, like Brazil and to a lesser extent Canada. Brazilian export volumes were up nearly 8 per cent on the latest figures. Canada's up about 3 per cent.

This is why the IMF's assertions are wrong and why weaker commodities by themselves won't or can't lead to weaker growth. Yes Brazil is in recession (Canada is in a technical one, not a real one), yet that has more to do with other factors: government mismanagement, drought and restrictive monetary policy.

This is also why investors shouldn't get carried away by assertions that emerging market trade has slowed sharply, or that global trade more broadly has collapsed. In some respects that is true but that's mainly because the analysts making that claim only focus on nominal prices. Refer to chart 1 again – bulk commodity prices have collapsed yet export volumes are strong. It's the same principle when we think of global trade more broadly.

Global trade is measured in US dollars as are commodity prices. All the figures you read about to explain how global trade has collapsed are in US dollars. Naturally, when the US dollar spikes and commodity prices fall, this shows up as a huge fall in exports from commodity producing nations. And it's true to say that in nominal terms exports look woeful.

But volumes don't – volumes growth, the actual quantity of stuff exported, is doing okay. Global or emerging market trade isn't strong, granted. It is currently slower than prior to the crisis, and below the average from 1980: 3.7 per cent for 2015, versus 5.4 per cent average (world trade in total). But there is no disaster there and indeed if we are talking averages, since the GFC, global trade volumes have actually been rising by an average rate. Since the peak in 2011, commodity prices are down 47 per cent. Yet even so, world trade volumes have increased by about 13 per cent. Emerging market exports are 18 per cent higher.

That global trade has slowed a bit probably just reflects the drop off in global investment since the GFC. Yet this isn't something that is well understood. It's certainly not permanent – growth in the emerging markets, China, India and ASEAN is just too strong and the investment needs are large. At some point it will pick up and with it, global trade. Recall that the subsequent explosion of global trade from the late 1980s up to the recession of the early 1990s was driven by a surge in global investment and the extraordinary growth rates of the newly industrialised Asian economies. Those same dynamics are still at work.

So while weaker commodity prices certainly do have an impact, without an actual fall in demand (driven by global recession), they generally don't make a large or sustained hit on real growth. A temporary one at worst. Typically what you see when in a nominal price shock, where output is still strong, is a temporary hit to exporters' profits and government revenues. It's a temporary adjustment to lower prices and mitigated to the extent that the exchange rate falls. Indeed the hit to the government accounts need not even be large as the Australian experience shows – government receipts are still around normal levels, despite the commodity price slump.

For the emerging markets elsewhere, weaker commodity prices are a sizeable economic stimulus and will do much to boost growth. So in that context, the commodity price slump is unlikely to cause a crisis or weaker growth, even in the commodity exporting nations. I realise the much of the rhetoric we read and hear in no way reflects this – but lower commodity prices are very much a good news story.