The fiscal storm confronting young Australia

As if the Murray report had not put enough pressure on the government at the weekend, a new report from the Grattan Institute will add to that pressure by pointing out the growing divide in wealth, and opportunity to grow wealth, between today's older and younger generations.

The ‘Wealth of generations' report charts the end of something wonderful -- a 70-year run of strong wages growth that kept alive a pleasant example of what economists and demographers call the ‘generational bargain'.

In Australia that bargain was pretty damn good. A worker could, over the course of their life, take more money out of tax revenues in real terms than they put in, and nobody felt hard-done by.

The reason is that each retiring worker left the economy bigger, and real wages higher, than when they joined it. Thus their children and grandchildren had no problem covering their pension and healthcare costs.

As the report puts it: “The generational bargain transfers income from groups that are income-rich but asset-poor to those that are wealthy but can have limited incomes. The bargain has been sustainable because real per capita incomes have grown consistently and strongly for 70 years. Younger generations have been able to finance the retirement of older generations while also improving their own living standards.”

We are now entering a phase of Australian history in which that bargain is much less attractive to the young.

The ageing population means more wealth must be transferred up the demographic ladder, and unfortunately is likely to coincide with flat or even falling real wages in the years ahead.

On top of that, the younger generation will have to pay off the debts accumulated by Labor during the GFC, plus the new debts being accumulated by Treasurer Hockey, at a time when a lower terms of trade makes tradeable-sector goods more expensive.

Oh, and one more downer ... they've missed a once in a lifetime period of asset inflation in the housing market -- something that has transferred more wealth to older cohorts than anything else, and at the same time has pushed up the cost of living for their children more than anything else.

“Bummer dude!” -- as any young person who still has a sense of humour after all that, might say.

Why does that increase pressure on the government to act? Because, at the same time as the consolidated revenue is being dished out to older Australians in record amounts, the wealthiest among them are also enjoying record tax concessions -- plus the joy, for many who own their own homes, of receiving a pension despite owning a large asset they can leave to their children.

For young Australians in their early careers, the new generational bargain is simple: you will pay more in taxes, in real terms, than you're likely to take out.

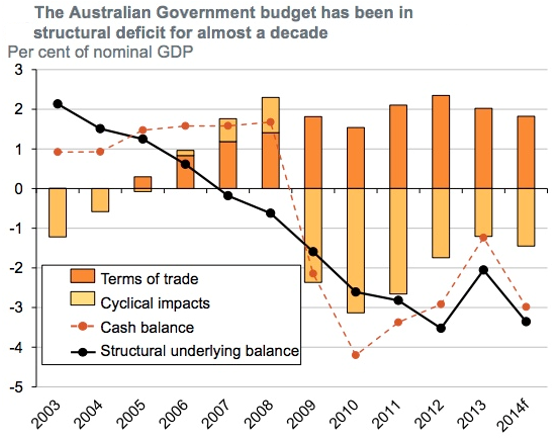

The report notes that Australia has run structural deficits for the past 10 years, and actual deficits for the past six years (see chart below). That cannot continue, because paying off those debts will soon become a significant drag on the ability of the younger generations to spend on consumption rather than on debt servicing.

So to recap, young Australians are facing a perfect storm of bad luck -- flat wages growth, a fall in the terms of trade, the end of rapid house-price appreciation, a growing number of older Australians requiring pensions and healthcare spending, and the burden of accumulated deficits.

There are three ways out of this bind.

Firstly, the young could pay a lot more taxes, though increasing the tax/GDP ratio too much starts to become counterproductive in its own right. (I have previously suggested that the Abbott government's target of 24 per cent is too low, when both the Hawke and Howard governments got to 26 per cent of GDP).

Secondly, government spending can be cut to the bone -- including the pensions and healthcare dollars directed to the oldies, but nobody wants that.

Finally, the Grattan Institute report identifies a politically fraught way to rebalance the generational bargain and make it fairer. Without actually ‘calling' for this measure, it notes:

“It is likely that large [budget] savings could be made if owner-occupied housing were included in the means test for the Age Pension, but with a government sponsored home equity release scheme for those who are asset rich, cash poor.”

That is to say, if you live in a $2 million home but receive a full pension, the government would stop your pension and replace it with an annuity that entitled the taxpayers to recoup their outlay by taking a percentage of the property's value when you've gone.

That might sound like a socialist money-grab, but in fact there are no other options other than the three listed above: the young pay more taxes than previous generations; services are slashed to the bone; or tax concessions are curtailed and housing market equity is traded for tax-dollars as described above.

Politicians will say there is a fourth option. If productivity could be increased dramatically in the years ahead, real wages could be sustainably increased too -- we'd be back to the old generational bargain.

They will say that, but it will mostly be an empty promise. As the Grattan Institute report puts it: “... while the growth of the last 70 years has set expectations, it may have been an anomaly when seen as part of a longer history.”

This government, or the next, must tackle this problem as soon as possible -- it only gets harder from here on in. Cutting government services in the way Hockey's first budget did is hugely unpopular. Raising taxes too high is counterproductive.

The other options -- reducing tax concesssion to the wealthy, reducing pension payments to the asset-rich, and finding a way to tap some of the wealth locked up in the property market -- are the only way forward.

And, as suggested yesterday, if the Coalition and Labor don't make policy inroads into this territory, it will be seized by minor parties who will offer their own generational bargain to young voters. And for older voters, that bargain could be even worse.