Stopping the shorters. The pensions pain ahead. This week and next.

Improving our communications to you

As part of InvestSMART's ongoing commitment to improving customer communications, we're pleased to inform you that we have now completed the centralisation of our member database. This change will not affect your current membership. The only change you'll notice is that, from today, all future email communications to members will be from InvestSMART.

Robert Gottliebsen

Taking the shorters to the cleaners

Three incidents really annoyed me this week - what happened to JB Hi-Fi and CSL; plus a conversation I had with a middle-aged person thinking about retirement and discovering that downsizing may be replaced by larger dwellings for older people.

The JB Hi-Fi and CSL incidents underline just how the analysts acting on behalf of the big superannuation funds simply don't understand how to look after clients. We are very fortunate in Australia to have strong self-managed funds to confine the fee gouging taking place at some large funds.

In the case of JB Hi-Fi the group announced a strong profit and the shares jumped sharply.

The reason for the big share price rise was only partly because of the results. The main factor in the rise in JB Hi-Fi shares has been the fact that earlier this year some 20 per cent of the stock was shorted.

The big Australian superannuation funds lent their share scrip to the shorters, which depressed the share price. On many occasions the capital required for the shorting comes from other superannuation funds who back hedge funds that take short positions. Long-term Eureka readers will know that I always rejoice when the shorters get taken to the cleaners. Clearly in this case those shorting the JB Hi-Fi stock had not looked closely enough at the fact that its main rival, Dick Smith, was in trouble and was set to go broke. And of course, JB Hi-Fi itself is extremely well managed.

There are a series of other companies where the shorters have borrowed share scrip from superannuation funds to smash the worth of the customers of those funds. Companies where shorters have made big plays include Myer (about 16.1 per cent of the capital has been shorted), WorleyParsons (13.7 per cent), Metcash (13.5 per cent), Flight Centre (12.3 per cent), Western Areas (10.5 per cent), Monadelphous (10.4 per cent) and Cover More (9.7 per cent). It will be good for the nation if more shorters were taken to the cleaners.

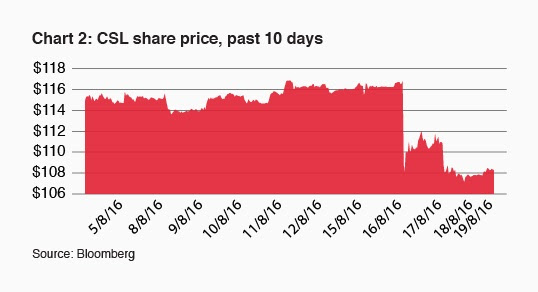

In the case of CSL there is no question of shorting, but the stock ran up quite strongly before the result, and after the result it fell. Yet there was nothing in the CSL result that should have surprised anyone. The company had told the market that 2015-16 would be a year of consolidation and, given their profit forecast, that turned out to be accurate.

The first thing that worried the institutions was that although that company had taken the opportunity to become a global leader in influenza vaccines it acquired a loss-making business and it would take time to restore the fortunes of that business and integrate it into CSL's influenza operation. CSL is quite open that although it bought the influenza business cheaply it will take five years before this business is producing strong profits. Such long-term planning is simply not on the institutions' radar and yet we need to encourage our companies to make long-term investments because that is how we will get growth into our share portfolios.

CSL has been very skilled at making major acquisitions when the market is depressed. Here it contrasts with BHP Billiton, which in recent times has made its acquisitions in the boom which then forced it to write assets down. I don't think the weak stockmarket will have any effect on CSL's long-term thinking, but a company with a lesser reputation might be put off the long-term game and not acquire a loss-making business because it will affect results for two or three years. It is important for large companies not to burn the current business, but they do need to make long-term strategic decisions. Just as our institutions play around with short selling, so too are they not being mature enough in understanding the long-term, growth stocks we have on Australian equity markets.

By the way, in 2016-17 CSL will resume a strong upward profit path because products it started researching almost 10 years ago are now coming on the market. CSL currently puts about 10 per cent of its turnover into research, and it has always been Australia's major private researcher. The institutions would love CSL to cut back its research because that would boost short-term profits. Who cares about the long term? But, as we all know, long-term share owners wanting retirement income want companies to know and plan what they are doing in the longer term.

CSL has a lot more products in the pipeline, but talking with chief executive Paul Perreault it was clear that longer term the limiting factor on CSL's growth ambitions might well be access to white blood cells. In the US, CSL has the most efficient plasma collection system in the world and this is the secret of its success. Again, it was set up by former CEO Brian McNamee in the early days of the company. CSL finds that there is a limited amount of countries where you can pay people to donate blood. For example it is very difficult to do in France and Spain.

CSL is developing a blood collection unit in Eastern Europe and Germany and its long-term ambition is to run a large blood collection operation in China. That is not a possibility at this point but the Chinese are beginning to understand the health benefits from the products that CSL produce, which are particularly important for haemophiliacs.

CSL is going to be a growth company for some time because it will be many years before the limits of its white cell production starts to hold it back.

Finally, I was yarning to a couple who are dismayed at what the Coalition government is proposing for superannuation. They simply will not be able to invest enough money into superannuation to gain a worthwhile income, so they are going to have to rely on the government pension.

But the means test for the government pension means that if they have too many assets those assets will be taxed heavily, first in conventional tax and secondly in pension reduction. The only tax shelter is the family home. If they reach 65 and decide to downsize their dwelling investment, given that the children have left home, they will then gain funds in their personal name, which will push down their pension entitlement in a horrendous way. So they have to stay in their big house and/or invest more in it, because the family home does not affect the pension.

This is a ludicrous situation and Scott Morrison needs to get someone outside of Treasury to make the superannuation reforms sensible for the retirement community and reduce reliance on the government pension.

Unfortunately the top bureaucrats in Canberra all have enormous government pensions and don't really understand what it is like not to have a government guaranteed generous indexed pension.

As I have pointed out previously, the final legislation will be determined by the Senate. Already Morrison is starting to shift his ground and is discussing raising the limit to $750,000.

Readings & viewings

In the scope of supermarket wars, there's none bigger than Aldi's 'grotesque' family feud and the billions at stake.

On the track Usain Bolt has proved beyond doubt he's the fastest man in the world. But he's also the world's fastest multimillionaire and there's no stopping him.

And, in keeping on the Olympics topic, do you think Olympic cheating and bribery are a modern phenomenon? Not so, says Julia Kindt of the University of Sydney. They're as old as the games itself.

Gold fever is gripping West Australians, but it's not the sort of gold you'd want to take home.

Australia leads the world in the decline of newsprint, said The New York Times this week. What are the implications for Fairfax Media and our democracy?

Satyajit Das is extremely worried about another banking crisis but he also has concerns about a fruitless global currency war.

The US election won't just have lasting implications for the country's politics - it has obliterated what's left of American news media.

When it comes to Uber, it seems there's no roadblocks to expansion. The supreme disruptor in the automotive space is now moving beyond its traditional road space with a heavy investment into trucking.

A long read from US asset manager Broyhill on what investors should be doing (but aren't) in this era of historically low interest rates.

Mitchell Sneddon's recipe of the week: "One more for the cold months, this maple and cider braised pork is a true winter warmer."

Happy 67th birthday to British rock icon Robert Plant. Here's the now-solo artist in vintage Led Zeppelin number, 'Black Dog'.

This week

Shane Oliver

Investment markets and key developments over the past week

Shares were mixed over the last week with European, Japanese and Australian shares down but US and Chinese shares up. Bond yields were little changed despite some Fed officials warning that a September Fed rate hike was “possible” and the US dollar fell back to where it was prior to the Brexit vote which in turn saw commodity prices rise, with oil helped by optimism of a supply cutback. The Australian dollar was little changed.

The Olympics, US elections and shares in August. It's well-known that August is a seasonally tough month for US shares with an average decline of 0.6 per cent in the S&P 500 for all Augusts since 1985. Interestingly though, in US presidential election years/Olympic years (they are the same) since 1985 US shares have seen an average 0.7 per cent gain in August. Maybe the feel good feeling of the Olympics has offset the uncertainty around the election. For Australian shares average August gains have been 0.4 per cent over the same period for all Augusts and for Augusts in US election/Olympic years.

Rethinking monetary policy or just back to the past. For the last two decades central banks have been focussed on price stability (using inflation targets) and have played the first line of defence in stabilising the economic cycle whereas fiscal policy has played back up, focussing more on fairness and efficiency for much of the time. But we are starting to see increasing discussion about whether a new approach is needed to manage macro-economic stability in a world of slower trend growth. Key aspects of this debate are about inflation targeting – whether inflation targets need to be set higher or turned into price level or nominal GDP targets – and whether fiscal policy should play a greater role. The debate is arguably not as big an issue for countries like the US and Australia but it is a big one for countries where deflation is or risks becoming entrenched such as Japan and maybe Europe. Ideally Japan needs to combine monetary stimulus and fiscal stimulus – via some form of helicopter money - to have a greater chance of meeting its inflation and growth targets without further blowing out its already huge public debt to GDP ratio. The week ahead is likely to see a heightened focus on some of these issues as the title of the US Federal Reserve's annual economic policy symposium in Jackson Hole, Wyoming over Thursday to Saturday is “Designing Resilient Monetary Policy Frameworks for the Future.”

The Australian June half earnings results improved in tone over the last week. While there was no real surprise from BHP's profit slump there have been some excellent results from stocks like JB Hi-Fi and Treasury Wine Estates. Key themes are: improving conditions for resources companies following a stabilisation in commodity prices; constrained revenue growth for industrials; ongoing cost cutting; continuing headwinds for the banks; and an ongoing focus on dividends. So far 51 per cent of companies have reported with 46 per cent exceeding expectations which is around the norm of 45 per cent. 68 per cent have seen their earnings rise on a year ago, 56 per cent have seen their share price outperform the market the day results were released and 92 per cent have either maintained or increased their dividends. While overall profits look to have fallen 8 per cent in 2015-16 thanks to the slump in resource profits, they are on track for a return to growth in 2016-17 as the slump in resources profits reverses and non-resource stocks see growth.

Major global economic events and implications

US economic data was mostly good with solid home builder conditions and another unexpected rise in housing starts, strong leading indicators and a fall in jobless claims but mixed readings from the New York and Philadelphia regional manufacturing conditions indexes. Meanwhile, there were a few gyrations around expectations for when the Fed will next raise interest rates with the minutes from the July Fed meeting presenting a relatively dovish picture but regional Fed Presidents Williams and Dudley pushing back against market expectations that look to be too dovish. While I don't see a Fed hike in September, I think it's possible if we see another really good jobs report for August, and I remain of the view that the Fed will hike in December. Against this backdrop the US money market's probabilities of just a 20 per cent chance of a hike in September and 47 per cent in December are way too low.

UK real retail sales surged 1.4 per cent in July or 5.9 per cent year-on-year, far stronger than expected. What happened to post Brexit gloom? I can understand Brexiteers feeling happy but they were only 37 per cent of those of voting age! Chinese home prices rose again in July but with slower growth for Tier 1 cities and to confuse the China bears electricity consumption rose 9.6 per cent year-on-year in July, the fastest in three years.

The Japanese economy barely grew in the March quarter as poor net exports and capex offset consumer spending and housing construction. Poor growth, core inflation sliding back towards deflation and the Yen having risen 20 per cent from last year's low point are piling pressure on the BoJ and PM Abe to do something. With the US dollar around the 100 Yen “line in the sand” a point of action could be getting near.

Australian economic events and implications

While jobs growth was much better than expected in July and unemployment fell back to 5.7 per cent, the quality of jobs growth remains poor with another surge in part time jobs at the expense of weak full time jobs. And this in turn is keeping the combination of unemployment and underemployment very high at over 14 per cent and driving wages growth including bonuses to a record low of just 2 per cent year-on-year in the June quarter. Given this and the ongoing downside risks it implies for inflation we remain of the view that the RBA will cut the cash rate again in November to 1.25 per cent. In this regard the Minutes from the RBA's last Board meeting offered nothing really new.

Speaking of interest rates, the Sydney and Melbourne housing markets are looking to be a bit more of a challenge. The perk up in finance commitments to investors, HIA new home sales and weekly auction clearance rates in Sydney and Melbourne (see chart) despite mixed readings on what home prices are doing suggest that the Sydney and Melbourne property markets may be getting a bit too hot again (at least in parts – I hear that western Sydney isn't so strong). Returning to rapid house price gains at a time when the supply of apartments is starting to surge would not be a good thing. But interest rates need to be set on the basis of what is right for the average of Australia – not just house prices in two cities so the RBA has been right to cut as the average of Australia needed it. However, pressure is likely shifting back to APRA to further tighten lending standards.

Dr Shane Oliver is head of investment strategy and chief economist, AMP Capital

Next week

Savanth Sebastian, CommSec

Spotlight on inputs into GDP figures

Domestic economic data remains in short supply. The highlight in the coming week is construction work data on Wednesday. But it is another big week for corporate earnings with commentaries on profit results and the outlook statements from major companies of interest to get a better handle on the economy.

The week kicks off on Monday with the release of the Commonwealth Bank Business Sales index – a timely measure of economy-wide spending.

On Tuesday there is an eclectic spattering of statistics. The Bureau of Statistics (ABS) issues additional data on producer prices while ANZ and Roy Morgan issue the usual weekly consumer confidence survey.

Consumer confidence rose by 2.5 per cent last week and now stands almost 4 per cent higher than a year ago. Lower interest rates, cheaper petrol prices and lack of inflation across the economy are all helping to ensure added savings for households. Confidence levels may also be buoyed by the fact that wages are outpacing prices by the biggest margin in 3½ years.

It is important to realise the decision to lower interest rates was driven by the low inflation outcomes and to some degree the Reserve Bank was cutting rates from a position of strength – with the Australian economy still recoding healthy growth. No doubt cutting rates from already record low levels is having its limitations but policymakers would be hoping that the lift in confidence last week continues over the next couple of months.

On Wednesday, the ABS issues preliminary Construction Work Done figures for the June quarter. The data covers residential, commercial and engineering construction, but it is the residential building figures which act as an input to the national accounts – that is, it assists in the calculation of economic growth figures.

In the March quarter construction work fell by 2.6 per cent, driven by a 4.2 per cent slump in engineering work and a 5.5 per cent slide in commercial building. However residential work lifted by 1.5 per cent to record highs, and that is where the focus will be. Inflation in the building sector is another aspect that comes to the fore in the data release. At present building sector inflation is growing at the fastest pace in five years, but that is being driven by outsized gains in activity last year and it is likely that inflation will moderate in line with price growth across the rest of the economy.

On Thursday, the ABS releases detailed job market data such as employment across demographic groups and unemployment rates for regions.

Bevy of housing data in the US

There is plenty to watch in the United States over the coming week with a particular focus on the housing sector. Also investor focus will be centred on the “flash” August readings on manufacturing activity in the US, Europe and China.

In the US, the week kicks off on Monday with the Chicago Fed National Activity Index. Economists expect the gauge to remain steady at 0.2 in July.

On Tuesday, new home sales and the influential regional survey – the Richmond Fed manufacturing index - are released. New home sales may have eased by around 2.5 per cent in July after lifting by 3.5 per cent in June.

Also on Tuesday the “flash” August readings on manufacturing activity in the US, Europe and China are slated for release.

While on Wednesday the focus is squarely on the housing sector. The monthly home price index is issued together with existing home sales and the weekly report on mortgage transactions – purchases and refinancing. In May home prices lifted 0.2 per cent to stand 5.6 per cent on a year ago. At present the pace of growth is healthy without being excessive.

The strength of the housing market is highlighted with existing home sales, and economists expect a 0.1 per cent rise in existing home sales to a 5.58 million annual rate in July after a 1.1 per cent gain in June. Some believe a housing shortage exists with only 4.6 months of stock on hand, below the 6-month figure regarded as balanced between demand and supply.

On Thursday, US data on durable goods orders (a key gauge of business investment) is released alongside the “flash” Markit services gauge, weekly jobless claims and the Kansas City Federal Reserve survey of business activity. Durable goods orders are tipped to have eased by 0.4 per cent in July, essentially reversing the 0.4 per cent fall in June.

And on Friday there are three indicators of note -the second reading on US economic growth for the June quarter, the advanced goods trade balance and the University of Michigan consumer sentiment index. Economists tip a modest revision with annualised economic growth of 1.1 per cent, while the final reading of consumer sentiment should lift from 90.4 to 90.8.

Sharemarket, interest rates, currencies & commodities

The Australian profit-reporting season moves into its final week with the majority of companies issuing results.

On Monday, earnings are expected from Fortescue Metals, Spark infrastructure, UGL, GWA and Bluescope Steel.

On Tuesday, Oil Search, Caltex Australia, Bradken, Virtus Health, Healthscope, SMS Management, Hills limited, Monadelphous Group and Boart Longyear are amongst those to report earnings.

On Wednesday, amongst those scheduled to issue their profit results are McMillan Shakespeare, Blackmores, APA, Qube holdings, Wesfarmers, Worley Parsons, St Barbara Mining, Codan, Shine Corporate, Qantas Airways A2 Milk, Boral and Ardent Leisure.

On Thursday, earnings include those from Iluka, AWE, Southern Cross Media, Charter Hall, Perpetual, Platinum Asset Management, Woolworths, Billabong, Nine Entertainment, South32, Flight Centre Travel, MYOB, Fantastic Holdings and Amcor Limited.

On Friday, Coca-Cola Amatil, Super Retail Group, Mayne Pharma Group and The Star Entertainment Group are amongst those expected to release earnings.

Sebastian Savanth is an economist with CommSec.