SMSFs: only millionaires need apply

Just before Christmas, the Australian Taxation Office released new statistics for self-managed super funds, detailing for the first time the full range of costs, whether tax deductible or not.

The new data indicate that in many cases, when a member switches from a collective fund to an SMSF, they reduce investment costs but incur a raft of new accounting, administration, and regulatory costs, which more than offset any savings. SMSFs are a complex product, and like buying an airfare, there are many add-ons to the base price.

In short, overall fees and costs actually go up significantly.

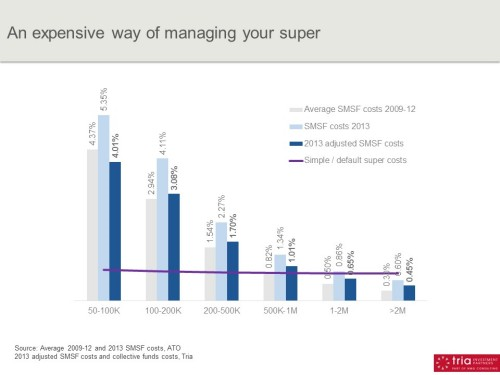

Based on this more comprehensive data, you would need a large pool of between $1 million and $2m before SMSF costs are, on average, attractive, according to consultants Tria Investment Partners.

“The price of control is high indeed,” Tria says.

The ATO estimates return on assets for SMSFs was 10.5 per cent in 2013, consistent with APRA funds of more than four members. The average SMSF member account balance is $524,000.

Claims of SMSFs being cost effective at $200,000 are dismissed by Tria consultants as “clearly rubbish”, with average costs of 2-to-3 per cent a year -- equal to, or higher than, legacy retail products. Alternatives to SMSFs, such as retail super or not-for-profit default funds average 0.8 per cent a year plus $6 a month.

The chart below reveals for 2013 adjusted average costs for SMSFs of $500,000 to $1m are 1.01 per cent. On a $750,000 SMSF, that comes to $7,538.

Source: Tria Partners

The data deducts around 25 per cent net from the ATO's 2013 SMSF costs to create a more like-for-like comparison with APRA-regulated funds. It adjusts for understatement of fees and costs in underlying structures such as trusts and other investments, as well as the overstatement of deductions for interest, depreciation, and insurance premiums, which account for around 30 per cent of SMSF deductions.

The latest ATO figures show SMSFs make up close to 30 per cent of the $1.9 trillion total superannuation assets. At end June 2014 there were 534,000 SMSFs holding $557 billion in assets, with over one million SMSF members representing around 9 per cent of the 11.6 million members in Australian super funds.

SMSF members tend to be older than members of APRA funds, with higher average balances and incomes, though the median age of SMSF members of newly established funds slipped under 50 in 2013.

As the data on the market is based on tax returns, it lags by 18 months or so. Prior to fiscal 2013, the ATO was not collecting data for SMSF pension divisions in the annual tax returns on which the statistics are based, as pension divisions are tax exempt and the costs not deductible.

So those costs for the portion of SMSF assets in pension phase were reflected for the first time in the ATO's December release. Previously, average costs of SMSFs released by the ATO appear to have been significantly understated.

SMSFs in the accumulation phase make up 63 per cent of the total, while those in the full pension phase make up 7 per cent, the ATO says.

It is interesting to note that SMSFs directly invested 78 per cent of their assets mainly in cash and term deposits and Australian-listed shares. Those with more than $2m in assets held a higher proportion in listed shares.

Of SMSFs with assets held under limited recourse borrowing arrangements, 51 per cent bought residential property.

The ATO itself notes the average ratio of operating expenses continued to decline in direct proportion to the increase in fund asset size, with the estimated operating expense ratio of SMSFs averaging $10,200.

All this clearly underscores the importance of researching all charges for advice, establishment fees, running costs, and any other charges not in the quoted fee when comparing funds.