Sluggish investment could hint at a structural economic shift

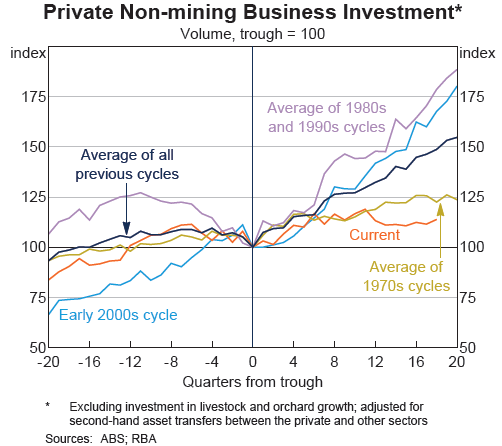

Compared with previous cycles, non-mining business investment has underperformed, tracking well below investment downturns in the 1980s and 1990s. With considerable uncertainty clouding the investment outlook one thing is clear: investment needs to get a move on or interest rate cuts are imminent.

In a recent research note, the Reserve Bank of Australia analyses the current investment cycle compared with those in recent decades. They find that this upswing -- and I use that term lightly -- has been considerably weaker than those during the 1980s and 1990s and is more in line with the average during the 1970s.

Investment downturns tend to happen at the same time as downturns in the broader economy. However, investment activity is typically more volatile than household spending or public expenditure and is often the tipping point for a tough period.

Australia is no exception in that regard and, while we haven't had a recession in 23 years, we have had a few periods when the pace of growth has slowed considerably.

According to the RBA, over the past 50 years, downturns in private non-mining business investment have lasted two years during which investment tends to fall by around 16 per cent, on average, peak-to-trough.

By comparison, investment expansions tend to last around five years, with investment rising by more than 70 per cent. There has, however, been considerable variation between episodes -- there's definitely no fixed rule on the size or length of downturns and expansions.

For example, in the 1980s and 1990s non-mining investment fell by between 25 and 50 per cent during downturns. During the 1970s, downturns saw falls of around 10 to 15 per cent.

Typically, non-residential non-mining investment suffers from less frequent downturns than non-mining machinery and equipment investment. But the magnitude of the downturns tend to be larger for the latter.

Intuitively that makes sense, since it is much easier to cease investments in machinery and equipment. Whereas with buildings and other structures, businesses often have to commit to the project early in the construction process. Either way, both forms of investment tend to experience downturns at similar times.

The same cannot be said of intellectual property, which is currently around one-sixth of total non-mining business investment. In the past 30 years, investment in intellectual property has experienced just one downturn. The increasing prevalence of computers and the internet has seen spending on intellectual property rise steady since 1980.

There are many reasons why the current episode is weaker than downturns during the 1980s and 1990s. RBA governor Christopher Kent noted earlier this year that relatively low growth and business expectations were weighing on investment activity (Why the non-mining sector is holding back on investment, September 16).

Some businesses have also been scared off due to the combination of the global financial crisis (observed through a lower appetite for risk) and until recently the high Australian dollar. It's no surprise that companies have been fairly pessimistic about the prospects for the non-mining sector.

The Australian dollar has depreciated by 12.5 per cent against the US dollar since the end of August. More importantly it's almost 8 per cent lower against the trade-weighted-index. So progress is being made, although at this point it is unclear whether the dollar has declined sufficiently or quickly enough to boost activity in the non-mining sector before mining investment collapses.

According to the RBA, firms have indicated via the bank's liaison program “that they are reluctant to commit to a substantial increase in investment until they see a sustained pick-up in sales of their products that would require them to add new productive capacity.” It's beginning to sound like a chicken and egg problem.

For other firms there is simply no need for more investment. Some firms have reported that they have sufficient capital, which suggests that the recovery in non-mining investment might not be as strong as many commentators expect.

However, we could also be witnessing a structural shift as output within the Australian economy is increasingly captured by sectors that are not capital intensive, such as the services sector, which could weigh on investment growth. As the services share of the economy rises, the non-mining investment share may ease.

Finally, the RBA notes that “the average life of capital in aggregate has increased, such that less investment is required to replace depreciated capital.” For example, capital within the services sector has, on average, a longer life than in manufacturing.

Low interest rates and a much weaker Australian dollar give us reason to be optimistic about the near and medium-term outlook for non-mining investment. However, there appear to be key structural reasons to be a little more pessimistic.

Irrespective of the reasons, the same conclusion should be reached: there is a lot at stake here. Non-mining investment is a key part of the rebalancing narrative, which so far isn't going as well as planned.

Commentators, the banks and I suspect even the RBA have cottoned on to the fact that we can't rely on the household sector -- either through spending or residential investment -- to fill the gap left by mining investment.

Exports should be reasonably strong -- hopefully supported further by the lower dollar -- but is no longer the great money-spinner that it once was. The federal budget is in a tough position and on balance I expect further spending cuts rather than stimulus.

That leaves us with non-mining investment and this will be a key narrative as we enter 2015. The dollar will help but will it be enough to spur activity within the non-mining sector? Only time will tell.