Property investors steam ahead on a second wind

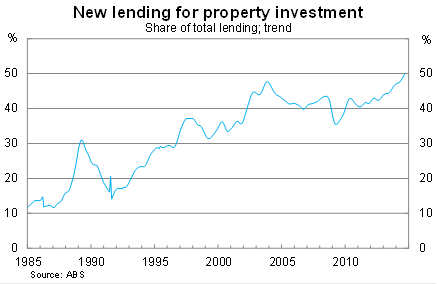

September marked a new milestone in Australia's most recent property boom: investors now account for one of every two new mortgages. Speculative activity is now at its highest level in history and is set to push higher as purchases from owner-occupiers trend lower.

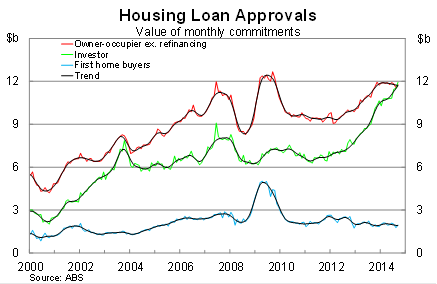

The value of loan approvals to owner-occupiers, excluding refinancing, rose by 1.8 per cent in September but is just 3.4 per cent higher over the year. Momentum within the owner-occupier segment has eased considerably over the past year and approvals have trended lower over the past seven months.

Refinancing of existing home loans remains popular -- not surprising given the combination of historically low rates and elevated mortgages -- with activity up 13.7 per cent over the year. The pace of refinancing activity is likely to ease somewhat over the next 12 months, given the limited supply of households looking to refinance, but should remain well above its long-term average.

But all attention should be on investor activity, which will dictate the future direction of house prices. The value of investor loan approvals rose by 3.7 per cent in September, to be around 25 per cent higher over the year.

More importantly, investor activity appears to have caught a second wind. Earlier in the year, activity appeared to be slowing and on a couple of occasions looked to have peaked. That has quickly changed, with investor activity rising at an annualised pace of 20 per cent in each of the past four months.

As a result, property speculation has increased to its highest level in history and now accounts for half of all new mortgages (net of refinancing). That will climb only further over the remainder of the year, given the vast discrepancy between the trend growth for owner-occupiers and investors.

Nevertheless, investor activity could sour and quite rapidly.

Investor optimism suffered its first hiccup in late September when the Reserve Bank of Australia released its Financial Stability Review (Regulators are finally bringing balance back to the housing market, September 24). That marked the turning point in speculation on macroprudential policies -- as it moved from theory towards reality.

The RBA has actively spoken out about investor activity during October and it will be interesting to see the response from investors when the data is released next month (Another RBA warning on housing, October 10).

Macroprudential policies represent a direct threat to the investor game plan. The buy and pray for capital appreciation model has treated Australian investors well over the past few decades but won't necessarily be as lucrative under lending restrictions.

The rational response by investors is to wait on policy changes before entering (or re-entering) the market. If macroprudential policies are implemented -- and are relatively harsh -- they could leave new investors holding assets that won't recoup their value for years.

That's precisely why the October data will be so interesting. It'd also answer the question: do investors consider the RBA's warnings credible? An increase in demand during October would provide a clear indication that investors are no longer listening.

The question then turns to the RBA and the Australian Prudential Regulation Authority. Are they willing to implement policies that are in the long-term interests of Australia's financial system even if it brings some short-term pain?

If left unchecked the eventual pain for investors, the financial system and, indeed, the Australian economy will only be greater. The last time investor activity approximated this level -- in Sydney during 2003 -- real house prices in Sydney declined by 17.5 per cent peak-to-trough and took a decade to recover.

Where this situation differs is that we are no longer heading into an unprecedented mining boom. To the contrary, we are facing a range of structural shifts -- such as a declining terms-of-trade and unfavourable demographics -- that all but ensure that the eventual shakeout will greatly exceed that earlier episode.