Property investors should heed APRA's warning

Investor activity has surged to new heights and the Australian Prudential Regulation Authority is watching closely. Its version of macroprudential policies compares unfavourably with those implemented by the Reserve Bank of New Zealand and Bank of England but it creates a framework from which we can safely assume it will introduce hard lending rules unless investor activity eases from its current level.

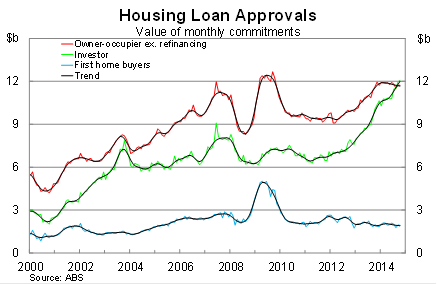

The value of loan approvals to owner-occupiers, excluding refinancing, fell by 0.1 per cent in October to be 0.8 per cent higher over the year. Momentum within the owner-occupier segment has eased considerably over the past year and approvals have trended lower over the past eight months.

Refinancing activity surged in October, rising by 3.7 per cent in the month. That's not surprising given the combination of historically low interest rates and high mortgage debt. It will be interesting to see whether refinancing activity eases somewhat over the next few months -- in anticipation of further rate cuts. The market has fully priced in a rate cut by April next year.

Activity by first home buyers eased further in October and accounted for just 11.1 per cent of loans to owner-occupiers. However, there are some ongoing concerns about data reliability. The ABS is concerned that banks are not recording FHB data adequately, leading to underestimates.

But all attention should be on investor activity, which will dictate the future direction of house prices. The value of investor loan approvals rose by a further 1 per cent in October, to be 20 per cent higher over the year.

After showing signs of fatigue earlier this year -- with trend approvals threatening to decline -- the investor segment appears to have caught a second win. That has prompted increasing concerns about the sustainability of investor activity, the implications for house prices and more broadly financial stability.

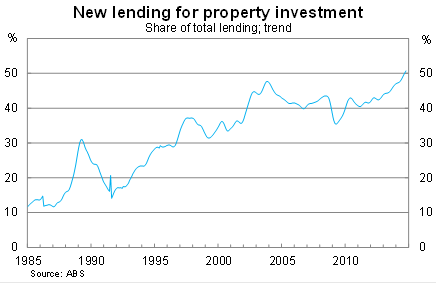

As a result, property speculation has increased to its highest level in history and now accounts for more than half of all new mortgages (net of refinancing). Based on current conditions, it appears all but certain that investors will increase their share of the market over the next three to six months.

Nevertheless, property investors face considerable risks, which and they should weigh up before entering (or re-entering) the market.

First, investor activity of this level -- or almost this level since we are now in unprecedented territory -- has historically been associated with a sharp decline in property prices. Investor activity skyrocketed in Sydney in the early 2000s but, after peaking in 2003, real house prices fell 17.5 per cent peak-to-trough and took a decade to get back to their earlier peak.

Second, regulatory authorities are not particularly keen to see this trend continue. Last night APRA and ASIC released new information regarding macroprudential intervention in lending markets.

“At this point in time, APRA does not propose to introduce across-the-board increases in capital requirements, or caps on particular types of loans, to address current risks in the housing sector,” APRA said. “However, APRA has flagged to ADIs that it will be paying particular attention to specific areas of prudential concern.”

APRA plans to focus on higher risk mortgage lending, including high loan-to-income and high loan-valuation lending; as well as interest-only loans and loans with very long terms.

They also plan to focus on lending to property investors. They believe that “portfolio growth materially above a threshold of 10 per cent will be an important risk indicator for APRA supervisors in considering the need for further action.

Finally, APRA believes that loan affordability tests for new borrowers should incorporate an interest rate buffer of at least 2 per cent above the loan product but also a floor lending rate of at least 7 per cent. This is used to assess how adequately new borrowers can service their mortgage.

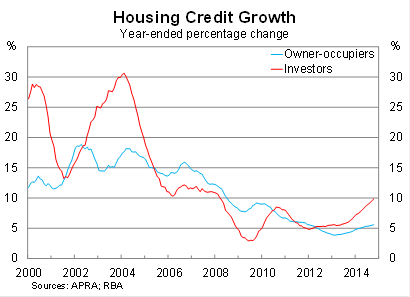

The threshold for investor lending is interesting because lending is already at that threshold -- or near enough to. Outstanding credit to investors rose by 9.9 per cent over the year to October and, given recent lending growth, is all but certain to push above that threshold by the end of the year.

Of course, APRA noted that lending had to be materially above the 10 per cent threshold and we have no idea what that means but it highlights the risk that new investors could be caught near the peak of the market with regulatory authorities directly intervening to reduce the value of their investment.

As it stands, APRA's version of macroprudential policy is much weaker than those implemented by the RBNZ and the BoE. Nevertheless, it has created a framework from which investors can predict their next move -- they can safely assume, for example, that if investor activity continues in its current vein, it is only a matter of time before APRA introduces hard rules on lending activity.