Making sense of mixed fortunes in business investment

Capital expenditure surprised the market by rising modestly in the September quarter but the outlook, while improved, remains fairly bleak. Non-mining investment is set to collapse over the next year and right now non-mining investment is in a poor position to absorb those losses.

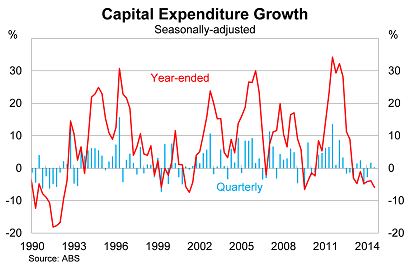

New capital expenditure rose by 0.2 per cent in the September quarter, beating market expectations, to be 5.9 per cent lower over the year. Spending has increased in the past two quarters, but is expected to deteriorate further over the next year.

Growth in the quarter was driven by ‘other select industries', which rose by 5.5 per cent in the September quarter, and more than offset a decline in both mining and manufacturing investment.

Mining investment fell by 3.5 per cent in the quarter, to be 15.8 per cent lower over the year. Manufacturing is particularly disappointing, having declined in 11 of the past 12 quarters.

It's important to note that the capital expenditure data does exclude some sectors outside manufacturing and mining. As a result, business investment in the national accounts should be a little stronger than indicated by these data.

Nevertheless, it highlights the challenge ahead for business investment. Manufacturing is providing no help -- and that won't change in the foreseeable future -- and mining is only beginning its steep descent. Total business investment is set to be weak for at least the next year and probably another couple after that.

In an odd result, the greatest contribution to growth in the September quarter came from Western Australia. Growth was also strong in New South Wales (up 4.4 per cent in the quarter) and in Tasmania (up almost 57 per cent). By comparison, capital expenditure fell by 5.5 per cent and 6.5 per cent in Victoria and Queensland, respectively.

Capital expenditure is notoriously volatile at the state level, so readers should take those results with a grain of salt. The long-term outlook for capital expenditure remains somewhat weaker in the mining states and is only expected to be partially offset by strength in New South Wales and Victoria.

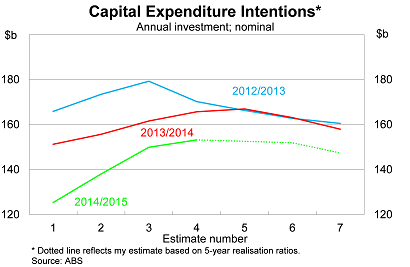

Each quarter, the ABS asks business their investment intentions for the future. This is the fourth quarter where businesses have been asked about the 2014-15 financial year. There are seven quarters of estimates for each financial year.

Based on realisation ratios over the past five years -- which basically show the historical relationship between investment intentions and actual realised investment -- capital expenditure is expected to decline by almost 7 per cent. This represents a moderate upgrade from the June quarter, when the data pointed to a decline of closer to 10 per cent.

Obviously the data is highly sensitive to the realisation ratio used and there remains considerable uncertainty surrounding the eventual drop-off. We should also remember that while there have been four estimates thus far from the 2014-15 financial year, this fourth estimate is the only one that actually contained data from 2014-15.

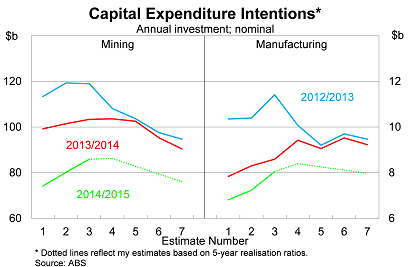

Naturally, most of this weakness comes from the mining sector but the manufacturing sector is also expected to underperform. Based on the estimates, capital expenditure by mining firms is expected to decline by around 16 per cent in the 2014-15 financial year, while manufacturing firms are set to cut investment by a further 13.5 per cent.

This will be partially offset by ‘other' sectors, which will continue to improve as the Australian economy rebalances. Capital expenditure by the ‘other' sector is estimated to rise by 8.6 per cent -- a modest downgrade on the June quarter estimate.

That creates an interesting dynamic: is the collapse in mining investment not as dire as first thought? Or potentially the economy isn't rebalancing as quickly as the Reserve Bank hoped?

The sharp fall in commodity prices -- particularly iron ore -- will weigh on investment decisions over the next couple of years. The same can be said of LNG prices. Some projects will be delayed or even cancelled due to the simple fact that prices are now 30 to 40 per cent below where investors thought they'd be when the project was tabled.

Meanwhile, the Australian dollar continues to be an impediment to non-mining investment, providing a barrier to stronger production and higher employment. The longer this remains the case, the less likely the Australian economy is to rebalance in time to absorb the hole created by mining investment.

The RBA would have mixed feelings about this release. The data is obviously weak in an absolute sense but relative to last quarter there has been a modest improvement. That said, the RBA would surely prefer that this improvement was generated through the non-mining sector because at this point, mining investment is clearly a greater downside risk and could deteriorate rapidly as firms adjust to the new reality of low prices.