LIC spotlight: Katana Capital (KAT)

Summary: Katana's portfolio managers aim to combine the best parts of a range of different investment philosophies. It focuses on Australian listed companies and ranks management as the most important factor to consider when deciding whether to invest. The LIC pays quarterly dividends and is trading at a slight discount. |

Key take out: Katana's gross returns have beaten the benchmark every year except 2013, and the fund is trying to reduce costs to improve net returns. |

Key beneficiaries: General Investors. Category: Shares. |

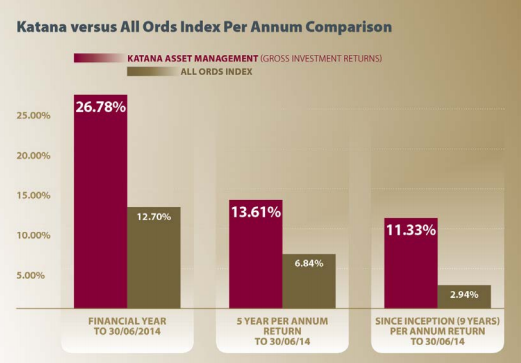

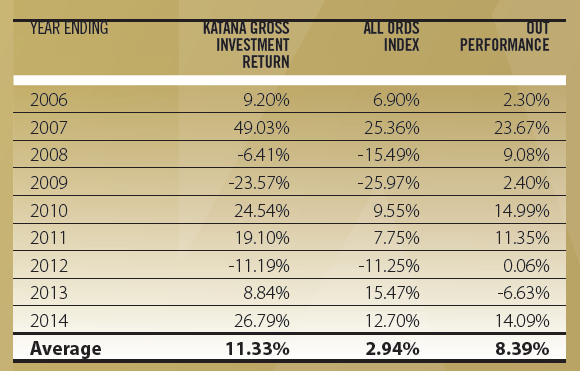

Boutique fund manager Katana Asset Management's investment philosophy is a collection of the best parts of many different approaches. This seems to be paying off, given its performance has been excellent over time in an industry where listed investment companies regularly don't outperform their benchmark. Looking at gross returns, Perth-based LIC Katana Capital has outperformed its benchmark index, the All Ordinaries, by an average of 8.39% since inception in fiscal 2006. Katana's gross returns have averaged 11.33% during that time, and the LIC has performed better than the benchmark in each year except fiscal 2013.

Source: Katana AGM presentation.

Source: Katana annual report.

Portfolio manager Romano Sala Tenna also believes that the returns are particularly strong given the fund's comparatively low level of risk. There is no gearing, a high cash balance, a general avoidance of speculative investments and a diversified portfolio that includes around 45-55 stocks, some 30 of which have a weighting of 1% or less. “Cycle in, cycle out – our returns are lower risk,” he says.

Katana aims to combine a range of different investment disciplines: value investing, fundamental analysis, growth investing, technical analysis, and market experience and observation. It seems like quite a mix, but Sala Tenna explains that each one of the fund's team of managers has a different natural disposition and background, which leads them to think and act differently.

“We're genuinely trying to apply the best precepts out of the different investment philosophies,” Sala Tenna explains. “It's increasingly a common occurrence for investment professionals to take on this multi-disciplined approach.” For example, value investing will outperform at a particular part of the cycle, but technical analysis can add value when fine tuning entry and exit points, he says.

Katana's portfolio managers Giuliano Sala Tenna, Matthew Ward, Brad Shallard and Romano Sala Tenna. Source: Katana.

Katana restricts its investment universe to Australian listed equities, and covers both small and large companies within the Australian market. Sala Tenna emphasises the fund's ability to diverge from the index. Katana has not had a position in BHP Billiton, Rio Tinto or Fortescue Metals Group since May, for example, a decision which he says would be too aggressive for an index fund.

Similarly, the fund is open to holding a high proportion of cash when the managers want to capitalise on upcoming opportunities. The fund currently holds around 32% cash. “There's enough value in the market now for us to move to 10% cash in the next few months. We're just waiting for some of these sectors and companies to find a base level.” Sala Tenna says the current weakness in the Australian market offers a good example of where technical analysis can add value, given that an understanding of price movements can help in moving with the market rather than against it.

The high cash holding means the fund is comfortable to hold its position in oil stocks, given both a long-term bullishness on oil and gas and a recent steep fall in the price of oil. “We're not going to barrel in when the market is in free fall,” Sala Tenna says. “But we can add value by buying on the way back up.”

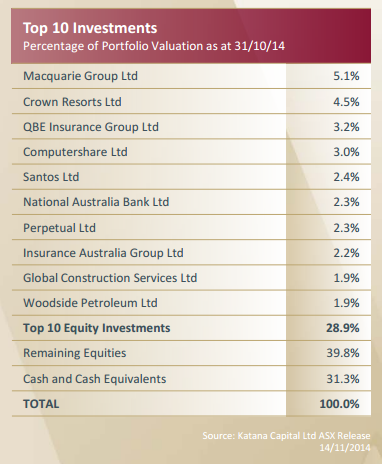

As a result, it is no surprise that the fund's top holdings include challenged oil producers Santos and Woodside Petroleum. Other top holdings include financial stocks Macquarie Group, NAB, QBE and IAG, but no miners.

Source: Katana AGM presentation.

Katana's criteria

The fund is long only and takes into account both the economic cycle and bottom-up analysis of stocks. Katana considers a range of criteria when deciding whether to make an investment, but ranks management as the most important factor. “Management is the most critical aspect, and the most difficult to assess,” Sala Tenna says. The group looks for managers that are trustworthy, competent, shareholder focused, passionate and visionary, in the belief that management decisions over a period of time will determine a company's success or failure.

Katana also looks for companies that have a robust business model and a sustainable competitive advantage, and can provide above average returns to investors over the long term. This includes patents, economies of scale, first mover advantage and regulatory advantages. In addition, Katana's criteria include a positive macro outlook, a strong balance sheet, high free cash flow, solid returns on equity and adequate liquidity.

The managers usually find companies that rate highly on one or two of their many metrics. But they particularly look for companies that overlap on different criteria, such as a business that scores highly on both value criteria and fundamentals, or one that has a good business model and a high quality of earnings. “We might have a company that's cheap and has a high growth profile,” Sala Tenna explains. “That's the sweet spot.”

Sala Tenna believes there are currently strong opportunities offshore but it does not make sense for Katana to pick international stocks. “We spend 10 plus hours a day keeping abreast of Australian companies and events.” He also notes the advantages in living and investing in the same jurisdiction, especially when information now flows so rapidly. “Trying to trade overseas markets for us doesn't make sense – even if we had time, you have to be in the time zone and react to real events,” he says. “But there are lots of ways to play offshore themes. For example, you can play the decline in the Australian dollar by buying offshore earners.”

Responding to feedback

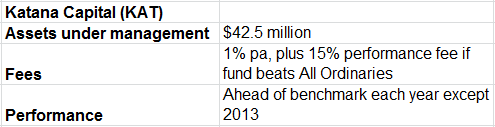

The fund pays dividends quarterly in response to feedback from shareholders, who said the frequent payouts were helpful in smoothing cashflow. Katana has announced it will pay a minimum dividend of 1.5 cents per share for each quarter during fiscal 2015. On the stock's current share price of 91 cents, this is a yield of 6.59% plus franking credits. The current share price is also at a slight discount to net asset backing, something many investors seek when evaluating LICs (see LICs with an instant yield booster, April 14).

The LIC has also reduced its fees to 1% per annum, compared with 1.25% pa previously. The performance fee has been cut to 15% of the outperformance against the All Ordinaries benchmark, compared to 18.5% previously. Sala Tenna says the fund has had a good gross return, but net returns have not been as strong as they would like. “We're conscious that we would like to get a better outcome for shareholders,” he says, adding that the fund has been “working aggressively” to reduce costs. The managers also have their own money in the fund, owning more than 16% of the funds under management, which provides another incentive to focus on returns.

Sala Tenna explains that funds under management fell during the GFC while fixed costs stayed the same, which affected the net return. Assets under management are now $42.5 million for the LIC, and under $60 million in total at Katana. Sala Tenna says the LIC is looking to grow, with a goal of reaching $100 million. “Hopefully we'll get there.”