Is Altair right about the Australian market?

|

Summary: Altair Assessment Management's ‘sell everything Australian' move has stirred the local investment community. What are the threats to the Australian market? Meanwhile, we look at retail and BHP's strategy as a growth business. |

|

Key take-out: Investors should fix their gaze on China to gauge the direction Australia is heading. Also consider that, historically, selling out of positions altogether has only caused more pain. |

Around the stock market there were vibrations this week when Altair Asset Management announced it was looking at quitting its Australian portfolio because it believed a major fall was on the horizon.

And Citi analysts went close to saying the same thing by suggesting the Australian housing market was set for a major fall.

This week I want to discuss what is worrying global institutions and the way retail investors should look at the situation. I also want to relate my experience of selling out of markets, because it is a radical step that can have long-term consequences. And, finally, I want to talk about BHP, which is one of the few stocks among the ASX 20 corporations to put up the flag and say “we are a growth stock”. That is not fashionable in this environment.

China first

So what are the factors that could really bust our market apart? The first and most obvious is a crisis in China created by its large debt. Make no mistake, if China suffers a major reversal then we will go into a deep recession because so many of our industries are linked to China. It is not just resources but also tourism, education and property.

Problems in China would almost certainly drive a repeat of what happened when Japan got into difficulty decades ago and was forced to sell its vast Australian resort property holdings leading to a big fall in values. In the case of China, the investment is in Australian residential properties where the locals have also made a major highly leveraged play.

Enough said, a big China setback is a disaster for Australia.

Not so serious, but also important, is what is happening in the US. Wall Street is priced on the basis that Trump will deliver a major boost to the US economy. If he doesn't, then American shares will fall sharply. We are seeing nervousness at the moment, which was reflected in higher bond prices early in the week.

And, leaving aside the China situation, if our housing market crumbles on its own it will hit the economy, in particularly the top four companies on our list – the banks.

Clearly the Australian economy is struggling at the moment, because our salaries are not rising. This is affecting the retail sector, but as I pointed out before, the cause of a major collapse will be more than just sluggishness in retail.

Trump's take, and the media's

The US and other global institutions have been forecasting the demise of China for a long time. It never happens. China has opened a completely new growth path with its Belt and Road program, one of the world's biggest infrastructure programs, which opens up an exciting vista.

I think there is a fair chance we will have a setback in the US because there will be delays in the planned Trump stimulations, partly caused by Russian diversions and Trump's own administrative problems. But when the market falls it will galvanise the Republican forces. So, in both China and the US, there are risks but there is no inevitability about a crash – although Trump instability worries me and there is a chance of a trade war.

Domestically, there is no doubt our housing market is clearly off its peaks. Sales are now harder to achieve, but that is a long way from a collapse. Always be wary of what you read about this in newspapers because young journalists are desperate for house prices to fall so they can get into the market and often write them. They have little understanding of the broader consequences.

Sell-outs

Moving sideways to retail investment, I was yarning to an old-time broker about the state of the sector this week who has a large number of clients in their 50s and 60s. They have no intention of selling out of the market. Nevertheless, they are what he calls “pensive”, and most unhappily for him, they are neither buying nor selling.

I think that is a good description of what is happening in the retail investment sector. There is a big reduction in the appetite for higher-risk companies, and you can see that in the share prices of middle-range companies and the panic that is created when a company issues a profit downgrade.

As my regular readers will know, when people are nervous about stock markets, I say look at your equity content and see whether it suits your risk profile, and if it doesn't, lower your equity content.

But selling out completely is another matter altogether.

I have been around a long time and in my youth I once sold everything and found it created a very difficult situation, where getting back in was a painful experience. More recently around 2007-2008, Westpac was offering 8 per cent on five-year term deposits and I substantially reduced my market exposure to invest in these deposits. This helped keep me calm through subsequent market difficulties, but when the deposits matured, interest rates had fallen and shares had recovered, so again it was a difficult adjustment. For older people it is important not to be overexposed to the stock market in tumultuous times because it can affect your health.

Back to BHP

Now to BHP. Elliott Management wants it to operate with one listed vehicle – BHP in Australia – and wants it to float off its oil interests or at least its US shale oil interests. This has caused BHP to have a good look at itself, and it is now really turning to shareholder value.

Quite obviously, if there is a major market collapse, BHP will be hit and, in particular, it is concerned about a decrease in world trade. But the mining industry is beginning to use technologies to improve the way mines are managed, so BHP has more than halved its costs per tonne in WA iron ore and is still looking to go lower. It believes with a passion that the Belt and Road program in China, plus the transformation of India, will underwrite demand for its base products in the next decade. And, as discussed previously, BHP is a bull in the oil market.

In shale oil, each well is a short-term exercise (usually two or three years), so it is possible to forward sell the expected production and lock-in the returns from each well assuming costs are on budget. It is a unique business if you manage it correctly.

It is a long time since the big Australian announced that it was a growth company – it is aiming at a 50 per cent rise in base value. There are very few growth stocks among the top companies on the ASX.

I believe BHP will follow up its current advertising campaign by opening up completely new channels of communication with smaller shareholders to convey the long-term message. The trouble is, with most institutions, long-term is 12 months, so the long-term BHP growth message could hold no relevance. But for retail shareholders, long-term growth is important.

Last Week

Shane Oliver, AMP Capital

Investment markets and key developments over the past week

Share markets generally rose over the last week helped by reasonable economic data and expectations central banks will remain benign. Eurozone shares were the exception and saw a slight fall on worries about an early Italian election. Bond yields were little changed, but commodity prices mostly fell and this along with weak Australian data weighed on the $A.

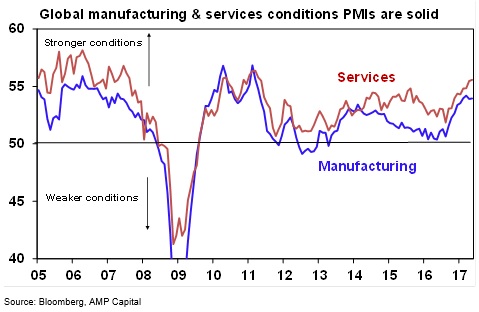

Are things so bad equity managers should hand all their funds back to their clients as one Australian manager is reported to have done? Putting aside speculation around other issues that may have driven the decision there are several points to make in relation to this. First, shares globally are at risk of a correction but the combination of improved growth including solid business conditions (see the next chart), rising profits, okay valuations and low interest rates indicates the broad backdrop is reasonable. Second, risks remain around China but they have long been there and there is no indication it's suddenly about to fall over. Similarly, I am expecting a pullback in Sydney and Melbourne property prices and the Australian economy remains weak but it's doubtful that it's on the edge of the abyss. Fourthly, over the years there have been numerous high profile calls to “sell everything” or “gear up big time for the great boom ahead”. Some get lucky but many not, the point being that it's dangerous to bet everything on one big call. Finally, individual fund managers are usually chosen to fill a role in a portfolio of assets which has been carefully constructed to meet investment goals over time with the expectation that each fund manager will manage the assets in their care in line with their process and views. So if one manager decides to give the money back the manager of the whole portfolio – be that a financial planner, super fund or individual - will invariably just have to find another manager to fill the gap.

President Trump's decision to leave the Paris climate agreement will have little short term impact on markets but poses a longer term negative for the US (and for global warming). Short term it's of little consequence for investment markets. It will take time for the US to exit and several key US states (notably California) will uphold the Paris agreement and more anyway. Longer term it's another delay in doing something about climate change and the US will pay some price as the rest of the world pushes faster towards renewables leaving the US behind. Of course, the next US President will likely sign up again but the delay is not helpful.

Just when it seemed "Eurozone break up risks" would be quiet for a while there is renewed talk of an early Italian election. Their next election is due by May next year but signs of agreement on electoral reform and a desire on the part of the governing Democratic Party (PD) to get an election out of the way before a contractionary budget due later this year have raised again the prospect of an early election around September-October. With the populist mostly anti-Euro Five Star Movement (5SM) tied in the polls with PD, there is a good chance that it will win the most seats. However, it's doubtful 5SM will be able to agree a coalition with the right wing Eurosceptic Northern League (which at times has advocated a break up of Italy). In which case Italy will revert to a coalition involving the current government and the idea of Italy leaving the Euro will recede again. None of this will stop markets from worrying about it in the interim. But one thing that helps fade the risk of a Eurozone break up though is that the elections in Europe since the Brexit vote have seen the rejection of anti-Euro parties suggesting the risk of Italy setting off a domino effect across Europe of countries seeking to leave the Euro is low. As such we remain upbeat on Eurozone shares.

Major global economic events and implications

US data was mostly good with a solid May manufacturing conditions ISM, consumer confidence down a bit but still very strong, solid gains in personal income and spending in April, strong labour market readings and continued increases in home prices. Core personal consumption deflator inflation fell to only 1.5 per cent year on year in April highlighting that inflation remains weak and pointing to a continued gradual monetary tightening process from the Fed.

Similarly Eurozone core inflation also fell in May back to 0.9 per cent yoy which explains why despite stronger activity data including another decline in unemployment and strong confidence readings ECB President Draghi remains dovish.

Japanese data remained mixed with strong labour market data, industrial production and a rise in the manufacturing conditions PMI but weak household spending. Depressed wages growth remains an ongoing constraint.

Chinese business conditions PMIs were confusing in May with stronger services conditions, a flat official manufacturing PMI but a further decline in the Caixin manufacturing conditions PMI. Averaging them out suggests stable growth after the slowdown of the last few months.

Australian economic events and implications

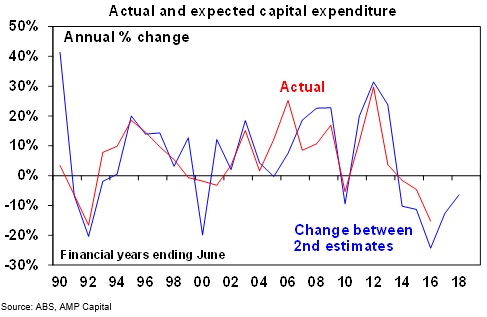

Australian data over the last week was messy. Building approvals bounced but the trend remains clearly down. Retail sales bounced in April allaying fears for now of a consumer collapse and setting up a stronger June quarter, but the bounce looks partly due to better weather and the timing of Easter and the consumer remains under some pressure. Business investment was flat in the March quarter, mining investment looks like it's getting close to the bottom and investment plans point to a slowing in the pace of decline in business investment but it's still falling (see the next chart).

Our estimate for March quarter GDP growth remains 0.1 per cent, but given normal forecasting errors a negative outcome is a very high risk. With consumers under pressure and the impact of Cyclone Debbie on coal exports risking a negative June quarter there is a possibility of a technical recession. Of course solid forward looking jobs indicators, a slowing drag from falling mining investment and strong public capital spending all argue against getting too gloomy, but the overall picture is one of sub-par growth running well below that assumed by the RBA and in the Budget. In our view this all points to the rising risk of another interest rate cut, a continuation of the relative underperformance of Australian shares compared to global shares that started in 2009 and a break in the value of the $A below $US0.70.

On the house price front, CoreLogic data for May adds to evidence that the peak at least in terms of momentum has been seen. The drip feed of negative news regarding the Sydney and Melbourne property markets - bank rate hikes, APRA moves, surging unit supply, tightening conditions for investors and foreign buyers (with NSW moving again on foreign buyers in the last week), constant warnings of a bubble about to burst - is starting to impact. Overall our view remains that the peak in home price growth in Sydney and Melbourne has been seen and that further weakness lies ahead with ultimately a 5 to 10 per cent average decline and that unit prices in parts of Sydney and Melbourne will fall by 15-20 per cent. In the absence of much higher interest rates, much higher unemployment and a generalised oversupply a property crash (say a 20 per cent plus fall in average home prices is unlikely). Of course it's dangerous to generalise across Australia – Perth property prices are probably getting close to the bottom and Brisbane and Adelaide prices are likely to continue meandering along at around 3 per cent year on year.

Shane Oliver is head of investment strategy and chief economist at AMP Capital.

Craig James, CommSec

Autumn avalanche: Plenty of economic covfefe

- It is a quirk in the economic calendar that each new season gets ushered in with a barrage of economic data. So to the ‘autumn avalanche'. Around a dozen key indicators or events are scheduled for the coming fortnight.

- In Australia, the week kicks off on Monday with the release of the “Business Indicators” publication from the Bureau of Statistics (ABS). The publication includes data on sales, profits, inventories and wages.

- Profits rose sharply in the December quarter with “company operating profits” rising by 20.1 per cent to a record high of $77.8 billion after rising 1.5 per cent in the September quarter. Profits are up 26.2 per cent over the year. Profits may have lifted a further 10 per cent in the March quarter.

- Also on Monday ANZ releases data on job advertisements while the Melbourne Institute inflation gauge and the Performance of Services index are also issued. Job ads rose by 1.4 per cent in April to be near 6-year highs.

- On Tuesday the Reserve Bank Board meets. No change in interest rate settings is expected. And the commentary accompanying the decision is likely to be very similar to that of the previous month. It would be interesting if comments were made on fiscal policy settings after the recent Federal Budget.

- In terms of economic data on Tuesday the weekly consumer confidence data from ANZ and Roy Morgan is released together with the balance of payments and government finance figures.

- Confidence levels have risen for four out of the past five weeks however it is clear that Aussie consumers are just feeling OK at present. The confidence index is still a little below longer-term averages but well above the 100 line that separates confidence from pessimism.

- The balance of payments data includes the current account – the broadest measure of Australia's international trade position. And for the first time since the mid-1970s, Australia may have recorded a current account surplus. In fact a $200 million surplus would be the biggest surplus in 44 years.

- The data also includes estimates on net exports (exports less imports). And together with the government finance data, the figures will be important inputs into the economic growth equation.

- On Wednesday, the March quarter economic growth estimates will be provided. And at this early stage we expect that the economy grew by around 0.5 per cent in the quarter to be up 1.8 per cent on the year. Australia is in the midst of the world's longest economic expansion in the modern era.

- On Thursday, the international trade data for April is released. And the run of surpluses is set to continue with the Commonwealth Bank Group tipping a surplus of $2.3 billion.

- And on Friday, housing finance data is released by the ABS together with the broader lending finance data. And by all accounts the tighter lending policies are having the desired impact with the number of loans for home owners expected to have fallen by 2 per cent in April while the value of all home loans may have been flat in the month.

Overseas: A quiet week ahead in the US

- An unusually quiet week is in prospect for key US economic data. There is more interest in China with inflation and trade data to be released late in the week. And all eyes will be on Thursday's UK election.

- The week begins on Monday in the US with the ISM services index due for release with factory orders, the employment trends index and the quarterly labour costs and productivity data. Economists tip a slight pull-back of the ISM services index from 57.5 to 57.1, remembering a reading above 50 indicates expansion of the sector. Labour costs may have grown at a 2.5 per cent annual rate with productivity largely unchanged.

- In China on Monday the private sector Caixin services index is released.

- In the US on Tuesday the JOLTS job openings index is released together with the usual weekly data on chain store sales. Job openings hit an 8-month high of 5.74 million in March and are not far from record levels, suggesting a healthy job market.

- In the US on Wednesday the usual weekly data on mortgage applications is released together with data on consumer credit. Credit has largely been trending sideways in recent years.

- In China on Thursday the May trade data is released while on Friday inflation figures are due for release. The trade data has proved a little volatile in recent months but in April imports were up nearly 12 per cent on a year ago with exports up 8 per cent. The trade surplus stood at just over US$38 billion in April.

- Business inflation (producer prices) is coming off recent highs with annual growth at 6.4 per cent, down from highs of 7.8 per cent in February. But non-food consumer prices in China have been on the rise with the annual growth of 2.4 per cent not far off the fastest rate in 6.5 years.

- On Thursday in the US the usual weekly data on claims for unemployment insurance is released. And on Friday in the US, the April data on wholesale sales and inventories are due for release.

Financial markets

- In the past decade, the All Ordinaries index has risen only twice in the month of June. The index rose by less than 0.1 per cent in June 2012 and you have to go back to June 2009 to find a 3.5 per cent increase. The months of June, September and November have traditionally been the worst months for Australian shares.

Readings & Viewings

This week was relatively quiet on the ballistic missile front, although Russia's strike into Syria did make headlines.

But the question is, does Elon Musk have more rockets than North Korea? We may never know, but the billionaire is no stranger to crash and burn incidents either. Here's a look at his career.

Meanwhile, as if they didn't already get the point, Amazon is again showing book stores just how it's done.

It's all a bit messy, but Uber has fired its star engineer, and its finance chief is taking off.

Support the engineers. One from Amazon is trusting the internet with $50,000 of his own money. We can't play in Australia, but can follow his game here.

Walmart is taking Amazon lying down. It's asking its employees to deliver parcels on their way home.

Let's hope they're not driving a German one. Donald Trump is upset over German cars, and he wants to make it harder to buy them.

What covfefe? In case you missed it, Donald Trump is reinventing the English language.

He had better watch out. It seems Bernie Sanders is still on the presidential campaign trail.

Is the US housing market overheating already? Billionaire's Row in New York is seeing its first foreclosure and Florida home price increases beat the national average. But don't be calling it a bubble.

If you're planning on heading to the swamp, make sure you pack these shoes.

The state of Ohio is suing big pharma over the opioid crisis.

Here's an excuse to buy more chocolate.

For tech geeks, which is everyone these days, Mary Meeker released her annual internet trends report. More talking than typing, lots of Netflix, and gaming hits the mainstream.

Netflix is actually wielding its production axe, and we should expect more shows to vanish.

Lastly, this IPO is designed for lazy people. Is this a growing start-up trend?