Investors gain amid residential pain

Summary: Rising house prices have put a smile on the faces of many property owners but that is balanced against tighter regulatory conditions and lending standards and recently out-of-cycle mortgage rate hikes by the major and minor banks. |

Key take-out: Investors should be unperturbed – even encouraged – by proposed responses to Australia's housing affordability woes. But they might want to consider other dynamics in the residential property space, such as debt levels and credit streams. |

Key beneficiaries: General investors. Category: Residential property, economics. |

Residential property is not only a key component in the portfolios of thousands of Australians, representing over half of household wealth, but it's also a key mechanism through which monetary policy affects the broader economy.

Individual investors mainly concern themselves with the profit and loss on their investment properties, the yield they can earn and whether they will take advantage of negative gearing. The Reserve Bank of Australia, by comparison, has a much broader interest in the health of Australia's $6.2 trillion property sector.

We know that Australian households are among the most indebted in the world. We also know that Australian house prices are expensive by global standards. But is this cause for concern?

Newly minted RBA assistant governor Luci Ellis gave an interesting and far reaching speech on ‘Housing and Inequality' last week in Melbourne. Housing affordability, a key part of any discussion on inequality, has been a key political issue in recent years and Ellis offers some insight into both prices and debt.

When it comes to analysis on the housing market it is quite common for analysts to refer to ‘median' or ‘average' outcomes, but those are often uninteresting or misleading. The systemic risks associated with housing never come from the median or average household. Similarly, housing affordability is not often a concern for the median or average household.

Ellis focuses on the distribution behind property prices, ownership and debt. If knowledge is power, then an understanding of the forces behind the property market is an important tool for the savvy property investor.

From the outset it should be made clear that Ellis' speech refers mainly to home ownership rather than investors, per se. However, since the family home represents the biggest and most important investment for most households I think the analysis warrants some consideration even if Ellis doesn't address investment housing directly.

It may also have some relevance since many readers may be thinking about helping their children buy their first home or investment property.

A policy vacuum

Home ownership rates have fallen for most age groups over the past three decades. The decline has been most pronounced among those between the ages of 25 and 44 years of age. This is the group for whom housing affordability has the most relevance; they are the group that is likely to have just entered or is planning on entering the housing market.

Available data suggest that home ownership rates have fallen further since the 2010 Census. The second graph below, based on data from the Household, Income and Labour Dynamics in Australia (HILDA) Survey, indicates that ownership among 25-34 year-olds has fallen below 40 per cent, while ownership among 35-44 year-olds has dropped to below 60 per cent.

Ellis isn't particularly concerned about this development, noting that “many people wait to settle down before they buy a home”. Certainly the Federal Government doesn't appear too concerned despite the occasional lip-service.

Federal MP Michael Sukkar, charged with finding solutions to housing affordability issues, recently said that young people needed to get a “highly paid job”. It echoes comments made by former treasurer Joe Hockey. Unfortunately, that is an oversimplification and an unhelpful one in an environment where full-time employment is falling and wage growth is at its lowest level in a quarter century. Australian wages are some of the highest in the world and that has done little to reduce ownership rates among younger people.

Details are scarce, but some MPs are urging the Federal Government to pursue ‘affordability' measures that could actually prove lucrative for existing owners and property investors.

The proposal to allow young Australians to access their superannuation to fund a deposit is straight out of the first-home buyers' handbook. It will push prices higher across the board and encourage younger Australians to take on more debt. It wouldn't help housing affordability, since it would create artificial demand, but it would be beneficial for existing home owners and investors.

Meanwhile, the MPs propose allowing retirees to downsize their existing home without affecting the assets test for the purpose of receiving the aged pension. For asset-rich retirees this would prove lucrative.

Debt-to-income considerations

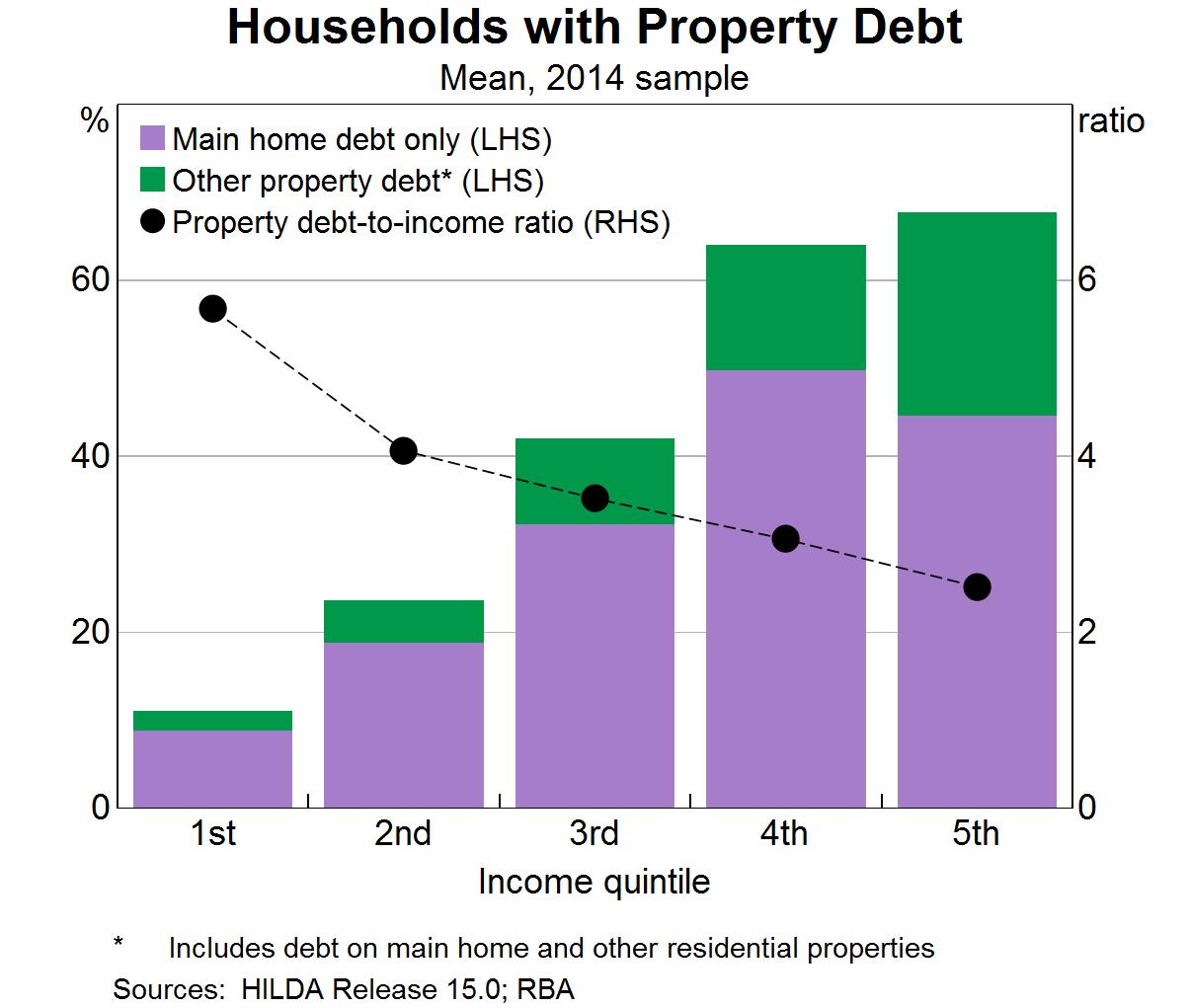

Returning to Ellis there is, however, good news for those concerned about the level of household debt. Household debt is undeniably high, but it is generally held by higher income earners. High house prices, by crowding out first home buyers, have ensured that those in the housing market are often well placed to manage their mortgages.

The graph below also shows that the highest income earners tend to be those that also hold ‘other' (or investor) property debt. These loans are frequently ‘interest-only' and are considered riskier than standard loans – though lucrative for investors – so it is comforting that those taking on these loans are well placed to manage such risk.

Nevertheless, property debt-to-income tends to be higher for lower income households. They may not hold as much debt but there is greater risk of default associated with that risk.

Deposit blues

“Much of the commentary around the difficulty of achieving home ownership centres on the task of accumulating the deposit,” said Ellis.

This isn't exactly true. The biggest issue with housing affordability is raising a deposit, but the commentary largely focuses on whether it is difficult or not to pay interest. Even the RBA, via its regular charts and updates, focuses on interest payments rather than deposits.

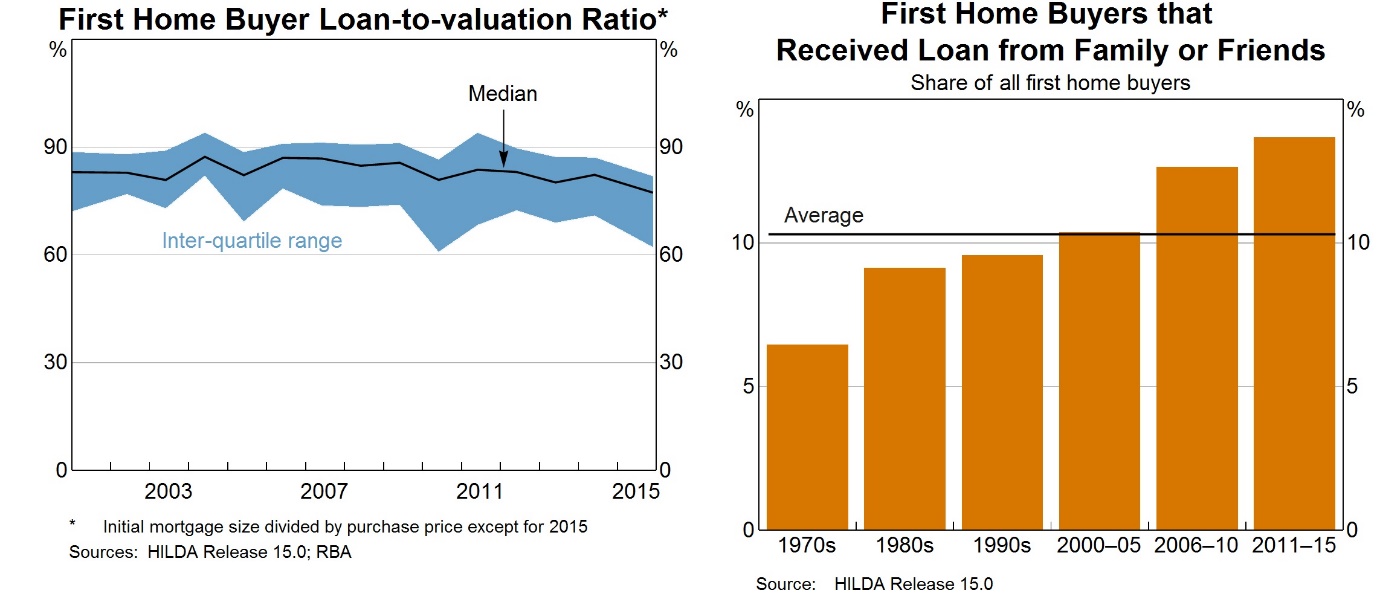

The data on deposits suggests that the average loan-to-valuation ratio for first home buyers has actually declined somewhat in recent years. That is, first home buyers are entering the market with higher deposits than they have in the past.

“It's not entirely clear why this is,” said Ellis. “And because a high loan-to-valuation ratio does imply higher risk both for the borrower and the lender, it might not be such a bad thing.”

Increasingly first home buyers are relying on the bank of mum and dad to put their deposit together. Although the share of first home buyers receiving direct help is relatively low I'd expect that has increased in recent years due to the large rise in house prices in Sydney and Melbourne.

I have maintained for some time that the current environment is an interesting one for home owners and investors. Rising house prices have surely put a smile on the faces of many property owners but that is balanced against tighter regulatory conditions and lending standards and recently out-of-cycle mortgage rate hikes by the major and minor banks.

Ellis doesn't appear particularly concerned by developments in home ownership or the accumulation of debt. There is certainly a social or composition aspect to these developments, particularly in how they have evolved over the past two decades. Yet, more recently, it has become difficult to see how price growth has been consistent with wages or economic activity.

Investors obviously need to make that assessment as well. The analysis by Ellis should bring some comfort; as would the policies discussed by the Federal Government that are unlikely to address affordability and may, in some cases, push property prices higher.