Investors cash in on the other property market

|

Summary: Self-directed investors, including SMSFs, are investing heavily into unlisted commercial property to take advantage of attractive yields and capital growth. There's also heavy activity taking place as trustees undertake in-specie transfers of units ahead of the new $1.6 million pensions cap. |

|

Key take-out: There is an increasing understanding and awareness of the benefits of unitised commercial investment grade property. |

Australia's residential real estate market may be cooling in spots, but then there's that other property market where investors are still enjoying pretty good returns.

In the scheme of total investor inflows, the commercial office sector is very much the poorer cousin of the $2 trillion residential property market dominated by housing and apartments.

But savvy retail investors, including self-managed super fund trustees, are behind increasingly strong capital inflows into unlisted commercial property syndicates and unitised office property funds.

What's the big attraction? It's mainly about yield and risk really, with investors able to tap into relatively secure and stable income streams that in some cases are delivering pre-tax returns above 6.5 per cent. Adding on capital growth of around 3-4 per cent, linked to incremental tenant rental increases, some investors are achieving annual total returns above 10 per cent.

Of course, that's not a given. To get the best returns, and effectively reduce risk, investors need exposure in the right locations. That means buying into A-grade commercial real estate, in areas experiencing strong growth, and preferably into properties leased to blue-chip tenants locked into long-term lease contracts. But buying a building isn't an option, for most at least.

Commercial office funds which own office buildings are essentially the window for smaller investors, with an increasing number of financial platform providers offering easy and low-cost access into unlisted funds. Tax Office data shows self-managed super funds alone hold more than $64 billion in unlisted assets, excluding residential real estate.

That number is set to grow further during 2017 as more commercial property opportunities reach the market. In fact, it was a lack of opportunity last year that curtailed investment inflows.

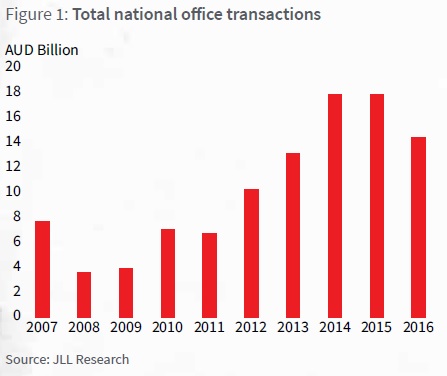

Data from global commercial office managers JLL shows Australian office investment transaction volumes totalled $14.46 billion in 2016, compared with around $18 billion in both 2014 and 2015. Investment inflows this year are likely to edge higher, with commercial property fund managers investing into new office buildings, primarily in Melbourne and Sydney.

Steven Bennett, Head of Direct at commercial property owner and fund manager Charter Hall, says there are a number of key ingredients that investors should be taking into account, including the quality of the assets on offer, the weighted average lease expiry, the management's track record, and returns.

“We know SMSFs and our investor base invests into property because of the income returns you can get. So we're very focused on delivering that security of income for our client base,” Bennett says.

The self-managed super fund segment remains a huge market for unlisted office funds, and that's currently creating a flurry of activity behind the scenes as fund trustees rejig their commercial property positions to comply with the Federal Government's incoming $1.6 million pensions assets cap on July 1.

The new rules mean that those in pension mode must open and transfer back to a superannuation accumulation account (and pay 15 per cent tax on all future earnings in that account) any assets above $1.6 million. For those holding more liquid assets such as shares, the issue is relatively straightforward. But for those in pension mode holding lumpy, illiquid assets such as real property, which are valued above $1.6 million, it's a bigger exercise. They must transfer back the whole property into an accumulation account.

On the other hand, Bennett points out that those with commercial property holdings in an unlisted unit trust can simply do a partial transfer of units from one account to the other, and it's here that much of the action is taking place.

JLL's head of research, Australia, Andrew Ballantyne, says he's seeing strong activity in investor inflows into commercial property, with Melbourne and Sydney definitely leading the charge, but the Brisbane and Canberra markets also showing good signs of recovery.

“Sydney and Melbourne remain firm, but people are surprised at how quickly the Brisbane market has recovered, and Canberra is seeing good rental growth,” Ballantyne says. He adds that the investor flows into commercial office property are a reflection of the risks and returns in other asset classes.

“People are getting next to nothing on cash returns. So they're moving up the risk curve a little bit, but not by too much. The attraction for income investors is that leases are contracts. With a seven year lease you know what cash flow is being generated; there's a higher degree of confidence.”

Ballantyne says that overall there is a growing trend among investors to allocate more of their capital in assets such as commercial real estate.

“It's largely being driven by demographics and the higher dependency ratio from pensioners and those on defined benefit schemes to generate stable income streams in retirement.”

Charter Hall's Bennett agrees. “In this era of low returns getting good quality yield is difficult, and getting it from a core sector is even harder. We focus on institutional grade property. We're not interested in buying second tier assets and gearing them up. We keep all our gearing around 30 – 45 per cent.

“The beauty of going through an unlisted commercial property fund is the gearing is all internalised. If you go through a limited recourse borrowing arrangement the trustee has got to be across all of that. You also leave yourself open to the perfect storm in the case where if the business that's supporting that property gets into difficulty … and you're then forced to sell the asset at the worst possible time.”

This month Charter Hall invested $229 million to buy up a commercial office complex still being finished in Sydney's Parramatta, which on completion next year will be fully tenanted by the NSW Government on a 12-year lease. Bennett expects the income stream to investors will be at the 6.5 per cent mark, plus capital growth.

“You do need to ask yourself, is residential going to deliver the income returns that investors want?,” Bennett says. “Consider the income returns on most residential in core CBD markets in Australia is less than 2.5 per cent once you allow for real running costs, and compare that to commercial where it's above 6 per cent.

“We think if you can get a 6 to 7 per cent return and 3 to 4 per cent capital growth, that's a good result.”