Investor Signposts: March 2, 2018

Economic growth data; and the Reserve Bank meets

- Top-tier economic data features prominently in the coming week with economic growth, building approvals, and retail trade all being released. The Reserve Bank Board also

.png) meets.

meets. - The week kicks off on Monday with the Australian Bureau of Statistics (ABS) releasing the December quarter Business Indicators publication, which includes data on profits, sales, inventories and wages.

- Also on Monday data on building approvals, new vehicle sales, ANZ job advertisements and surveys on the services sector are all released in a hectic start to the week.

- On Tuesday the Reserve Bank Board meets. No change in monetary policy settings is expected. Interest rates are firmly on hold until at least the end of 2018 due to retail deflation and modest wages growth.

- Also on Tuesday, the ABS issues the broader trade data for the December quarter – the balance of payments and foreign debt figures. The current account deficit narrowed slightly to $9.1bn in the September quarter.

- Retail trade data for January is issued on Tuesday. Sales data has been volatile in recent months although the decline in December was largely expected after the biggest increase in sales in eight years in November. The pick-up in quarterly retail sales volumes should be a positive contributor to economic growth for the December quarter. Retail trade may have lifted 0.4 per cent in January.

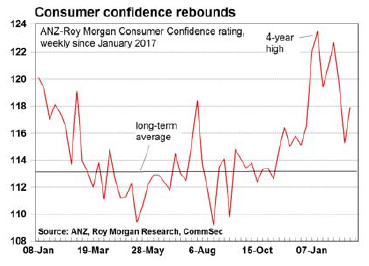

- Also on Tuesday, Roy Morgan and ANZ release the weekly consumer sentiment data and the ABS issues the government finance data. The spending figures (consumption and investment) are a key input into the following day's economic growth estimates.

- On Wednesday, the December quarter National Accounts are released. The main interest is in the economic growth figures (the change in GDP) but the data also includes other estimates such as household consumption. The economy probably grew by 0.6 per cent in the quarter and around 2.5 per cent for 2017.

- On Wednesday, the Reserve Bank Governor, Philip Lowe delivers a speech at the Australian Financial Review Business Summit in Sydney. The AiGroup releases its construction industry survey also on Wednesday.

- On Thursday the ABS releases international trade (exports and imports) for the month of January and a surplus of $600 million is expected.

Overseas: Spotlight on Italian election, US jobs and Chinese inflation data

- The week kicks off on Sunday with the Italian general election. The poll is generally regarded as the most important in Europe this year. The Italian economy is improving, but a hung parliament looks likely. Italian shares have been strong performers this year on diminishing bank concerns.

- On Monday, services sector activity gauges are released for both the US (ISM) and China (Caixin). Chinese business activity expanded at the quickest pace in seven years in January. The ISM expanded to its highest level in over twelve years.

- New order growth is accelerating in the US manufacturing sector, rising in six of the past seven months. Factory orders, however, expected to moderate in January when the data is issued on Tuesday.

- On Wednesday the US Federal Reserve issues its Beige Book on economic conditions across twelve regions.

- Also on Wednesday private sector companies (ADP survey) are tipped to have hired a further 195,000 job seekers in February. And the US trade balance report is released. A deficit of US$54.1 billion is forecast in January, up from the US$53.1 billion deficit in December, a 9-year high. Imports have been strengthening. And consumer credit is tipped to increase to US$20 billion in January, up from US$18.45 billion in December.

- Atlanta Fed President Raphael Bostic speaks on the US economic outlook on Wednesday.

- On Thursday we get the latest read on China's trade balance. China's imports surged by 36.9 per cent and exports by 11.1 per cent year-on-year, respectively in January. The

trade surplus stood at US$20.4 billion.

trade surplus stood at US$20.4 billion. - Inflation data is released in China on Friday. Both consumer and business price indexes slowed in January. Factory prices, which feed into the prices that export customers pay, are continuing to decelerate. Prices rose at an annual growth rate of 4.3 per cent in January on lower commodity price growth – a third consecutive monthly decline – weighing on industrial profits.

- Consumer prices softened to an annual growth rate of 1.5 per cent in January. It is expected that the Consumer Price Index picked-up in February after the Lunar New Year base effects pass through from the previous month. Food and non-food inflation will keenly observed.

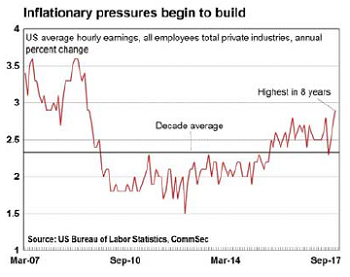

- Also on Friday the all-important US employment report for February is released by the Bureau of Labor Statistics. While the unemployment rate is forecast to remain at 16-year lows of 4.1 per cent, an additional 190,000 jobs are expected to be created. All eyes will be on average weekly earnings with an increase of 0.3 per cent expected. Annual wages growth is the strongest in eight years, sparking inflation concerns in markets.

Craig James is the Chief Economist at CommSec.

Share this article and show your support