Investor Signposts: July 23, 2018

Australian inflation and trade data, and another big week in the US.

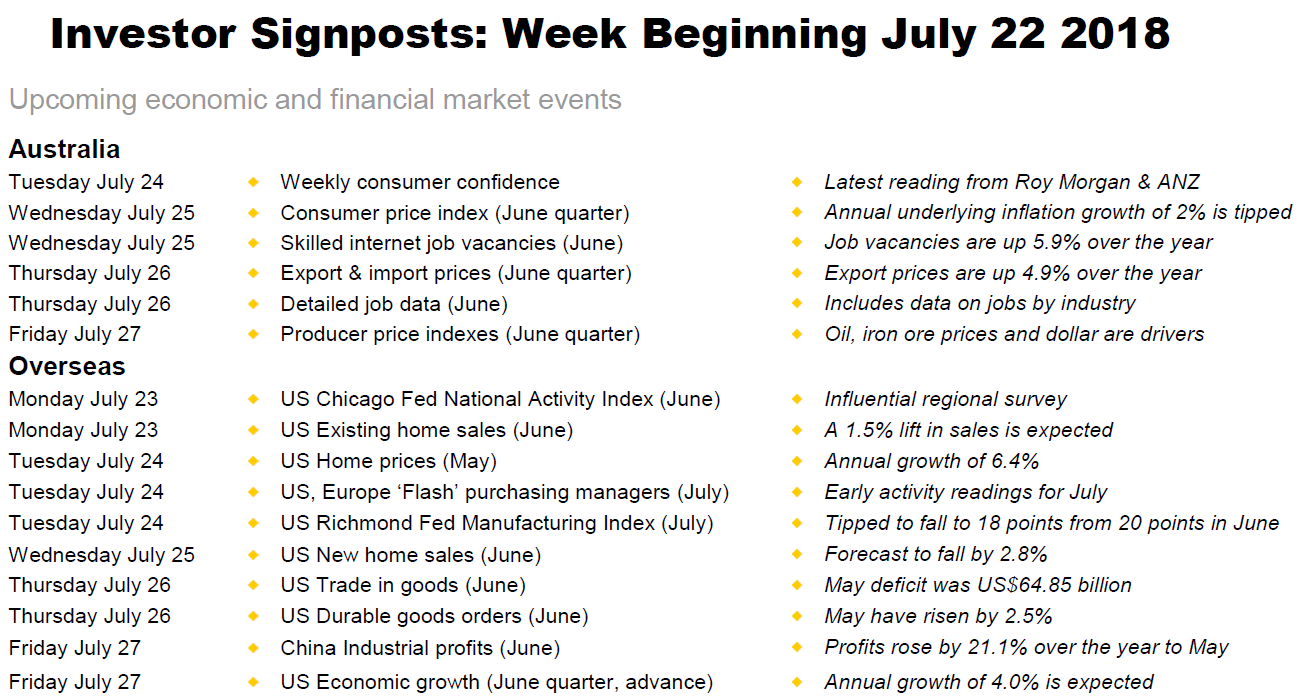

Australia: Will consumer and business prices lift?.png)

- The focus of investors this week will be on consumer and business inflation. Trade (exports/imports) prices are also released. Further information on the jobs market will be keenly observed.

- The week kicks off on Tuesday, with the regular weekly gauge of consumer confidence from Roy Morgan and ANZ.

- On Wednesday, the Bureau of Statistics (ABS) releases the much anticipated June quarter Consumer Price Index – the main measure of inflation in Australia.

- We expect that headline consumer prices rose by 0.7 per cent in the June quarter, to be up by 2.5 per cent over the year. But ‘underlying' measures of inflation are tipped to be more subdued, increasing by 0.5 per cent for the quarter and 2 per cent for the year.

- Significant contributions are expected from rising petrol prices (around 0.2 percentage points) and health (around 0.15 percentage points), while alcohol and tobacco prices are expected to lift too. Falling recreation, communications and fruit prices will keep overall prices in check. With core inflation tipped to remain anchored to the bottom of the Reserve Bank's 2-3 per cent target band in the near term, an extended period of interest rate stability is likely for the remainder of this year.

- Also on Wednesday, the latest skilled internet job vacancy index is issued by the Department of Jobs and Small Business. Vacancies fell by 0.9 per cent in May, but are up 5.8 per cent over the ye

.png) ar.

ar. - On Thursday, trade prices are released for the June quarter. Export (down 1 per cent) and import (down 2 per cent) prices are tipped to decline, but are up 4.9 per cent and 2.1 per cent annually.

- Also on Thursday, the ABS issues detailed job data, including information on employment by industry.

- On Friday, the Producer Price Indices – measures providing a guide on inflation across the business sector – are issued. In the June quarter, the ‘final demand' measure was up 0.5 per cent to stand 1.7 per cent higher over the year. According to the ABS, “the past several quarters have shown significant input price pressures evident across a number of industries”.

Overseas: US economic growth and housing in the spotlight

- It will be relatively quiet in China over the coming week in terms of new economic data. However, there will be data on industrial profits on Friday. In the US, housing market indicators and economic growth are of most interest.

- The week kicks off on Monday in the US, with data on existing home sales to be released alongside the Chicago Federal Reserve National Activity index. After a 0.4 per cent fall in May, economists are tipping a 1.5 per cent lift in home sales in June. A chronic lack of stock on the market is constraining sales but boosting prices.

- On Tuesday, the influential Richmond Federal Reserve survey and the regular weekly data on chain store sales are released, together with home prices. Home prices are tipped to edge up by 0.1 per cent for a second consecutive month in May. The annual growth rate was a healthy 6.4 per cent in May.

.png)

- Also on Tuesday, the Markit organisation releases ‘flash' readings for activity in manufacturing and services sectors in the US, Europe and Japan. In terms of the US readings, an easing in services sector activity is expected to be offset by a small lift in manufacturing activity.

- On Wednesday, weekly data on new mortgage applications is released, together with new home sales. Economists believe that new home sales may have fallen 2.8 per cent in June after surging by 6.7 per cent in May. Sales in the south – which account for the bulk of transactions – jumped to their highest level in over 10 years.

- On Thursday, the influential Kansas Fed Manufacturing Index for July is released alongside a key measure of business investment – orders for ‘durable goods'. Durable goods are generally described as items with lifespans longer than three years – like cars and aircraft. Economists believe orders may have risen by 2.5 per cent in June, following a 0.4 per cent decline in May.

- Also on Thursday, the ‘advance' June data on trade in goods is released. A deficit of US$64.9 billion was posted in May, and the big trade deficits are ‘front of mind' for investors given the Trump Administration's tariff measures.

- On Friday, the ‘advance' reading on US economic growth in the June quarter is released alongside the June quarter Employment Cost index (ECI). Economists expect that the US economy grew at a bumper 4 per cent annual pace in the quarter, after 2 per cent annualised growth in the March quarter. The included data on prices will be watched carefully together with the ECI, which is tipped to increase by 0.7 per cent in the June quarter.

- Also on Friday, China is scheduled to release industrial profits for June. Total profits expanded slightly in May and annual growth was broadly stable. Revenue growth moderated on lower real sales growth in the industrial sector, despite higher producer prices.

Financial markets

- The US company earnings season continues for the June quarter.

- On Monday, Alphabet, Kaiser Aluminium and Whirlpool report.

- On Tuesday, 3M, AT&T, Biogen, Harley-Davidson, Lockheed, and Verizon Communications are among those reporting.

- On Wednesday, Boeing, Coca-Cola, Facebook, Ford, Freeport-McMoRan, Qualcomm and Visa report.

- On Thursday, earnings are due from Allergan, Amazon, American Airlines, ConocoPhillips, Intel and McDonald's.

- On Friday, Chevron, Colgate-Palmolive, Exxon Mobil and Merck and Weyerhaeuser are all scheduled to report.

Ryan Felsman is a Senior Economist at CommSec

Share this article and show your support