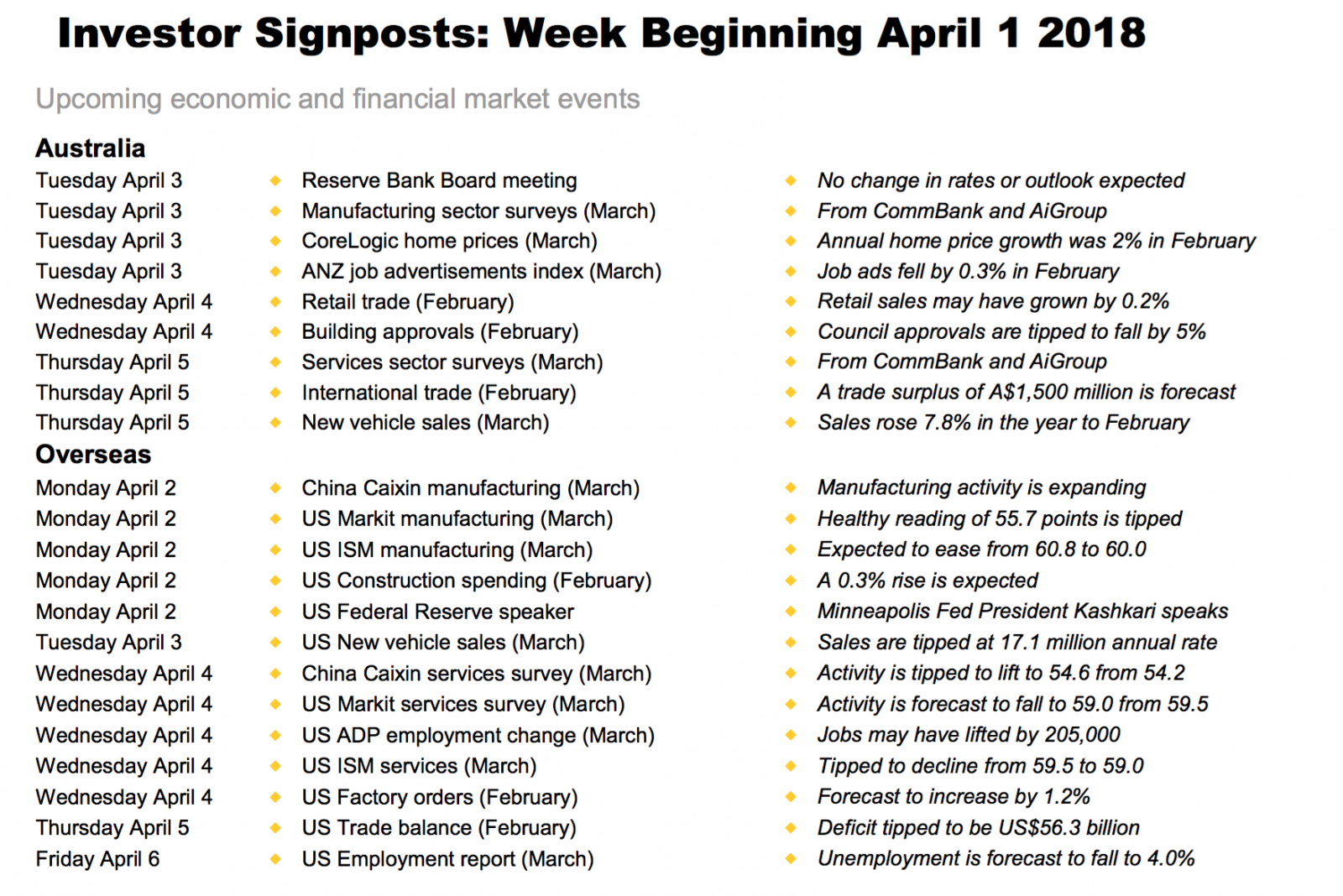

Investor Signposts: April 3, 2018

It's an autumn avalanche of data this short week ahead.

Australia: Autumn avalanche

- It's a short week in Australia due to the Easter Monday public holiday. Top-tier economic data features prominently in the coming week with retail trade, building approvals and international trade all being released. The Reserve Bank Board also meets.

- The week kicks off on Tuesday with data on home prices, ANZ job advertisements, the weekly Roy Morgan-ANZ consumer sentiment survey and surveys on the manufacturing sector all released in a hectic start to the month.

- The Reserve Bank Board meets on Tuesday but no change in the Board's neutral monetary policy settings is expected. Interest rates are firmly on hold until at least year-end due to retail deflation and modest wages growth. Reserve Bank commentary on US trade protectionism and its potential impact on global business investment would be of particular interest to market observers.

- On Wednesday, local council building approvals data for February is issued. Residential building approvals increased by 17.1 per cent in January, led higher by volatile apartment approvals which soared by 43.2 per cent. However, detached house approvals fell by 0.9 per cent. Residential construction is expected to remain firm before declining in late 2018.

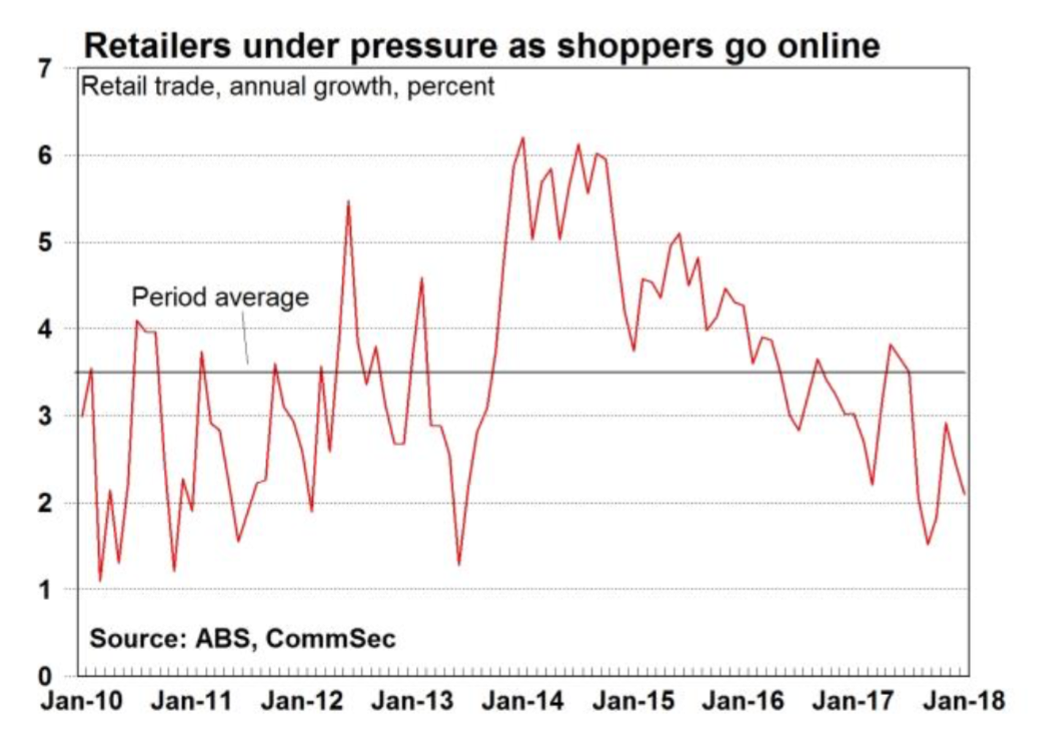

- Also on Wednesday retail trade data is released for the month of February. Retail spending edged higher by 0.1 per cent in January, following December's 0.5 per cent fall and November's 1.3 per cent jump in spending on the back of Apple iPhone X and ‘Black Friday' sales events. While a strong contributor to December quarter economic growth, household consumption remains a key uncertainty this year. Aussie households' spending is restrained by low real wages growth and higher utility costs. However, consumer confidence surveys suggest that improving job security and less desire to save are supportive of retail spending.

- On Thursday Australia's international trade data for February is released. The goods and services trade balance was a healthy $1,055 million surplus in January. Exports rose by 4.3 per cent, while imports fell by 2.4 per cent. The Reserve Bank Commodity Prices Index, which is based on estimates of export prices rather than spot prices, rose by 1.8 per cent in February. An increase in the price of iron ore and coking coal was behind the rise, pointing to a further improvement in the trade balance over February, subject to export volumes and imports.

- Also on Thursday surveys on the services sector for the month of March are issued by both the CBA and AiGroup. New vehicle sales data is also issued. Australia's new vehicle market grew 6.1 per cent in the first two months of 2018 compared with the same period last year. New vehicle prices are near 30-year lows.

Overseas: US employment and trade data in focus

- The data deluge continues in the US in the coming week with most interest in employment and trade.

- The week kicks off on Monday in China with the release of the private sector Caixin purchasing manager's index for manufacturing.

- Also on Monday, the US ISM manufacturing and construction spending data are issued. The ISM prices paid index hit its highest level since May 2011 during February. Manufacturers are passing on higher input costs to their customers, boosting inflation expectations.

- The final US Markit purchasing managers manufacturing index is issued on Monday. Minneapolis Fed President Neel Kashkari speaks on monetary policy and the economy hosted by the University of Minnesota.

- On Tuesday, new auto sales are released in the US. Sales decelerated to an annual growth rate of 11.8 per cent in February.

- On Wednesday, services sector activity gauges are released for the US (ISM & Markit) and China (Caixin). Chinese business activity is expected to have expanded at the quickest pace in seven years in March.

- Also on Wednesday the ADP survey is expected to show that private sector companies hired a further 205,000 job seekers in March. Factory orders are expected to have increased by 1.2 per cent in February after declining by 1.4 per cent in January.

- On Thursday the US trade balance report is released. A deficit of US$56.3 billion is forecast in February, down from the US$56.6 billion deficit in January – a 9-year high. Imports have been strengthening.

- Also on Friday the all-important US employment report for March is released by the Bureau of Labor Statistics. The unemployment rate is forecast to fall to 4.0 per cent with an additional 203,000 jobs expected to be created. All eyes will be on average weekly earnings with a monthly increase of 0.2 per cent expected, translating to annual growth of 2.7 per cent. Consumer credit data is also released on Friday.

Craig James is the Chief Economist at Commsec.

Share this article and show your support