Invest like a tech tycoon

Summary: Silicon Valley technology entrepreneurs are working with private bankers to diversify and manage their wealth, protecting their families' lifestyles from the risks of their red-hot companies. These clients often have more conservative portfolios that offset the risk of their own company stock. Bankers would prefer them to be even more diversified, but there are signs prudence is on the rise. |

Key take-out: Private bankers are using municipal bonds to diversify entrepreneurs' portfolios and staying away from real estate, meaning they can liquidate in a short time. |

Key beneficiaries: General investors. Category: Economics and investment strategy. |

In silicon valley these days, there's an unmistakable sense of déjà vu. The initial-public-offering market is booming, and multibillion-dollar takeovers are back. In the past seven months, Facebook alone spent $21 billion to buy two companies that have no profits. To the casual visitor, it looks a lot like 1999. But talk with the valley's entrepreneurs and investors and something becomes clear: Hidden beneath the hype is a culture that has matured in its own disrupt-or-be-damned way.

Nowhere is that shift more evident than in the personal investment portfolios of the valley's elite. At long last, tech tycoons are diversifying their wealth. And they're being helped by private bankers who've descended on the valley by the planeload, setting up shop alongside venture-capital firms and start-ups. To offset big holdings in their risky companies, tech folk have been working with private bankers to plow money into investments such as farmland and municipal bonds. Long a staple of the East Coast establishment, munis (municipal bonds) are becoming a favourite of Silicon Valley. Not only do they offer welcome ballast, but they also take some of the sting out of California's sky-high tax rates.

Fourteen years after the dot-com crash, Silicon Valley and advocates of wealth preservation have reached a détente: Entrepreneurs realise their red-hot companies can flame out, and the private bankers accept that they're never going to eliminate risk from the personal portfolios of Silicon Valley's tycoons. Says a banker with Northern Trust: “There's still an excess optimism gap – that's what makes them entrepreneurs. But they're willing to be reasoned with.”

That reasoning is the fine line that advisors and their clients now walk in the valley, where, true to form, entrepreneurs are creating their own styles of wealth management. “I do risky things and then non-risky things. There's no middle,” says Steve Mullaney, a long-time tech executive who sold his company to VMWare for $1.3 billion in 2012.

Mullaney has handed some of those assets to Northern Trust, the Chicago bank that now has 50 employees in northern California overseeing $7.4 billion in assets for private clients. Mullaney gives the firm enough money to ensure his family's lifestyle, freeing him up to use the rest to take big risks in start-ups, private equity, and a few stocks. That strategy is common in the valley; private bankers frequently use the phrase “immunising lifestyles” to describe their primary mission.

Northern Trust is “a conservative Midwest bank,” Mullaney says. “They're not people who are going to go crazy with your money … I wanted the opposite of me.”

For Silicon Valley tech titans, such diversification could make the next crash very different from the one that occurred in 2000. Leading up to the dot-com crash, a “financial myopia” had filled the valley, according to Michael Lewis, who famously tracked the life of Netscape founder Jim Clark in his 1999 book, The New New Thing. Lewis wrote of Clark, “He had no interest in preservation of any sort. His life was dedicated to the fine art of tearing down and building anew. He didn't buy U.S. Treasury bonds or stock in companies outside of Silicon Valley or, for that matter, stock in anything outside the outrageously volatile Internet sector.”

These days, valley investors are looking beyond their own backyard. U.S. Trust, among private banking's old guard, is sweetening its wealth management offerings by buying timberland and farmland, particularly for tech clients in northern California. “They built something they can see and touch, and they like to then move [those assets] into something they can see and touch,” says Mark Benson, who runs U.S. Trust's West division. “If we buy a farm and manage a farm for them, they can go out and walk on it.” Such real assets can provide bond-like security, the firm says, with total annual returns of 8% to 10%.

Mark Benson of U.S. Trust says folks who build tangible companies also want tangible assets like timberland and farmland. Photo: Martin Klimek

Traditional stocks remain quite low on the totem pole in Silicon Valley. Entrepreneurs would rather get equity exposure by investing in start-ups run by people they know and trust. “You're betting on people,” says Mullaney, in a theme repeatedly raised in the valley. “Effectively that's like having inside information. [The] information is: I know how good you are.”

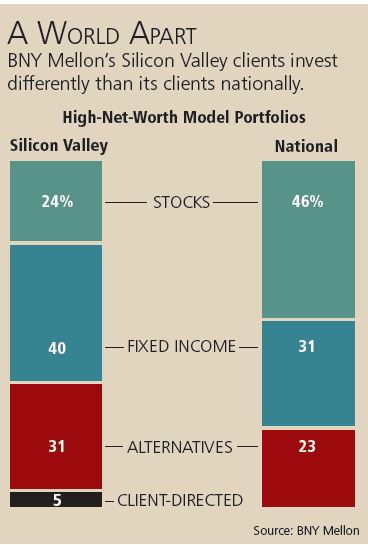

At Bank of New York Mellon – one of the big traditional banks pushing West – the typical valley clients put 31% of their liquid assets in alternative investments, far higher than the bank's national average (see chart). But those same investors are also overweight in fixed income, which accounts for 40% of their assets, versus 31% nationally. Just 24% of BNY's valley portfolios are allocated to stocks, versus 46% for the firm's average high-net-worth portfolio.

“The general theme is their allocation to private equity and alternatives is higher, but when you look at the overall portfolio, it's more conservative,” says David Emmes, who runs the Western division at BNY Mellon Wealth Management. The allocations are moulded to offset the risk that many valley clients carry through their own company stock and options.

Just the sight of BNY Mellon in the Western U.S. is a sign of the times. The bank is a 2007 marriage of Pittsburgh's Mellon Financial and Bank of New York, founded by Alexander Hamilton in 1784. Some 230 years later, BNY Mellon is opening its first Palo Alto office this fall. It recently became a “founding partner” of the San Francisco 49ers new stadium, which opened last month in Santa Clara.

Northern Trust, itself founded in 1889, is wooing entrepreneurs from its office on Sand Hill Road, a six-mile stretch famous for its venture-capital firms. The bank's advisors take a low-key approach, but they've clearly learned how to impress the high-tech set. Says Steve Bell, who heads the bank's wealth-management operations in the West: “We as an industry are much more open than we were 15 or 20 years ago. And with the technology investor, one has to take another degree of openness in that there's an element of the overall portfolio that may well be self-directed by the client.”

Steve Bell, who heads Northern Trust's business on the West Coast, says Silicon Valley entrepreneurs “want to live a certain lifestyle, and they want to immunise that lifestyle.” Photo: Martin Klimek

The idea of establishing a safety cushion is striking a chord. In a conference room filled with flat-screen TVs, Northern Trust displays proprietary software producing risk assumptions and crafting portfolios based on client needs. If a family spends $800,000 a year, the firm knows what kind of investments are needed to fund that lifestyle for decades to come. The model allocates funds into risk assets and risk control, working around clients' big positions. During the demo, the team pulls up graphs to support the firm's risk assumptions, each backed by decades of historical data, the kind of evidence Silicon Valley folks want, says Morris Noble, a Northern Trust senior investment officer. “This is appealing to our kind of clients because they tend to have a linear, analytical thought process. It doesn't require a leap of faith. They can understand the logic.”

Speak to private bankers in California and the term “balance sheet” repeatedly comes up – vast wealth makes clients look more like corporations than families. Often that wealth is tied up in concentrated stock, which stems from a cultural bias in the valley, says Dan Rosensweig, CEO of Santa Clara–based Chegg, an education company that went public last year. A born-and-bred New Yorker, Rosensweig moved to the valley in 2002. He says his West Coast friends prefer equity over salary. “Most of these start-ups fail, and people know that. But it's the journey. It's the experience.”

The concentration adds risk and keeps private bankers working overtime. “As advisors, we would love them to be diversified,” says Harvey Armstrong, who is a managing director at CTC myCFO, a unit of BMO Financial Group. “But it's not our money. We didn't make it, and they are the decision makers in that process.

“We would love them to be diversified, but it's not our money,” says Harvey Armstrong of CTC myCFO. Photo: Martin Klimek

Still, there are signs prudence is on the rise. More and more private-company founders and executives are taking money off the table before an IPO or sale. “That didn't exist in the prior cycle,” says Daniel Schrauth, a San Francisco–based wealth advisor at JPMorgan Private Bank. It's now “incredibly common” for entrepreneurs to sell private stock in their companies and take more time to go public. “That's evidence of their changing viewpoints on the value of diversification.”

To balance the risk, JPMorgan uses muni bonds. The primary goal is to decrease correlation with concentrated positions, while reducing the time needed to raise cash, if needed. To tame a balance sheet that's 60% concentrated equity, JPMorgan recommends 45% muni bonds, 10% equity, 12.5% nondirectional hedge funds, 2.5% hard assets, 10% world government bonds, 15% inflation-protected securities, and 5% cash. Real estate is left out. In an emergency, JPMorgan can liquidate in just three months. As concentration falls, the firm ups equity and hedge funds and adds real estate, while scaling back on munis.

JPMorgan's private bank, which is known for inheriting post-IPO clients from its investment bank, is trying to forge its own identity these days. Two years ago, the firm moved Jeremy Geller to San Francisco from New York, where he had run the private bank's hedge fund efforts. It was recognition from JPMorgan that the valley now needed sophisticated advice as much as New York's financiers. Geller calls his team an “investment banker for private clients,” bringing to individuals the kinds of strategies normally reserved for institutional investors.

JPMorgan's Jeremy Geller calls his team “an investment banker for private clients.” Photo: Martin Klimek

Like so much of silicon valley, the region's wealth management itself is subject to disruption. In the late 1990s, one of Clark's major projects was called myCFO – a response to his distaste for bankers. Clark saw software and the internet as a way to end wealthy clients' reliance on expensive advisors. Accounting and asset management would be provided in-house at a much lower cost.

Valley executives and venture capitalists flocked to the idea; Cisco's John Chambers was hot to be the first client, according to Lewis' account in The New New Thing. But the dot-com crash intervened. By 2002, myCFO's tax shelters were invalidated by the IRS. BMO Financial bought some of the firm's assets later that year.

Right now, the newest new thing is Wealthfront, an automated, low-cost, passive investing service aimed at the 20-somethings getting hot jobs in the valley. Wealthfront spreads their assets across 11 ETFs based on answers to a risk survey. These investors are cynical after the 2008 crash and “hate sales pitches,” says CEO Adam Nash. “The idea that you can beat the market sounds like a sales pitch, and more importantly, it hasn't come true in their lifetime,” he adds. Courting average accounts of $80,000 from those young adults, Wealthfront has amassed $1 billion in assets in under three years.

The valley's private banks don't appear to be threatened, and the tech titans aren't eager for cookie-cutter solutions. What matters to them is having a smart advisor who can ensure that their risk-taking doesn't endanger their lifestyle.

It's 2014 in the valley. Priorities have changed.

This article has been reproduced with permission from Barron's.