Hungry property investors are starving small business

Housing speculation continues to drive credit growth across the country. Lending growth otherwise is quite muted, reflecting both the high existing stock of credit to businesses and households but also the ongoing popularity of refinancing and deleveraging.

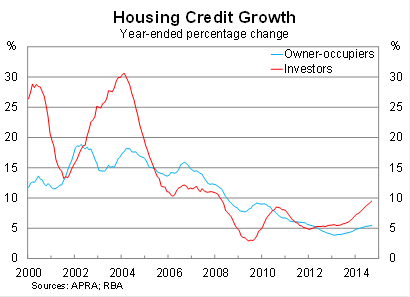

Housing credit rose by 0.6 per cent in September, to be 6.8 per cent higher over the year. Growth continues to be concentrated among investors, with credit outstanding to investors rising by 9.5 per cent over the year.

Growth in investor activity is at its highest level since April 2008. That might give the impression that speculative activity is not particularly abnormal -- a view only reinforced by the next graph -- but we have to remember than this growth in investor activity is coming off an exceedingly high base.

Credit outstanding to investors has increased by 60 per cent since April 2008 and investor activity, as a share of total credit outstanding, has increased from 16.5 per cent to 20.6 per cent in September.

As a general rule, the higher the stock of credit, the greater the potential systemic and financial risks for any given level of credit growth. In the absence of a lengthy period of deleveraging, the Australian economy is unlikely to experience credit growth in the same vein as the 1990s and early to mid-2000s.

Growth in credit to owner-occupiers continues to grow at a more moderate pace, rising by 5.5 per cent over the year and -- given mortgage approvals appear to have peaked -- I'd expect credit growth to owner-occupiers to peak in the next three to six months.

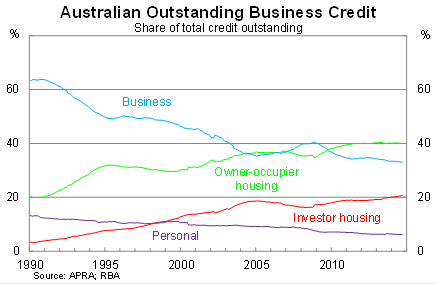

Nevertheless, mortgage lending in aggregate has been sufficient to crowd out lending to the business sector. This hasn't been such an issue for larger organisations -- who can utilise equity or even bond markets for financing if they need to -- but for smaller businesses it can be the difference between success and failure.

Mortgage lending now accounts for almost 61 per cent of total credit. The business sector accounts for just 33 per cent -- down from over 45 per cent back in 2000 -- which reflects a range of factors including the ascendency of the mining sector and a strong preference by domestic banks to hold mortgage rather than business assets.

The dynamics of the lending market -- including both the growth rate and share of total credit for investors -- makes it abundantly clear why the Reserve Bank of Australia has expressed concern about the domestic property market (Another RBA warning on housing, October 10).

Low interest rates will continue to support domestic activity, but the speculation fuelled housing boom appears to be on borrowed time. From a long-term macroeconomic perspective that's a good thing, even if many recent investors don't quite find the return they were looking for.

The challenge for the Australian economy is clear: we need the non-mining sector to begin investing in our productive capacity. Rampant speculation in domestic property -- and by extension land prices -- reduces our international competitiveness and in many ways creates a barrier to entry for new businesses.

It is also a poor model for long-term sustainable growth. How exactly will the property market continue to flourish if the business sector performs poorly? In the long-term, house prices are determined by a combination of leverage and incomes and current lending market dynamics clearly undermine the latter.

Our long-term prosperity will largely depend on productivity growth and, right now, the market simply isn't calibrated to that effect. That should be a concern for almost everyone in Australia -- rich or poor, young or old, businesses or households -- because starving the business sector is a recipe for weaker long-term income growth and that is ultimately a recipe for a lower standard of living.