How ETFs are powering the markets

Tony Kaye

How ETFs are powering markets

I want to start this Weekend Brief by talking about exchange-traded funds. What's going on in the ETFs sector globally is nothing short of phenomenal, and Australian investors are joining the party in droves.

Now, you wouldn't have seen them, but there were celebratory fireworks over Wall Street earlier this week. They had nothing to do with the Independence Day holiday on July 4.

That was a bonus, of course, because I wouldn't be surprised if there were quite a few fund managers, financial advisers and traders nursing sore heads on Tuesday morning. 2017 is turning out to be their best-ever year – at least so far.

While the United States doesn't rule off its end of financial year books on June 30 like we do, the end of last month marked a new milestone for the exchange-traded funds sector as investment records tumbled yet again.

The latest trading data shows that, in the first six months of 2017, just under $US250 billion of global investor funds were ploughed into ETFs. That's more than double the rate of the previous two years, and around $US45 billion of those new investment funds came through in June alone.

Most of the money went into the US – the epicentre of the ETFs market – but there was also a strong flow into European funds. And a portion of those inflows came from Australian investors too, because ETFs are really taking off here as well.

So, given there were 22 market trading days in June, the total inflows work out to more than $US2 billion per day. That equates to lots of fees for the fund managers, and don't forget the huge online brokerage fees that are being generated too.

And it turns out, in the US at least, that around half of all new inflows are going to just four ETF issuers. Blackrock, which offers its products under the iShares banner, is the undisputed ETFs king with a whopping $US1.7 trillion of ETF assets under management globally. Vanguard is now sitting on about $US735 billion in ETF funds, State Street with $US540 billion, and Invesco with $US124 billion.

Some experts are describing the ETFs sector of the market as an unstoppable juggernaut, which is definitely not an overstatement.

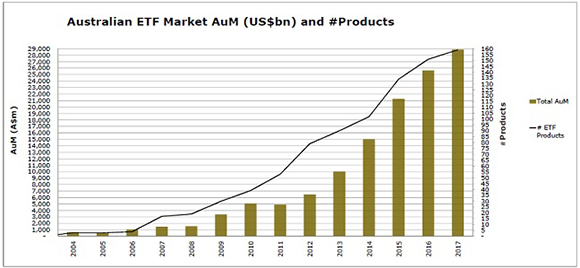

Our own ETFs market is now worth close to $30 billion, and it's clear that number will continue to grow strongly over time. New ETF products are being added to the ASX boards just about every month. If we look over the past five years, the Australian ETFs market has recorded a compound annual growth rate of 35 per cent.

So what are the driving factors in the Australian ETFs market? Well, of course, we're just a microcosm of what's happening on the global market. Investors globally are now using ETFs as an essential component of their stocks portfolio. In a single stock market trade, an investor can effectively buy one security that covers off a whole market index, a specific sector or an asset class.

They're very low cost too, which is certainly very attractive. The iShares Core S&P 500 product, for example, which is available on the ASX, is charging fees of just 0.04 per cent.

Increasingly, ETFs are being used to complement more active stock picking strategies, so investors can effectively have a foot in both camps. They may hold one or more ETFs as a passive index investment strategy, and use unlisted managed funds or listed investment companies as their active strategy to outperform the market.

Also, rather than just being used as a long-term strategy, more investors are using ETFs for short-term plays across commodities, currencies and other thematics.

In Australia, investors are primarily buying ETFs that cover the S&P/ASX 200 or the whole Australian market, the S&P 500, and ETF products that generate a regular income stream. Many are also buying a blend of different ETFs through tax-effective structures such as separately managed accounts that align with their diversified growth and income strategies.

As a disclosure, I should note that InvestSMART now has five ETF-based funds on its product list where investors can do exactly what I've said above. Click here to find out more.

ETF assets under management in the US are now just shy of $US3 trillion. That represents about 6 per cent of the total US stock market's value, which is an amazing statistic in itself. In a report this week investment bank Goldman Sachs said that ETFs were one of the major forces behind the US market's solid gains over this year.

Which is sort of what some market commentators are alluding to when they raise concerns about the pace of inflows into US ETFs. They're saying this is heightening the prospect of a price bubble being formed on the US stock market.

But I wouldn't put too much credence into that. The fact is that investors are also buying shares directly and through managed funds and other products. The demand is already there, so ETFs are just another mechanism. What happens on the US market will relate to other factors, not to the growth of ETFs.

We won't know the full Australian ETF figures for 2016-17 for another week or so, but I spoke to several of the key ETF players in the Australian market during the week and they were very upbeat. No real surprises there. We can expect to see solid funds growth again having been recorded over the last financial year. The actual number of new ETF funds added here will come close to $6 billion.

One thing is certain. Expect that inflows figure here to increase substantially in 2017-18 as more investors board the ETFs bus.

Nerves of steel

At a recent Sunday outing in May, a friend of mine who happens to be an executive at Arrium had just returned from a “business mission” to the UK.

Last year he went on a different mission, to North America, and shortly after Arrium announced the sale of its Moly-Cop grinding media business for $US1.23 billion.

In May my friend didn't give anything away about what he was doing in the UK. But there wasn't much to guess about really, because the joint takeover bid for Arrium from London-based Liberty House and its stablemate SIMEC, through their GFG Alliance bidding vehicle, was already out in the public arena.

It was no secret that the team at Arrium, including representatives for corporate administrators KordaMentha, were busy trying to bed down a final deal – either with GFG or the Korean steelmaker POSCO. Arrium was placed into voluntary administration in April last year, owing its bankers and creditors close to $4 billion.

Finally, after months of negotiations, this week the Liberty-SIMEC consortium was announced as the winning bidder for Arrium's Australian steelmaking and iron ore assets. They include its Whyalla steelworks, an iron ore mine in the Middleback ranges, electric arc furnaces and mini mills in Victoria and NSW, and scrap recycling operations.

It's great news for Whyalla, where Arrium employs the bulk of its 5500-strong workforce. GFG says it will spend $1 billion on the operations.

But what does the deal mean for Arrium's long-suffering shareholders? The short answer is, nothing. As always, the company's banks stand first in line to recover their debts – and the takeover deal won't even pay them back in full. If there was anything left, smaller creditors would get second dibs. Ordinary shareholders are always last in line.

Arrium shares are suspended, having last traded in April at 2.2 cents. Those who bought in above $6 a share at its peak in 2009 will never see their money again.

For the group of company shareholders who formed the group Arrium Shareholders United, and all Arrium investors, I really do sympathise.

But the writing has been on the wall for Arrium for some time. Investing in any business, especially one as complex as Arrium, involves taking on significant risks. Do your homework, so you know exactly what you're getting into.

In some cases, like Arrium, you need nerves of steel to invest.

This Week

Shane Oliver, AMP

Investment markets and key developments over the past week

- Global share markets were messy again over the last week as bond yields backed up further continuing the latest “taper tantrum” that was kicked off by several central banks led by the ECB just over a week ago. Eurozone shares rose slightly but US, Japanese, Chinese and Australian shares fell. Bond yields continued to rise partly in response to the minutes from the last ECB meeting which indicated it considered dropping its easing bias (but decided against it because it might trigger a tightening in financial conditions - which of course has happened anyway!). Commodity prices slipped and this combined with a still neutral RBA contributed to a fall back in the $A, which is continuing to bounce up and down in the same $US0.72-78 range it's been in for more than a year now.

- The back up in bond yields in response to a shift to a somewhat more hawkish tone from several central banks could have further to run, but for shares its likely just another correction. After strong gains and signs of investor complacency shares and bonds have been vulnerable to a correction for some time. The first “taper tantrum” in 2013 which was kicked off by then Fed Chair Ben Bernanke's comments around slowing or tapering the Fed's quantitative easing program saw share markets fall 6-11 per cent and 10-year bond yields in the US and Australia rise by around 140 basis points. However, we remain of the view that the latest taper tantrum will settle down. The only reason central banks have become a bit more hawkish is because global growth has improved which in turn is good for profits and shares, monetary tightening by the ECB and other central banks even when it does get underway will be very gradual (with the recent back up in bond yields and the Euro likely to further slow the ECB) and it will be a long time before global monetary policy is tight and hence threatening to shares. So, expect the correction in shares to remain just that and the uptrend in bond yields to remain gradual (despite occasional spurts higher).

- Of course, in Australia the RBA has not even joined the hawkish tilt of other global central banks. In fact, after its July meeting the RBA retained a neutral bias in terms of the outlook for monetary policy. Not following other central banks with a hawkish tilt was a good move because not only would it have been premature and unnecessarily scare the horse as one Board member put it, but the failure to do so helped knock the $A a bit lower. Our view remains that the RBA will be on hold for the next year at least, with risks around the consumer and a housing slowdown preventing hikes but a fading in the drag from the mining investment slump and solid employment growth heading off cuts. A recent good run of data in Australia – for jobs, retail sales and trade – has seen the risk of another rate cut in the short term recede.

- North Korea is back in the headlines as a threat to the world and as a source of investment risk following the testing of an Intercontinental Ballistic Missile which looks to have been designed to achieve maximum annoyance ahead of the July 4 Independence Day holiday in the US. North Korea's progress towards being able to reach the US with nuclear weapons is clearly continuing. This led to the usual condemnation from western countries and talk of sanctions. But it's a tough one: a military strike against North Korea is obviously being considered again but the likely catastrophic consequences for Seoul/South Korea and potentially Japan mean that some form of diplomatic solution to contain the threat is more sensible and hopefully more likely. North Korea could be a source of further volatility in share markets, but trying to protect investment portfolios against the threat it poses (beyond buying defence stocks and safe havens like government bonds, cash and gold) is a bit like trying to hedge against the risk of nuclear war in the post war era.

- New Zealand is showing Australia up. Not only do they have a sensible energy policy and climate change strategy, a sensible tax system, budget surpluses, falling public debt and faster broadband all achieved with a fraction of the angst Australia seems to go through … but they have just won the America's Cup! Which is something we were did once when we were about to embark on a roughly 20-year run of economic reforms. Sporting achievements aside, our populist Senate and bouts of ideological and/or personality driven politics in our major political parties is working against our national interest.

Major global economic events and implications

- US data was mostly solid. The ISM manufacturing and services conditions indexes rose to strong readings above 57 and while the Markit PMIs are a bit softer, overall it suggests that US businesses are doing well. Labour market data was solid. And core capital goods orders were also revised up to show a small rise in May. Against this construction data for May was soft. The minutes from the last Fed meeting added little that was new with debate over when to start letting the Fed's balance sheet run down (ie reversing quantitative easing) and the case for letting the labour market run a little hot against the risks regarding financial stability of leaving interest rates too low for too long. Overall, we are inclined to see the Fed announce the start of the balance sheet run-off in September and then wait to December (given recent soft inflation data) before raising rates again.

- Eurozone manufacturing and services conditions PMIs for June were revised up to solid levels consistent with solid growth. While strong growth indicators point to the ECB reducing its quantitative easing program for next year (from €60 billion a month to €30 billion a month) the back up in bond yields and the Euro, low inflation and risks around Italy suggest that this is unlikely to be announced until late this year and that the first rate hike won't occur until late next year.

- Japan's Tankan business conditions survey improved a bit more than expected and points to ongoing reasonable economic growth.

- Chinese business conditions PMIs mostly rose in June consistent with a stabilisation or modest improvement in growth after a modest slowing.

Australian economic events and implications

- Australian data was mostly on the strong side. The Australian Industry Group's business conditions PMIs were solid in June, retail sales rose nicely for the second month in a row in May pointing to solid consumer spending in the June quarter, the ANZ job ads survey remained strong pointing to solid jobs growth and the trade surplus rebounded in May as coal exports recovered after the impact of Cyclone Debbie and gas exports rose strongly as LNG projects complete. However, it would be wrong to break out the champagne just yet as building approvals fell sharply in May confirming that home building activity is set to slow and low wages, high underemployment and the July surge in power prices will weigh on consumer spending going forward. In other data, home prices bounced back in June after seasonal weakness in May but momentum in Sydney and Melbourne is continuing to slow and the Melbourne Institute's Inflation Gauge showed continuing benign inflation.

Dr Shane Oliver is head of investment strategy and chief economist, AMP Capital

Next Week

Craig James, CommSec

Household and Business confidence in focus

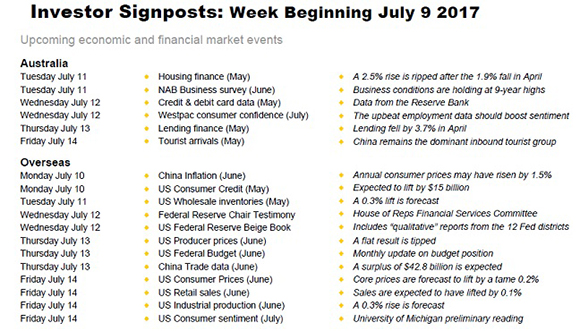

- Another big week of economic events is in prospect in Australia and overseas. In Australia the focus will be on business and household confidence as well as the lending landscape. In China, trade, and inflation indicators are released throughout the week. In the US, Federal Reserve chair, Janet Yellen, gives testimony on the economy while data on retail sales and consumer prices are the highlights.

- In Australia the week kicks off on Tuesday with the Australian Bureau of Statistics (ABS) release on housing finance. Despite the tighter lending standards adopted by the banking sector, and based on data from the Bankers Association, it is likely that loans for owner-occupiers (those who want to live in the homes) rose by around 2.5 per cent in May after falling by 1.9 per cent in April. And the total value of all new loans may have risen by 1.9 per cent in the month.

- Also on Tuesday the National Australia Bank business survey is released alongside the ANZ and Roy Morgan weekly consumer sentiment survey. The business survey covers key business indicators, a reading on business confidence as well as gauges on prices, wages and finance. The indicators of confidence and conditions have showed encouraging improvement since the Budget, with a particular focus on a lift in profitability.

- On Wednesday the monthly Westpac consumer confidence index is released. The weekly survey has shown that households are in a happy place, with confidence levels holding at a 12-week highs. And it is likely that both readings will get a further boost following the improvement in job security and lower petrol prices.

- On Thursday, the ABS will release lending finance figures – includes housing, personal, business and lease loans. Total lending statistics fell from 4-month highs in April, down by 3.7 per cent to $70.2 billion.

- Also on Thursday, the Reserve Bank releases data on credit and debit card lending. Consumers continue to cut back on credit card debt. In smoothed terms (12-month average) the average balance was down by 0.8 per cent on a year ago. Interestingly credit card accounts lifted by 1.2 per cent in the past year, whilst debit accounts grew by almost 8 per cent – highlighting the shift away from debt.

- On Friday. The ABS releases the Overseas Arrivals and Departures publication that has information on both tourism and migration flows. Chinese tourists are still flocking down under. Tourists from Greater China (China and Hong Kong) comfortably exceed those from New Zealand, but tourists from mainland China should pass NZ in their own right in the next few months.

Spotlight on US and Chinese data; Fed Chair Testimony

- So-called ‘top shelf' economic indicators are released in China in the coming week. And in the US Federal Reserve Chair, Janet Yellen, testimony will draw the most interest alongside retail sales and consumer price data released on Friday.

- China will actually kick off proceedings over the week – with the release of inflation data on Monday. Similar to what has been seen across the globe, inflation in China has lifted over the past year, but remains well contained. In fact producer prices (business inflation) - which was in a deflationary environment 12 months ago - is now up 5.5 per cent over the year.

- In the US, on Monday the Labour Market Conditions index is released alongside consumer credit data. It is widely expected that consumer credit lifted by around $15 billion in May.

- On Tuesday, the National Federation of Independent Business releases its Business Optimism index alongside the JOLTS survey of job openings and data on wholesale inventories and sales. For the record inventories are expected to have lifted by 0.3 per cent.

- On Wednesday the Federal Reserve chair, Janet Yellen, delivers the "Semi-annual Monetary Policy Report" to the House Financial Services Committee. The hope is that the report and testimony from the Federal Reserve chair will clear up a lot of issues related to how the Fed believes the economy is faring, timing of balance sheet adjustments and where rates are headed over the medium term.

- Also on Wednesday the US Federal Reserve releases the Beige Book - the indicator is a ‘qualitative' survey of economic conditions across 12 Fed districts - released ahead of Federal Reserve interest rate decisions. In addition the usual weekly data on home purchase and refinancing is issued.

- On Thursday, the weekly figures on claims for unemployment insurance are released together with the June data on producer prices and the monthly budget statement. The producer price index (business inflation) is expected to remain tame. Analysts expect a 0.1 per cent rise in the “core” rate (excludes food and energy).

- In China on Thursday, trade data (exports and imports) is slated for release. A trade surplus of $42.1 billion is forecast.

- And we have to wait till Friday for the key ‘top shelf' indicators for the week – namely retail sales and consumer prices. Economists tip a 0.1 per cent increase in June retail sales after the 0.3 per cent slide in May. No doubt fluctuating petrol prices are having a significant influence on the results. Encouragingly core sales (sales less autos and gasoline) are expected to have lifted by 0.3 per cent in June.

- The consumer price index is tipped to lift by just 0.1 per cent in June. Excluding food and energy prices are expected to rise by only 0.2 per cent. Clearly inflation remains well contained and allows the Federal Reserve to time to gauge how the economy is faring before raising interest rates.

- Also on Friday, data on business inventories is issued, alongside industrial production, and the University of Michigan confidence reading.

Craig James is chief economist at CommSec.

Readings & Viewings

Go figure. France announces is will ban the sale of all petrol and diesel cars from 2040, just over 22 years from now, and Tesla's share price heads into bear territory. It's no longer the biggest US carmaker by market capitalisation. Doesn't make a lot of sense really.

The times, they are a changing. Just ask the iconic Swedish carmaker, Volvo, as it goes all electric. It will be giving Tesla a run for its money.

Warren Buffett isn't sitting on his hands when it comes to energy investment. He's close to spending $US18 billion to buy one of the largest power transmission companies in the US.

Sun? Dirt? Nope, looks like LED light could be the future of farming.

Another fashion house has bitten the dust, although there's always hope of a resurrection. Jeans group True Religion filed for bankruptcy this week, joining a growing list of clothing firms this year that have filed for protection.

Could this be a North Korean attack? South Korean-based Bithumb this week reported thousands of its Bitcoin customer accounts had been hacked.

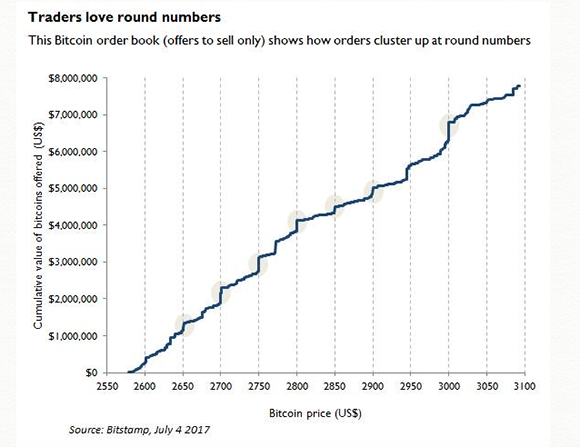

And as always, there's been a number of new Bitcoin predictions this week, like "$5000 soon" and "$50,000 within a decade". Not only do people buy into hype, but they like these round numbers. Check out the pattern forming in the Bitcoin order book:

Timeshares are not something we hear much about these days, but one scheme (or scam) was in the news this week.

Speaking of strange figurations, did you hear what happened to Alphabet, Amazon and Apple on the NASDAQ earlier this week? Thanks to a technical glitch, they absolutely tanked. It seems $123.47 is the magic number.

Also during the week came news about the dark web. It's a dark place, for dark deals, and some users are worried they've been scammed. Maybe stay off it then?

Meanwhile, it was a £15 million deal allegedly struck after a boozy night at the Horse and Groom pub in London. That's the basis of a High Court claim against the founder of listed British group Sports Direct.

Speaking of scams, remember this Chinese project involving buses that would be able to straddle traffic? It turns out that investors have been given a bum steer.

Here's a harrowing weekend read on arson, which speculates that San Fransisco is burning because of soaring property prices.

This theory about power causing brain damage could explain a lot.

Lastly, what a great name. Take a peek inside the Titanic Hotel. And, earlier this week came a story that relics from the Titanic are set to be auctioned off.