Gender balance buys better results

Summary: Several international studies have found a link between gender-diverse executive teams and financial outperformance. Our analysis of the share price performance of listed Australian companies also found companies with diverse management teams outperformed. Commentators say companies with homogenous management teams may be missing out on talent, and companies with broader ways of thinking about business opportunities may be the ones that are most likely to choose female executives. |

Key take-out: Using the most recent available figures, our analysis showed Australian companies with at least one female executive performed better than the index, while companies with 30 per cent or more female executives had an even better result. |

Key beneficiaries: General investors. Category: Shares. |

A growing body of research shows that companies with more diverse senior management teams in terms of gender outperform their rivals financially. Although international studies abound, comparatively little Australian research has been done on the subject. In search of insights for Australian investors, Eureka Report has undertaken an analysis of the share price performance of listed Australian companies to compare those with both male and female executives and those with only male executives.

Using data from 2012, the most recent year for which comprehensive figures were available, 167 companies were identified from the ASX500 as having at least one woman among their executive key management personnel (KMP). The data uses the Australian accounting standard definition of KMP as “persons having authority and responsibility for planning, directing and controlling the activities of the entity, directly or indirectly, including any director (whether executive or otherwise) of that entity”, while executive KMP are the executive members of the group of KMP.

Over the two years to April 30, 2012, the report's census date, the All Ordinaries, which tracks around 500 Australian equities, fell by 7.59 per cent (or –3.86 per cent annualised).

An index of the 167 companies with at least one female executive KMP, equally weighted, fell by 4.71 per cent (or –2.38 per cent annualised). That is, it lost less ground than the All Ordinaries:

Source: Bloomberg, WGEA, Eureka Report

Some 41 companies were identified where woman made up 30 per cent or more of the total executive KMP. An index of these companies, equally weighted, rose by 5.73 per cent (or 2.82 per cent annualised):

Source: Bloomberg, WGEA, Eureka Report

For this sample and time frame, the share prices of companies with gender-diverse senior executive teams outperformed.

Looking offshore

These results are comparable to the findings of international studies with larger sample sizes. A 2014 Credit Suisse study of over 3000 companies found companies where women made up more than 15 per cent of senior management posted a return on equity of 14.7 per cent in 2013, while companies where women comprised fewer than 10 per cent of senior management had a ROE of 9.7 per cent.

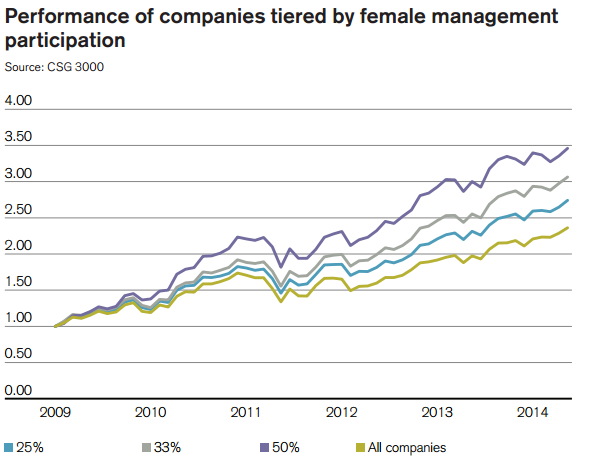

Credit Suisse examined the share price performance of companies grouped by the proportion of women in management. The study compared companies with at least 50 per cent female management representation, 33 per cent and 25 per cent to the entire universe of companies. “Essentially, as each threshold was raised, performance increased,” the authors wrote:

Source: Credit Suisse

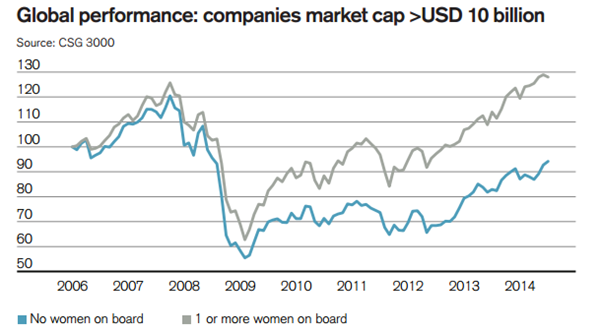

The study also considered the relationship between share price performance and gender of directors. From 2005 to 2014, companies with market caps greater than $US10 billion with at least one woman on their boards posted an excess return of 3.3 per cent a year compared to large-cap companies with all-male boards:

Source: Credit Suisse

Other studies support the Credit Suisse findings.

US research house Catalyst published a 2004 study that covered 353 Fortune 500 companies The top quartile, or companies with the highest gender diversity in their top management teams, reported a return on equity of 17.7 per cent from 1996 to 2000. By contrast, the bottom quartile, or most male-dominated companies, reported ROE of 13.1 per cent. Total return to shareholders over the period was 127.7 per cent for the most diverse companies, compared to 95.3 per cent for the least diverse.

A 2012 McKinsey study considered both gender and cultural diversity across 180 publicly traded companies in the US, UK, France and Germany from 2008 to 2010. Overall, companies that ranked in the top quartile for diversity of senior leadership reported a return on equity of 12.1 per cent, compared with a 7.9 per cent ROE for companies in the bottom quartile. Margins on earnings before interest and taxes were 9.8 per cent for the most diverse companies, compared with 8.6 per cent for the least diverse companies.

This research follows a 2010 McKinsey study that compared the performance of 279 companies in Europe and the BRIC countries from 2007 to 2009. Companies that made the top quartile in terms of female representation in the executive committee compared to their sector reported an average return on equity of 22 per cent, compared to 15 per cent for companies with no women in their executive committee. The study also looked at average EBIT margins. Companies with the highest representation of women in the executive committee had an average EBIT margin of 17 per cent, compared to 11 per cent for those with no women in the executive committee.

US-based academic Roy Adler in 2001 looked at 200 Fortune 500 companies that supplied data for each year since 1980. The 25 firms with the best record of promoting women to executive level reported profits that were 34 per cent higher than their industry medians when compared to revenue, 18 per cent higher when compared to assets and 69 per cent higher compared to equity. The results were reported in the Harvard Business Review and confirmed in later studies every year from 2004 through 2008.

US-based human resources consultants DDI produced a 2014 report that looked at leaders throughout an organisation, from supervisor or department manager level up to the C-suite, for 2031 companies in 48 countries. The study found that for companies ranked in the top 20 per cent for financial performance, 37 per cent of their leaders were women. For companies ranked in the bottom 20 per cent for financial performance, only 19 per cent of their leaders were women.

Causation or correlation?

Most studies and commentators tread carefully when considering the possible reasons for this outperformance. Many point out that two factors may be at work: women may be improving companies' performance, or better performing companies may be promoting women – or a mixture of both.

UK-based Aberdeen Asset Management global chief investment officer Anne Richards says a considerable body of research has shown that diverse teams make better decisions. “Mixed teams are less susceptible to groupthink and are more likely to explore a range of options before reaching a conclusion,” she says. “A process of thinking more laterally and being more open to a wider range of considerations leads to better outcomes.”

“Companies which rely overly on the skills of just one sex are putting themselves at a competitive disadvantage. They are missing out on 50 per cent of the available talent pool,” Richards says. “It is something that is justifiably of increasing concern to serious investors.”

Many commentators, including Escala Partners CIO Giselle Roux, are also quick to point out that gender is only one measurement of diversity, and factors including age, ethnicity and disability are also key to consider. Roux says the choice of a female executive is a suggestion that a company has a broader way of thinking. “Some people say women bring different styles. That might be mildly the case. I think it's more about corporations which behave beyond their inherent biases or norms,” she says. “If you're prepared to include people outside your comfort zone who do not behave in the same way, then you're able to look at a business opportunity through a different lens and come up with different sets of solutions.”

Blackrock head of corporate governance and responsible investment for Asia-Pacific, Pru Bennett, looks for independent directors and a diverse skill base on boards. “There's a lot of research that shows when there is a diverse skill set there's more robust discussion,” she says. “You could have diverse thinking among a group of all men, but what we're saying is there's a risk when people have a similar background, age and experience you may miss out on diversity of thoughts and ideas.”

If companies are doing a good job at succession planning and talent management, then having women on boards and in senior management should be the outcome, Bennett says. “If diversity isn't there, you have to raise the question of what's happened to the talent from graduate level.”

AMP Capital manager of corporate governance Karin Halliday says this talent leakage should be a cause of concern for investors. She has been examining the effects of diversity among the stocks in which her group invests. “I looked at our voting on remuneration packages. We voted in favour of remuneration reports more often when there were two or more women on a board than when there were none.” She attributes this to female directors asking different questions and challenging conventional wisdom. In her sample, she also found when a company has more women on its board it tends to have less related party transactions more independent directors.

She compares the value of a company to an iceberg – the hard assets are visible “above the surface”, but a lot of value is “below the surface” in the form of intangible assets, including the quality of management, which her organisation makes sure to examine.

“We want to make sure we're invested in companies likely to generate the best return.”