Four steps to rebalance your portfolio

Summary: A step-by-step process to rebalancing your portfolio before June 30.

Key take-out: The process begins with updating your risk profile, and ends with clipping or cutting underperforming investments.

June 30 is not a mandatory trigger point when it comes to reviewing and rebalancing your portfolio.

However, the mid-year point is a logical time to do this, especially if you have underperforming or loss-making assets that may be worth offloading to offset capital gains. Likewise, it's highly likely that during the financial year your portfolio allocations have moved out of balance.

A good starting point to reviewing your portfolio is InvestSMART’s free Portfolio Manager. As an investor, you can enter your asset details and specific investment goals, with the Portfolio Manager calculating an asset allocation ratio that's specific for you.

1. What’s your risk profile?

Most retail investors go about portfolio construction bottom-up style. Vanguard Asset Management calls this an "ad hoc approach” where investors simply select a manager or fund and pay little regard to the make-up of their portfolio.

Top-down investors are smoother operators, understanding their appetite for risk, and exactly how they want to dice up their asset allocations.

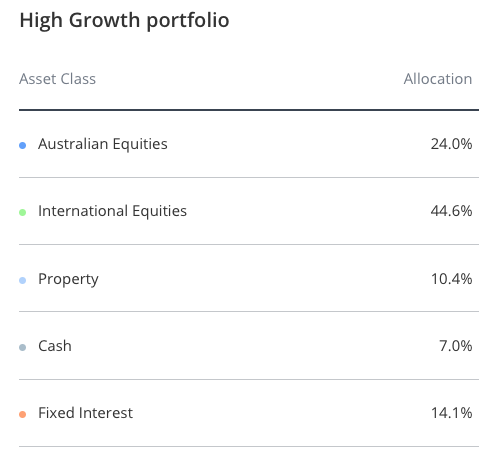

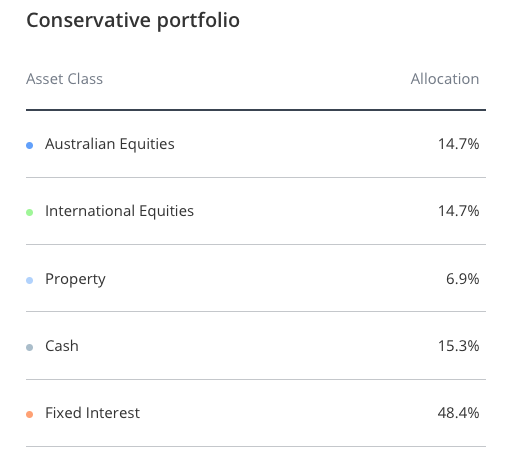

InvestSMART has established four risk profiles, ranging from conservative to high growth. To put this in context, a conservative investor equates risk with danger, while a high growth investor will accept a very high level of volatility.

Source: InvestSMART Portfolio Manager.

Investors often act in ways that place them at extreme ends of the risk curve, sometimes to their detriment. The conservative inclined might be overweight cash, while growth investors can be geared far too aggressively.

Data recently gleaned from 60,000 Australian investors using InvestSMART’s Portfolio Manager can deliver some sounds insights into asset allocation. The data found of the 10,000 investors who claimed they approached risk conservatively, with a zero to five-year investment horizon, because of their high weightings to shares they were actually more aligned to longer-term growth or high-growth profiles.

Even if you consider yourself conservative by nature, it's your horizon that matters. If you’re investing for more than 10-20 years, historically, equities have far outperformed fixed interest and cash over the long-term.

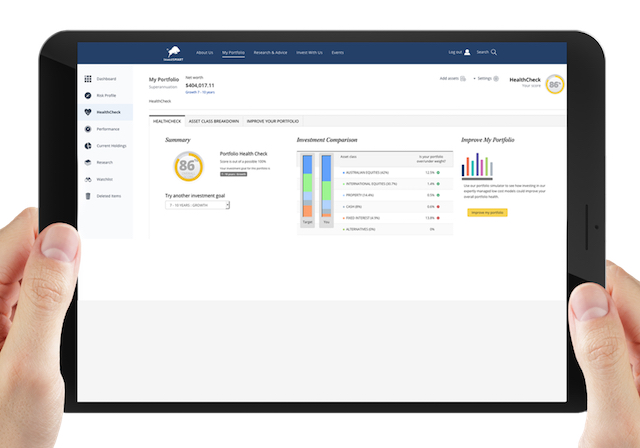

2. Conduct a full HealthCheck™

Consider this your portfolio’s regular health check. Hopefully it’s relatively pain free.

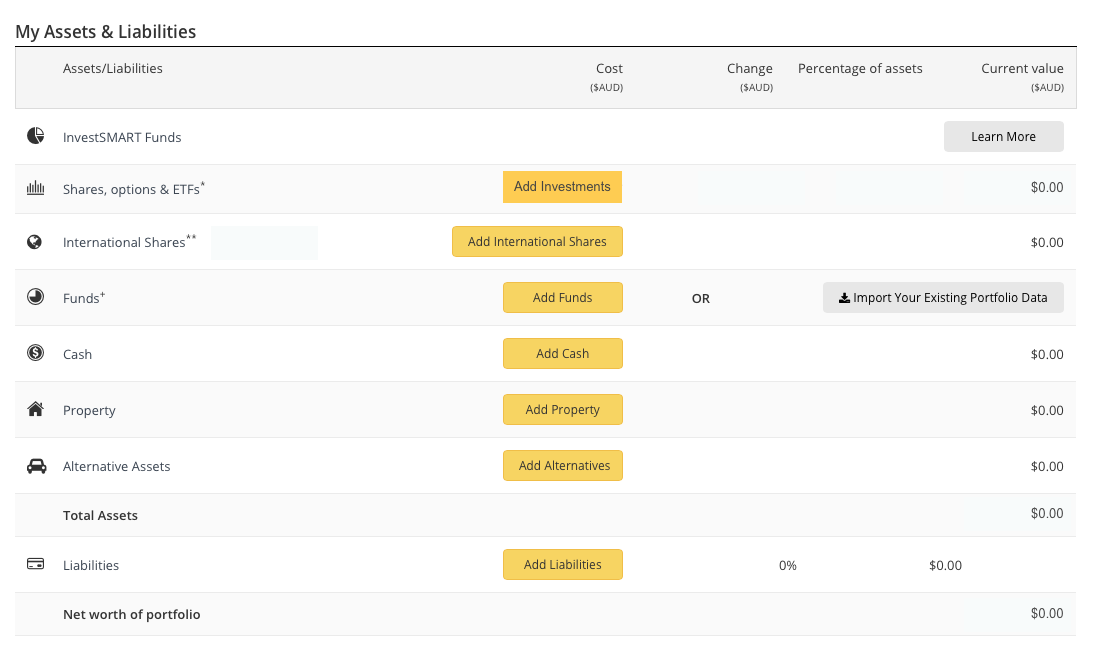

Strip the strategy back to basics. Plug in your risk profile, record your 'Current Holdings' as 'Assets & Liabilities' under the correponding tab on the left of the Portfolio Manager and get an overall HealthCheck™ score.

Going beyond spreadsheet analysis, the Portfolio Manager produces a streamlined and current snapshot. The tool pulls in the dividends of your holdings as they have been announced to the market, the compositions of any managed funds, and property data.

Investors can also change ‘asset class mapping’ through the Portfolio Manager, so if an ASX-listed managed fund, for example, derives most of its earnings from offshore, it can be reallocated as an international holding. This could significantly affect a HealthCheck™ score.

Under the Portfolio Manager, investors can also click the Settings function to add separate portfolios. For instance, a younger investor may have a self-managed superannuation fund with a high-growth profile, and simultaneously run a separate, balanced portfolio as they save for a house deposit.

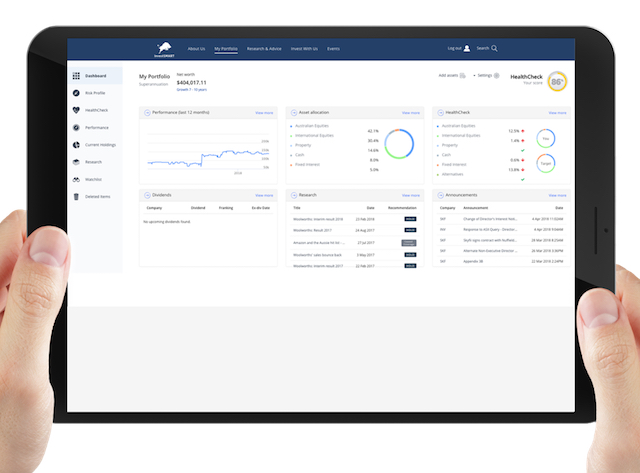

For each portfolio, your HealthCheck™ score indicates how much you are overexposed, or underexposed, to asset classes compared to target allocations for your chosen risk appetite.

If your score seems a little low, and often it will, simulate adjusting the portfolio by adding and reducing holdings via 'Improve my Portfolio' shown on the image below. A score less than 75-80 per cent indicates the portfolio lacks diversification.

The reason it’s out of whack? The ASX 20 represents around 60 per cent of the ASX 200. The financial sector makes up around 50 per cent of the ASX 20. This, along with property, makes up a typical Australian investor’s portfolio. This is not balanced.

However, the goal isn’t to maintain a HealthCheck™ score of 100 per cent, as this would require constant rebalancing, which chews up brokerage fees.

3. Check your balance

Before making any real changes, you can simulate the impact in InvestSMART’s Portfolio Manager.

A portfolio can easily ‘lose its balance’, especially in extended bull and bear markets. In equity bull runs, a portfolio may bend out of shape as individual stocks quickly and disproportionately increase in price more than their peers. It might be time to trim these holdings in favour of undervalued assets.

Rebalancing a standard portfolio too frequently will probably do little for returns. InvestSMART, and others, have crunched the data to prove it.

On a balanced portfolio, if it fell below 80 per cent over the last 20 years, InvestSMART CEO Ron Hodge claims it would only have been rebalanced on four occasions.

4. Taxing matters

It might be time to clip or cut underperforming investments. Tax selling is prevalent from May through to the third week of June.

Similar to simulating the impact of adding or removing an investment to improve your HealthCheck™ score, you can simulate removing an actual investment to review portfolio performance over a certain time frame.

Looking at the granular data, according to brokerage firm Bell Potter, if the average investor drew down their holdings of nine heavily sold stocks last year, they would have been out of the money shortly after.

InvestSMART provides coverage for a couple of these nine stocks that went unloved last June — JB Hi-Fi and Blackmores. As a group, these stocks were down 22 per cent in the financial year to May, and rallied 23 per cent off their lows to their July highs.

These are not recommendations. It’s just an idea worth considering before prematurely dumping holdings and triggering a tax event. As an aid, there may be research on your specific investments under the ‘Research’ tab in the Portfolio Manager.

“Some stocks have really big falls that begin in late May and usually goes until the 2nd or 3rd week of June,” Bell Potter’s Richard Coppleson provides as an explainer to tax loss selling.

“Many of these stocks bottom around then and then start what can be in some cases really big recoveries that go from mid/late June usually until the 3rd week of July and then fizzle out.”

InvestSMART advocates that asset allocation is a key driver of investment returns, playing a much larger role than individual asset selection. However, while putting all your eggs in one basket may not be wise, it’s not wise to cart around a mixed basket of stocks that’s riddled with rotten items.