Fed effect will hit dollar, rates

Summary: Higher interest rates in the US change much of the dynamic around the world, including Australia. But there is still a lot of uncertainty within the Fed about just how strong the US economy is. |

Key take-out: The Aussie dollar finds itself in a precarious position, while don't be surprised to see banks hike rates. |

Key beneficiaries: General investors. Category: Economy, shares. |

A great deal of optimism has been swirling around the United States stockmarket since late last year. Stocks have flourished and the case for tighter monetary policy has strengthened.

The Federal Reserve obliged markets this week by raising its benchmark interest rate to a range of between 0.75 and 1 per cent. It was the second rate hike in the past three months and is expected to be the first of at least three hikes this year.

Nevertheless, the Federal Reserve doesn't necessarily share the same level of optimism as market participants across the United States. In fact it was the dovish tone from Fed chairwoman Janet Yellen, combined with a broadly unchanged economic outlook, which caused government bond yields to tumble following the official announcement.

Market participants were betting on a more hawkish Fed and when that didn't eventuate repricing occurred among treasury bonds. Both gold and commodity currencies rebounded, with the Australian dollar once again jumping to over US76c, reinforcing the fact that market participants were positioned for a more bullish Fed statement.

Instead the Fed reiterated what has long been its mantra: a slow and gradual return towards policy normalisation.

“The data has not notably strengthened,” Yellen told reporters. “We haven't changed the outlook. We think we're moving on the same course that we've been on.”

The earlier temper tantrums that plagued rate hikes appear to be a problem of the past. Nevertheless, the Fed's benchmark rate remains incredibly low by historical standards. The big test for markets will occur when real interest rates (that is the benchmark rate minus core inflation) return to positive territory.

Right now the real federal funds rate sits at around minus 1 per cent, so we still have a way to go.

The March meeting also coincided with the release of the Fed's quarterly outlook. This survey is based on the projections of Federal Reserve board members and presidents and is keenly watched by market participants.

The Fed estimates that long-term sustainable growth in the United States is around 1.8 per cent; so the economy, currently growing at an annual rate of 1.9 per cent, may warrant tighter monetary policy. According to the estimates, the unemployment rate, currently at 4.7 per cent, is already consistent with long-term estimates, which suggests that any further improvement will drive wage growth and inflation higher.

However, the market is most interested in the Federal Reserve's estimates of monetary policy. This provides insight into whether the bank is hawkish or dovish and provides a sense of direction for policy.

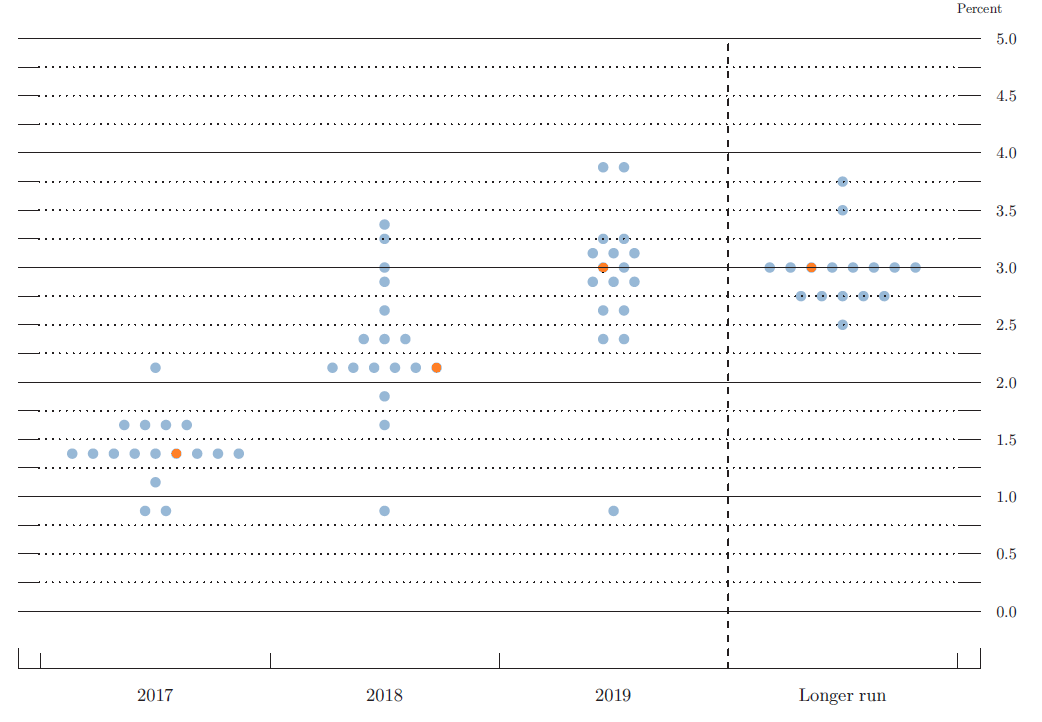

The graph below shows the assessment of where participants believe the federal funds rate should be by the end of 2017, 2018 and 2019. There is a fair bit of disagreement among participants in the survey; Federal Reserve officials often and quite openly disagree with one another and that is reflected in their assessment of monetary policy.

The orange circle represents the mid-point for each year. The mid-point for 2017 is a federal funds rate of between 1.25 and 1.5 per cent – which means another two rate hikes this year – and is expected to climb to 3 per cent by the end of 2019.

Chart 1: FOMC participants' assessment of appropriate monetary policy; federal funds rate

There is still plenty that must occur before those forecasts can be met.

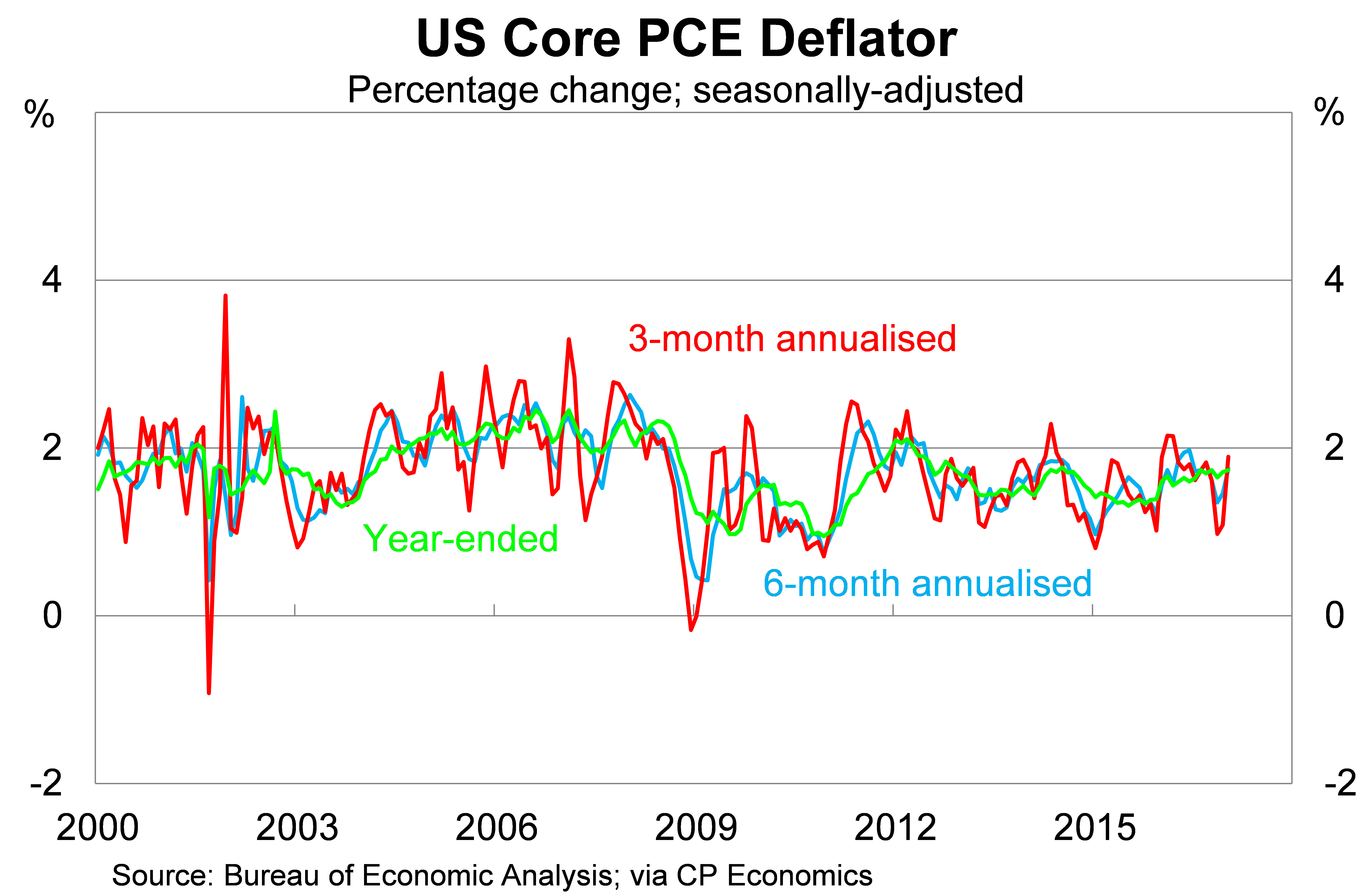

Perhaps the most important is that the Federal Reserve will need to see material progress towards meeting its inflation objectives. The Fed pursues an annual inflation target of 2 per cent, based on the PCE deflator, a mark it has achieved on just four occasions since the beginning of the global financial crisis.

The core PCE deflator has increased by 1.7 per cent over the past year; though shorter-term measures indicate that inflation has picked up a little over the past three-to-six months. Part of the problem is that we haven't seen any material improvement in wage growth over the past six months.

The Fed remains ever hopeful that wage growth will begin to normalise soon. Given the ongoing pace of employment growth, that appears to be a reasonable assumption. Nevertheless, at the present time stronger wage growth remains elusive.

Higher US interest rates will also have important implications for the Australian dollar, capital flows and the banking sector.

First, higher US interest rates will lead to a more valuable US dollar and that will (a) lead to a depreciation of the Australian dollar; and (b) put downward pressure on the demand for commodities, such as iron ore and coal, that will again lead to a depreciation of the Australian dollar.

Part a) is obviously a welcome development but part b) will create some difficulties. Australia needs a lower currency to support growth in tourism and the non-mining sector. But we also benefit a great deal from higher commodity prices, which boost national income growth and feeds through to greater corporate profitability and wage growth.

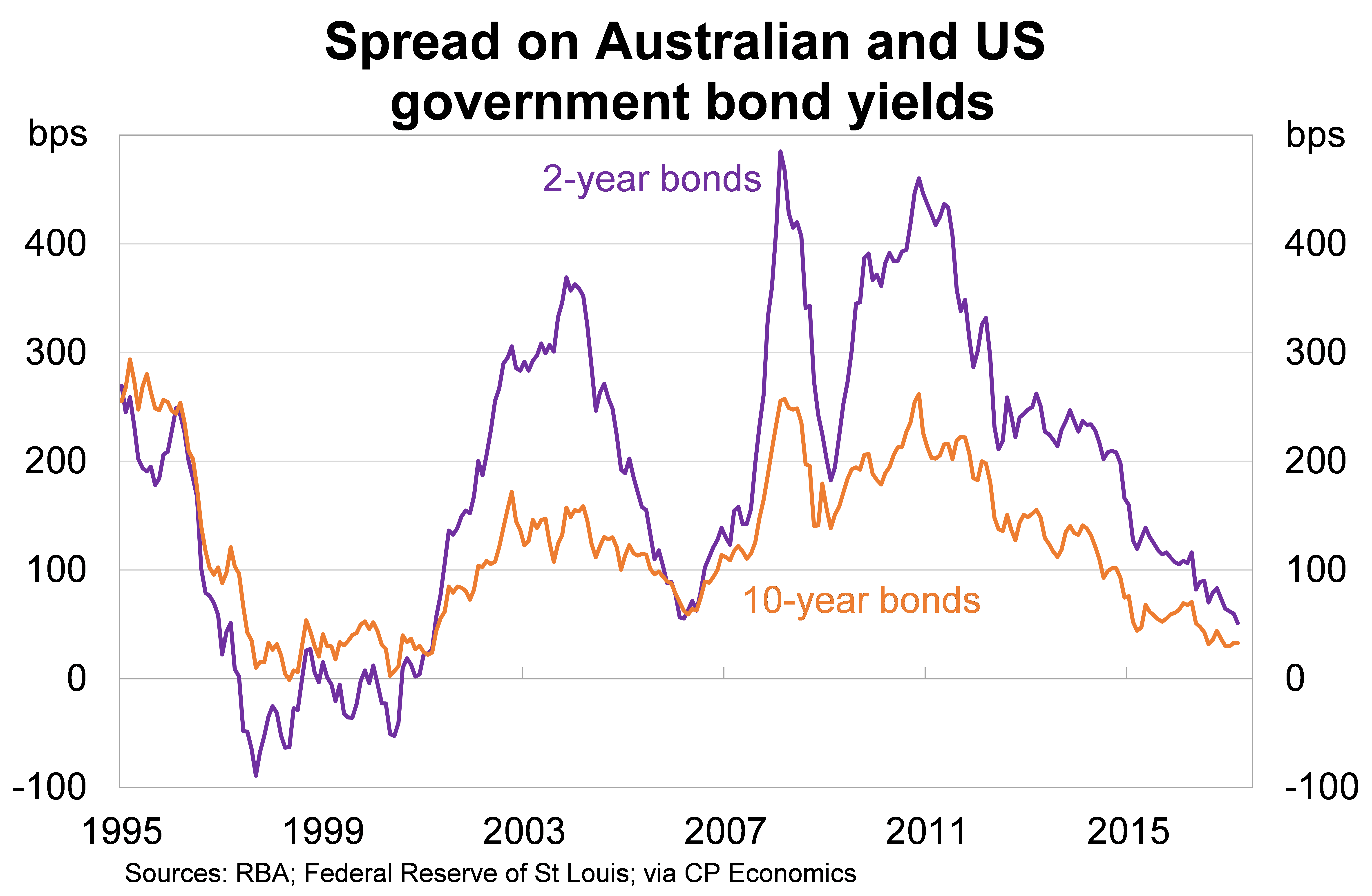

Second, higher US interest rates makes the US a more attractive destination for foreign capital. This could lead to less foreign capital inflows into Australia. One of the key measures to watch will be the spread between US and Australian government bonds – the spread has narrowed significantly over the past year and should continue to do so over the remainder of 2017.

If the spread turns negative – that is returns on US government bonds exceed returns in Australia – then I'd expect the Australian dollar to drop like a stone.

Third, higher US interest rates should increase the funding costs of Australian banks. Overseas funding for Australian banks is estimated at 51 per cent of nominal GDP – a huge amount – and any increase in the cost of those funds is likely to be passed on to consumers via higher interest rates. So don't be surprised if your bank increases your variable mortgage rates by, say, five to 10 basis points in the near future.