Exploiting low rates 1: Finding alternatives to cash

Summary: An old rule of thumb suggests keeping three years of your annual expenditure in cash. Although cash is liquid, low deposit rates mean that holding cash is costly when compared to investing the same sum in equities. Effective alternatives include disciplined use of credit cards, overdraft facilities and home equity loans. |

Key take-out: It's cheaper to keep cash balances low and selectively use credit for liquidity needs. It's important to view options such as credit cards as payment mechanisms only, taking advantage of interest free periods for purchases, while avoiding the high interest rate charged. |

Key beneficiaries: General investors. Category: Cash. |

One of the dilemmas for retirees or those close to retirement is how much of your portfolio should you keep in cash? One well accepted rule of thumb is to keep around three years of your annual expenditure in cash – with something like two years' worth to cover daily living expenses and maybe one year held as an emergency fund for health expenses etc.

The reason for cash is simple. It's liquid, so you can access it any time, without having to sell off any assets at a time when they may be correcting – something that might force an investor to crystallise a loss.

The downside is that holding cash is not costless. It yields you little in the way of return – and the best rates on offer aren't even very liquid. So according to the RBA, the average ‘bonus' savings account (which restricts the number of withdrawals) offers 3.1 per cent per annum assuming you make no or only a limited number of withdrawals. Your stock standard savings account offers slightly less at 2.25 per cent, while term deposit rates vary from 2.25 per cent (for one month) up to 2.75 per cent (for three years). On average, cash accounts offer a yield of about 2.7 per cent.

So on that basis, you've got three years of annual expenditure sitting in cash, earning at best 3.1 per cent or on average 2.7 per cent. Fairly abysmal whichever way you look at it when you compare them to the grossed up dividend yield of the ASX200 (of around 6 per cent) – or higher if you look at the banks or Telstra.

If that wasn't bad enough, we know the attractiveness of cash is set to decline further still, with the market currently pricing in two more rate cuts by the end of the year. That would bring the RBA's cash rate to 1.75 per cent and the best deposit rate available for investors down to about 2.5 per cent.

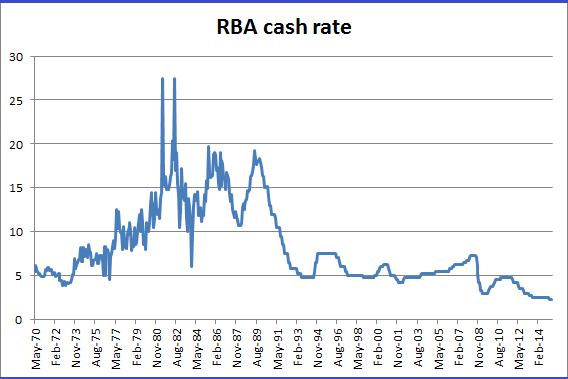

Figure 1: RBA cash rate since 1970

Source: RBA

How costly that ends up being for each retiree – in absolute dollar terms – depends on what your annual expenditure is. Which of course is related to income, lifestyle etc.

The Association of Superannuation Funds of Australia suggests that those seeking a modest lifestyle need to spend about $33,000 per year. That rises to around $60,000 for those looking to be comfortable. Using the rule of thumb that you should hold three years in cash, this implies a buffer of around $100,000 to $180,000 kept on deposit at the bank. That's a sizeable sum of money – and to keep that amount in cash would cost a lot:

· Holding $100,000 we use the difference between the market dividend yield (6 per cent) and the average deposit rate of 2.7 per cent. The difference between these two rates is what you are giving up to hold cash and is effectively the cost of holding cash. So that's 3.3 per cent pa. Applying that rate to $100,000 means you are paying $3300 per year to hold three years of income in cash.

· Holding $180,000 and using the difference between the market yield and the average deposit rate (6 per cent – 2.7 per cent = 3.3 per cent x $180,000) means holding three years income costs you $5940 per year.

That ‘cost' is what retirees are giving up by not investing in equities or other higher return assets for the sake of liquidity. Now I'm not suggesting that retirees should be 100 per cent invested in equities. A balanced and diversified portfolio is critical, no matter what stage an investor is in – just starting out or retired.

But the point remains that holding cash is expensive – it's not costless. Especially as there are effective alternatives to holding cash for liquidity needs.

So for instance a simple credit card for daily purchases can help reduce the need for holding cash. Discipline is required obviously and it's important to view the credit card as merely a payment mechanism – a cash alternative – rather than accessing it for credit. You obviously don't want to be paying the 20 per cent plus interest rate that credit cards can attract and there are much better rates on offer for credit. But for the disciplined, the 55 day interest free period that many cards have for purchases is a great way to reduce the need for holding cash on deposit and managing weekly cash expenditures.

Another method is to establish overdraft facilities. Interest rates on these facilities – which must be linked to an existing account – vary from 13-16 per cent and that's comparatively high. But if you're using it simply to manage liquidity it's a cheaper option than maintaining a large cash balance. So for instance accessing $5000 for three months on overdraft costs roughly $162.

What about for larger transactions – a medical emergency or an overseas holiday? Well here, rather than sitting down a year in advance and estimating your cash needs and depositing that in the bank – an even cheaper method might be establishing a line of credit to an existing property. Lines of credit or home equity loans – also called home equity access – offer a much cheaper alternative to holding large sums of cash on deposit.

Terms vary but for amounts up to $500,000, you can establish them with no application fee, an annual interest rate of below 5 per cent, with an ongoing annual fee of between $400-$500.

It seems to me that the old rule of thumb is actually an expensive one. It may have been okay when deposit rates were so much higher. But in an ultra-low rate world, it's actually cheaper to keep cash balances low and to selectively use credit to manage liquidity needs.