Eureka's Week: Solar, oil, RBA minutes, China, yield

Last night | Solar | Oil | Minutes | China | Yield | Readings & Viewings | Last week | Next week

Last night

Dow Jones, up 0.38%

S&P 500, up 0.6%

Nasdaq, up 1.12%

Australian dollar, US72.2c

Exciting bundle deal to kickstart your weekend

Before you get stuck into the weekend briefing, we wanted to bring to your attention this exciting offer we have put together to help you kickstart your weekend.

Right now, if you extend your membership for another 12 months, not only will you get another year of Eureka's fantastic content, but you'll also receive full access to InvestSMART.com.au (RRP $770) for only $495.

InvestSMART includes research on over 200 companies, including 54 buy and 64 sell recommendations courtesy of Intelligent Investor, along with 10 model portfolios tailored to a range of investment goals.

It's a great offer, representing a saving of over 50%. Here are more details: bundle deal.

Solar

I met the MD of a UK company called Oxford PV this week, Frank Averdung. The company is a spin-off from Oxford University based on a new material for solar power cells called Perovskite, which is apparently getting some traction. Frank is in town trying to raise some venture capital money here.

The reason for talking about it, and making it the first item this week, is that he told me about something that happened in Dubai earlier this month that had passed me by: an auction for the right to build a new solar power generator has produced the first ever bids below 3c per kilowatt hour.

The deal was won by a consortium of an Abu Dhabi renewable energy developer Masdar and a Spanish firm called FRV which has built two large scale solar farms in Australia – one in ACT and one in Moree.

The point is that the auction in Dubai confirms that solar is now the cheapest form of electricity. This is a huge development.

It's true that we're talking Dubai, where there's rather a lot of sun, and the facility won't be generating electricity till 2018, but the standard cost of coal power generation is 6-7c per KwH, so there's now quite a big buffer between the cost of fossil fuel electricity and solar.

Last year the growth in global energy consumption was one per cent. The growth in renewables, according to Frank Averdung, was 25 per cent.

Here are some big facts: the total world consumption of electricity is 18.5 terawatt years (TwY), which is forecast to grow to 28 TwY by 2050. (That's 18.5 billion and 28 billion kilowatt hours (KwH).)

The maximum potential power from all the wind blowing around the earth is apparently 75-130 TwY, but the planet would have to be more or less covered by windmills, which might look untidy.

The amount of electricity available from photons hitting the earth's surface from the sun is 23,000 TwY per year.

The two main problems with solar have been cost and intermittency (there's no power when the sun's not shining).

Both of these problems have more or less been solved now: the second by battery storage technology, which is producing a lithium boom, and the first through the rapidly declining cost of solar PV.

Eight years ago the price of silicon was $470 per kilogram; now it's $15. Silicon only represents nine per cent of the cost of installed PV (residential), so while it's important, the main thing is improving efficiency in installing it and extracting more electricity from the photons.

Oxford PV's Perovskite apparently provides a big improvement in efficiency, which will lower the cost further. Unfortunately it's not available to retail investors yet so this is not a pitch for you to invest in it (I won't be investing either, not that they asked me to).

Over the past couple of decades, we've been witnessing, and experiencing, a succession of technological revolutions that are having a massive impact on us as investors – algorithmic trading, cloud computing, social media, online retailing and so on.

The switch to solar power, now the cheapest form of electricity, is potentially the biggest of them all.

Oil

A discussion of the oil price naturally flows from the above. The rally to $US50 a barrel has prompted a re-emergence of the bulls: hedge fund long positions on NYMEX (bets that the oil price will rise) are near the all-time record levels of June 2014.

That was just before the oil price peaked at $US120 and then collapsed, so what hedge funds are betting on can be seen as a counter indicator – a “kiss of death”.

The collapse in the cost of generating and storing solar power is the main reason to think that $US50 is a ceiling for the oil, not the start of another long rally, and therefore the new floor, but there's more.

Oil prices are no longer controlled by Saudi Arabia or OPEC. This has been demonstrated again over the past month by the fact that the price rose after Saudi Arabia failed to agree production cuts with Russia. The Saudis, Russians and Iranians are all now producing oil flat out for cash, and will keep doing so because cartel behaviour is now pointless with UAS shale producers sitting there ready to flood the market at any opportunity.

This means that oil is now just like any other commodity, with the price determined by the least efficient supplier whose production is needed to meet demand.

In other words, with the destruction of OPEC, the price will be set by the marginal costs of the US shale and Canadian tar sands producers (when demand is strong) and by the Middle East producers when demand is weak. It won't be set by the budgetary needs of Russia and Saudi Arabia, or what the big oil companies have found or even by temporary disruptions like the recent ones in Nigeria.

That suggests a maximum, not minimum, price of $US50 a barrel.

Share markets have tended to move in a direct relationship with the oil price, rather than inverse, as you would expect. A lot of investors are still seeing the oil price collapse as a bearish signal for global growth and investing.

This is another short-term marginal pricing issue: it will take a while for the benefits of cheap oil to flow through, whereas the negative impact on those directly affected by lower oil prices is more immediate. Also the effect on overall market indices is magnified when traders react to the prospects of oil producers and their bankers, but that's not offset by the long term benefits because they're too far off.

The fact that solar is now cheaper than fossil fuel electricity means that much of the oil and coal that has already discovered will become stranded assets. It means that searching for more of the stuff is a waste of time and money – a huge misallocation of capital. Yet that's what most oil (and coal) companies believe is their main skill.

In fact, as the budget positions, and political security, of the regimes in countries like Saudi Arabia and Russia continue to deteriorate they are likely to produce more and more oil at lower and lower prices. And as time goes on, supply disruptions and geopolitical events will become less important.

Minutes

There were two sets of central bank minutes this week – from the RBA and the US Federal Reserve – and they had the opposite effect on the Aussie dollar, even though interest rates in Australia and America are heading in different directions, so both central banks are outing downward pressure on the Aussie.

To sum up: the key message that markets took from the RBA minutes was that the May rate cut was line ball – that it was the subject of hot debate – while the Fed minutes confirmed that June is “live” for the next rate hike.

The result was that the AUD went up after the RBA minutes and down after the Fed minutes.

But apart from the new information that there was a debate at the May meeting, the message from the RBA minutes was that they are quite disconcerted by sudden in inflation and worried that it could become entrenched: “if inflation was to be persistently lower than previously forecast, it (is) possible that, in time, this could be reflected in lower wage growth.”

Overall, it's clear that the May cut was not a once-off – there are more coming, maybe even, as one commentator (can't remember who) suggested, down to a zero cash rate in Australia.

In my view that would be ridiculous, and both good and bad for investors – mainly bad. Let me explain.

The main thing is that RBA is singing from a song sheet that is different to normal peoples'. It has an inflation target of two to three per cent and has had since 1992. For nearly all of the time since then, the job has involved getting inflation down to below three per cent, which led to Ian Macfarlane keeping rates higher in Australia than the US during the American booms of the late 90s (internet) and mid 2000s (housing).

Now, shockingly, inflation is 1.5 per cent and apparently heading south. The good folks at the RBA suddenly have to get their heads around getting inflation UP to two per cent, rather than down to three per cent.

In a way, a central bank is a robot consisting of human beings. They have emotions and foibles like the rest of us, but come to work each day to fulfill the terms of a statutory mandate. That's because, as a group, they don't have a boss – just the public interest, as expressed through legislation and formal mandate. In other words, they have no direct political oversight, ever since the RBA was given full independence by Peter Costello.

This is really important to understand because it means that two to three per cent inflation target is not flexible. Former Govrnor Ian Macfarlane says it is, but that's not how the RBA is behaving.

Governor Glenn Stevens has been making speech and speech for a while now in which he talks about the limitations of monetary policy, and the fact that inflation is low for a variety of reasons, but he still has to try to get it up to two per cent. That's his job.

And the fact is that inflation below 2 per cent is not really a problem. It would be if it was caused by a recession, but it's not. It's caused by low commodity prices, in turn caused by excess supply not weak demand, automation and high levels debt.

Not only is it natural that average consumer prices are flat, but there's nothing the RBA can do about it anyway.

The fact that they are trying to, by cutting interest rates is both terrible for income investors and terrific for growth investors.

Obviously it's becoming harder and harder to get a decent income: the as I have written many times, retirees are the front line soldiers in the central banks' war against deflation. You are being sent over the top to be mown down by low yields.

Low and falling interest rates should be good for growth investors because it helps economic growth, stock valuations and property prices, but I think we are entering diminishing returns on this front. Valuations can't keep rising forever and lowering the price of credit can't keep boosting the economy because at some there's simply too much debt.

As for the US Fed – it's in the middle of a fascinating contradiction. The Fed funds rate is clearly in a new upcycle, and the FOMC is explicitly biased to towards increasing it. Next stop, a June rate hike.

Yet bond yields are falling again, predicting lower inflation. Breakeven inflation rates (that is, market pricing for expected inflation) is continuing to fall. Growth looks weak and both the CPI (ex shelter) and the producer price index (ex services) recorded year-on-year falls.

In a note this week, Charles Gave of GaveKal Research observed that the unadjusted CPI is only positive because the “cost of shelter (is) being driven up by asinine policy responses, and also the impact on health costs from “Obama Care”.

“Pushing up the price of shelter and health insurance can be thought of as a tax rise as the impact is to reduce disposable income for the average consumer. The effect will be to apply downward pressure on all other prices and consequently on the profits of companies operating in these markets. Seen in these terms, is it any great wonder that US long bond rates are declining? In my view they will keep falling.”

That note was headed: “Here comes US deflation”, which tells you where he's coming from. If he's right, US interest rates won't be going up for long.

China

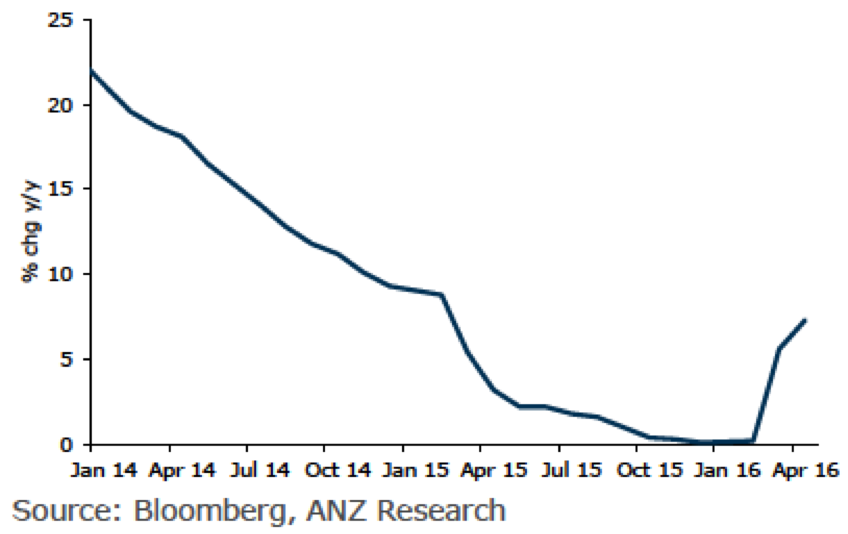

Meanwhile China just keeps powering on. GDP growth is slowing, it's true, but real estate construction, which is arguably more important for us because of its impact on steel, and therefore iron ore demand, rose 7.2 per cent in the first four months of 2016:

INVESTMENT IN CHINESE REAL ESTATE CONSTRUCTION

This is better growth than the first quarter increase of 6.2 per cent, suggesting that it accelerated in April.

For the four months property sales rose 36.5 per cent in floor space and 54.1 per cent in revenue. Inventory (floor space waiting to be sold) fell 1.1 per cent, so there's some destocking going on.

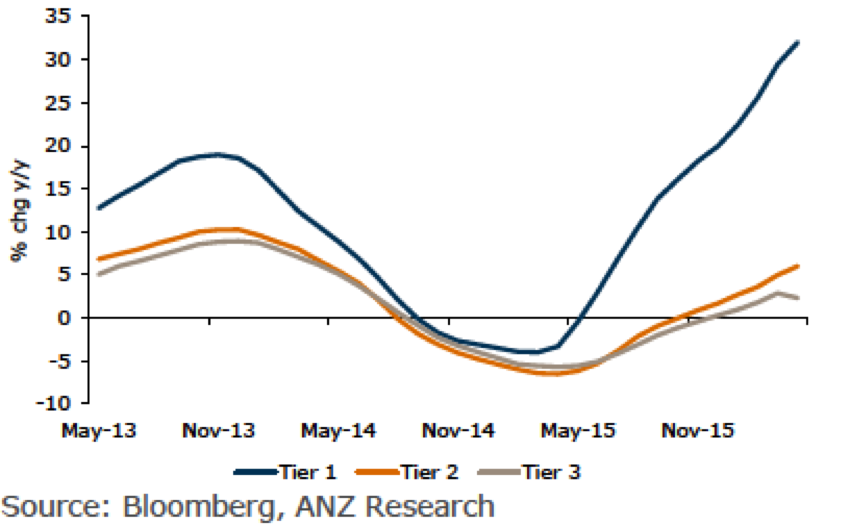

What's more house prices in China are booming, especially in the Tier One cities (Beijing, Shanghai etc):

CHINA HOUSE PRICES, BY TYPE OF CITY

All of this has seen China steel output jump to a record in April, of 2.3 million tonnes. So as regulators try to stop rampant commodity speculation in China, which is causing a fair bit of volatility, at least the fundamentals are OK – for the moment.

The key issue for China in the medium term is how will the consequences of the debt reckoning be allocated?

It's coming, you can be sure of that. Over the past few years China has been the subject of one of greatest episodes of capital misallocation in history. Debt has spiraled and investment returns have fallen because of empty apartments, factories producing for inventory and unused roads.

Debt is continuing to rise as China continues to pile on infrastructure investment (it rose 19 per cent in the year to April), while talking about structural reform and transitioning the economy to services and consumption. That's happening, but obviously too slowly for the leadership's tastes.

So the capital losses are continuing to build. At some point, I don't know when, those losses will have to be recognised, and the big question is how will they be shared. Will it be orderly, or messy? Will it result in recession and social disruption?

As with many things these days, we haven't seen a country like China go through this sort of episode before, so we don't know. Maybe the Communist Party will be able to control and absorb the unwinding in the interests of staying in power. Maybe not.

You probably think I should make a call on the future of China. Sorry. I don't have a clue.

Yield

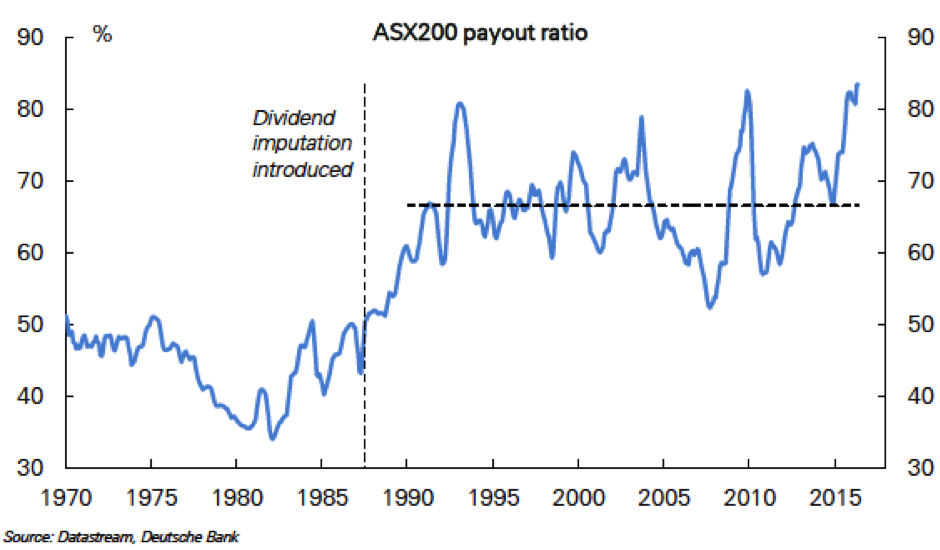

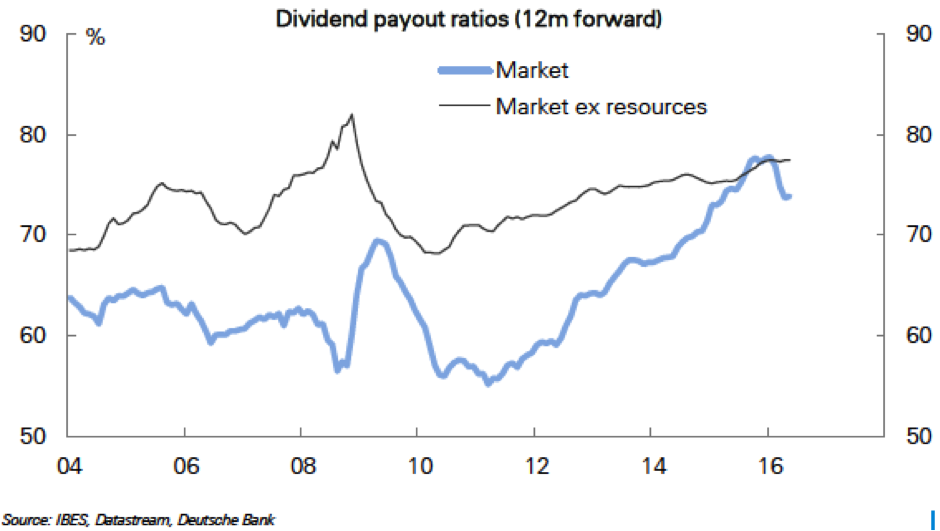

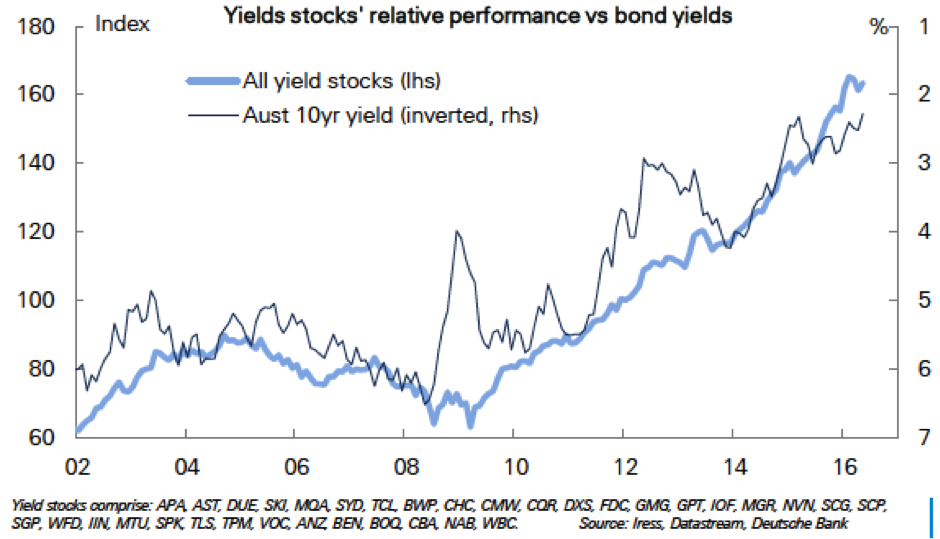

Here's an interesting, and for many investors very important set of charts from a Deutsche Bank report this week on dividends and yield in the Australian market.

At first glance you'd say the dividend payout ratio – currently at a record high – can only go down.

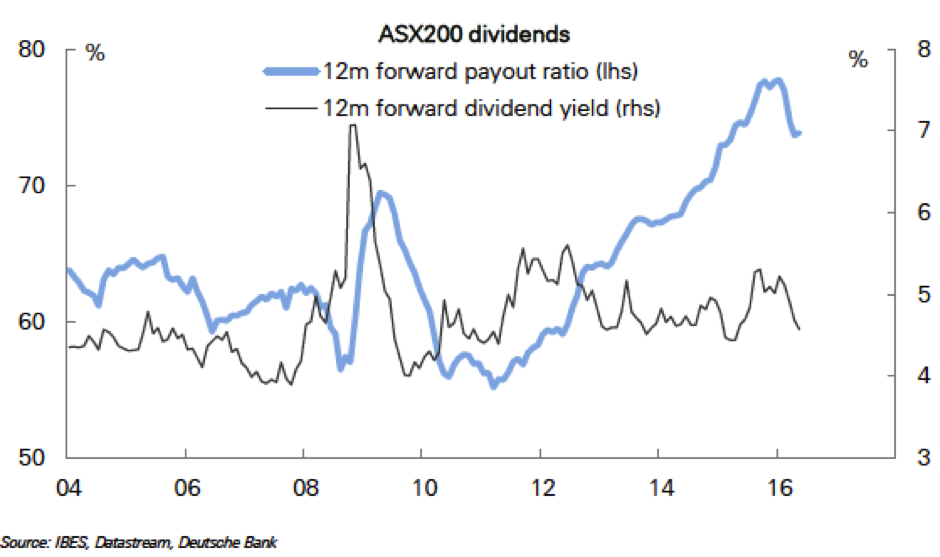

And with profits under pressure, companies are having to pay more and more of their earnings out to maintain their yield:

But a lot of this has to do with resources, and in particular BHP and Rio Tinto, which have maintained dividends. Resources represent 15 per cent of the market, but they have skewed the market payout ratio quite a lot:

Deutsche Bank reckons companies will be able to borrow to fund expansion, rather than have to cut dividends, because gearing ratios are quite low.

I'm a tad skeptical about all this. The first chart clearly shows that dividends have been boosted by companies taking their payouts ratios to a record high, and a very low dispersion among both companies and sectors suggests that it's not just a few outliers.

Dividends are clearly vulnerable, either to profit declines or the need to invest in the business.

What's more the main factor governing the performance of yield stocks is the 10-year government bond yield. If that goes up, as it must do at some point, then the banks and other high yield stocks will fall.

Readings & Viewings

I got some feedback about my comments last week about insomnia. Here's the best: “As a recovering insomniac can I tell you one thing I have learnt. Before electric light, people went to bed very early, woke up periodically, got up and did things, then went back to bed. Hence we go through sleep cycles. If you try this, you start breaking the problem into smaller pieces. One or more of the cycles will be good or OK. You get things done and don`t completely waste the night. It is a start – from Dan.” I've basically broken through after a few nights of not much sleep, and I'm sleeping through the night most of the time, but if I don't, I just do what Dan suggests. No problems!

Jeff Bezos says the debate between security and privacy is the “issue of our age”. Yeah, I guess it might be.

Nice video explaining the grandfather paradox – where if you went back in time, and killed your grandfather, you wouldn't be born and therefore could go back in time to kill your grandfather.

And more science: wormholes explained in three minutes. (Or not – I'm still confused).

The guys at Livewire are doing a fine job of publishing views and videos with local fund managers. You can either set up your own alerts here, or just let me keep picking the eyes out of it each week. Here's a video on investing in small caps, with three excellent fund managers, who know all about this subject – Matthew Kidman, Chris Stott of Wilson Asset Management and Mark Devcich of Pie Funds.

A sceptical take on scepticism.

Science fiction stories are looking more like reality than ever before.

My old friend John Spooner was let go by The Age last week. Here's a gallery of his best work.

If meat eaters acted like vegans (very funny).

Goldman says the oil surplus has come to a “sudden halt”.

Equity crowdfunding is dead – we are seeing the rise of marketplace investing.

Another video from Livewire: Chad Slater from Morphic Asset Management says the RBA is stoking a massive asset bubble.

Here's a chart shows when people are at their happiest (hint: I've got 20 years to wait).

How to deal with Germany's (and perhaps our?) opposition to immigration and refugees.

How inventing riddles has revealed the flaws in our grasp of reality.

Why a staggering number of Americans have stopped using the Internet the way they used to.

Is this the end of sex? (It's a piece about all the new ways to make babies, and wonders whether we need to, um, do it any more).

China's horrible Cultural Revolution is starting to be debated.

Ideas for reducing the global debt burden (it may be too late).

In praise of the quiet life.

High fees, lousy returns – have hedge funds lost their swagger?

The foul reign of the biological clock (one for our daughters perhaps).

Confused about the Medicare rebate freeze? Here's what you need to know.

A ripper of a Clarke and Dawe, with John doing Bill Shorten.

Happy Martin Carthy, 75 today. He's was one of the talents behind Steeleye Span, one of my all-time favourite bands. Here they are doing Gaudete. Maddy Prior sends shivers up the spine.

And happy birthday Kevin Shields, founder of the Dublin band, My Bloody Valentine. This is an interesting video about the way he plays the guitar, and it sort of explains the band a bit too.

Last week

Shane Oliver, AMP

Investment markets and key developments over the past week

Share markets were constrained over the past week by renewed talk of Fed tightening with US, European and Chinese shares falling. However, Japanese shares benefitted from a fall in the value of the Yen and the Australian share market rose slightly led by health and energy shares. In fact the Australian share market is the only major global share market to be up this year. Bond yields generally rose as investors moved to factor in a higher probability of a Fed hike next month and this also saw the $US push higher again. While the stronger $US weighed on the $A and metal prices the oil price managed to push higher. The iron ore price continued to slip and has now reversed half of its bounce from its December low of $US38/tonne to its April high of $US70/tonne as speculative forces in China have waned and the global steel glut remains.

After five months of a lot of noise but inaction, the Fed is clearly edging towards another rate hike, with the June meeting “live” for a hike and a move in the summer looking likely. The minutes from the Fed's last meeting were far more hawkish than the statement released immediately after the meeting, the key comment being that most Fed meeting participants felt that a hike at the Fed's June 14-15 meeting would be likely be appropriate if incoming data was supportive. In recent weeks it's arguable that recent data has been supportive of a hike with signs that June quarter GDP growth is picking up, continued labour market strength and inflation edging towards the 2% target. So quite clearly the June meeting will see serious consideration given to a hike and this has seen the US money market's probability of a June hike move up to 28% from close to zero only a week or so ago.

My view is that while a June Fed hike is now a close call, a July or September hike is more likely because: the Brexit vote will take place just one week after the June meeting and several Fed officials have indicated that the Fed will consider that; Fed voting members appear to be more cautious than the full range of Fed meeting participants who include non-voting regional presidents who tend to be more hawkish; and the Fed will likely need more time to assess recent data releases which have only just started to improve again. So at this stage our base case is for a July move.

More broadly we remain of the view that Fed hikes will be very gradual with constrained global growth and the risk that the $US will start to surge higher again creating renewed weakness in commodity prices, Renminbi deprecation, pressure on emerging countries and a brake on US growth all acting to constrain by how much and how quickly the Fed can hike.

Ho hum PEFO. The Australian Pre-election Economic and Fiscal Outlook was a bit boring in that it was based on the same underlying assumptions that were in the Budget because the economic and fiscal outlook “has not materially changed” since the Budget on May 3. So as a result the budget deficit projections are identical as those in the Budget. Fair enough, but a couple of risks seem to have heightened since the Budget. First, wages growth has slowed to a new record low of 2.1% and is now running well below the assumed 2.5% wages growth for the year ahead. Related to this the Budget/PEFO inflation assumptions are now above those of the RBA. Second, the iron ore price has fallen 16% since the Budget and is now running below the Budget/PEFO assumption of $US55/tonne. So the risk with the PEFO projections as with the Budget is that the assumed 6% pa plus revenue growth will not be achieved and so the return of the Budget to surplus will be pushed out even further. Unfortunately, the whole PEFO process lost significant credibility around the 2013 Federal election with the new Coalition Government revising up the budget deficit projections over the four year forward estimates compared to the 2013 PEFO by a total of $68bn just four months after PEFO was released.

What's happened to autumn? In Sydney its been more like summer lately which reminds me we are still in the grip of a serious El Nino weather phenomenon. An El Nino sees trade winds that normally blow across the Pacific to the west (La Nina) weaken or reverse causing more rain in the east Pacific and less rain/drought in the west Pacific. The Southern Oscillation Index which measures sea surface pressures across the Pacific and is one indicator of it remains deep in El Nino territory, pointing to lower farm production and higher food prices, but so far there hasn't been much sign of this. As we have seen in the past the link between El Nino and farm production varies, but it's still worth keeping an eye on.

Major global economic events and implications

US data was a bit messy with softer readings for regional manufacturing conditions surveys, a bounce in industrial production in April but after two months of falls, home builder conditions and housing starts basically trending sideways but a fall back in jobless claims and stronger leading economic indicators. The overall impression though is that GDP growth is bouncing back, albeit modestly, after the March quarter's slow down to 0.5% annualised growth. The Atlanta Fed's GDPNow growth tracker is currently estimating 2.5% annualised growth for this quarter. CPI inflation bounced in April due to higher oil prices but core inflation dipped slightly to 2.1% yoy.

Japanese GDP rose more than expected in the March quarter as did machine orders but growth has been bouncing between positive and negative quarters against a zero growth trend for the last year now and the Kumamoto earthquake may be a bit of a dampener in the current quarter.

China saw the housing market continue to hot up in April, particularly in Tier 1 cities. Meanwhile, the People's Bank of China moved to try and damp down concern about the sharp slowing in credit seen in April indicating that the drop was temporary and that it will continue to support growth. Clearly it doesn't want sentiment to swing back to the negative on China again. Our base case remains that Chinese growth will come in around or a bit above 6.5% this year. No boom but no bust either.

Australian economic events and implications

In Australia, while the minutes from the RBA's last Board meeting were interpreted as suggesting that the RBA would not be rushing to cut rates again as it awaits “further information”, March data showing a new record low in wages growth suggests that another rate cut as early as June or July is possible. While labour market data for April was pretty much as expected, increasing signs of softness after last year's strength – declining hours worked, falling full time jobs and mixed indicators from forward looking labour market indicators - also support the case for further monetary easing. So we remain of the view that the RBA will cut rates two more times this year taking the cash rate down to 1.25%. Our base case for the next move is August but it could come earlier.

Next week

Savanth Sebastian, CommSec

Business investment data in focus

The March quarter economic growth data is released on June 1. And in the coming week, pieces of the growth puzzle start to be put together. The other focal points in Australia will be speeches to be delivered by Reserve Bank officials including the Governor, Glenn Stevens.

The week kicks off on Tuesday with the release of weekly consumer confidence data from ANZ and Roy Morgan, while the Australian Bureau of Statistics is expected to release a research paper titled “Unemployment Duration in Australia” – providing a bit more colour on the employment

landscape. However the weekly confidence data will be analysed more closely given the Federal Election campaign is currently underway.

Confidence levels lifted last week after the interest rate cut. It is clear that the Federal Budget has not yet had a major impact on confidence. And it may be that the slide in the Aussie dollar has dulled the positive impact of the interest rate cut on confidence levels. Overall a lower Australian dollar is great news not just for export-orientated businesses but also the broader economy. However Aussie households tend to view a lower Australian dollar as a negative, making overseas travel and overseas online purchases more expensive.

Also on Tuesday Reserve Bank Governor Glenn Stevens will be delivering a speech at the Trans-Tasman Business Circle boardroom briefing at 1.05 pm AEST. The question and answer session following the speech is open to the media and will prove interesting.

Also on Wednesday, preliminary data on construction work is released for the March quarter. The data on residential work completed is an input into the calculation of quarterly economic growth (released on June 1).

On Thursday, the ABS will release the March quarter estimates of business investment. This data is also an input into the calculation of economic growth. But also insightful are the estimates of planned investment for the coming year.

While the Reserve Bank will be particularly interested in estimates of completed non-mining investment, there will also be focus on future spending plans. In the March quarter the first estimate of investment in 2016/17 was just $82.57 billion (weakest result since 2007/08), and 19.5 per cent lower than the first estimate for 2015/16 – marking the largest fall for a first estimate reading in records going back 25 years.

Overall we expect that investment fell by 3.5 per cent in the quarter, reflecting the winding down of the mining construction boom.

Also on Thursday, the Reserve Bank Assistant Governor (Financial Markets), Guy Debelle, delivers a speech at the Forex Network Conference in New York (11.00 pm AEST). And Assistant Governor Debelle is back on Friday as a panel participant at the ACIFMA America event on the BIS FX code (8.30 am AEST). Mixed bag of US economic data; Fed Chair Yellen to speak

In the US, there is the usual bevy of economic indicators to be released with the focus on the housing sector. Also over the week a number of Federal Reserve officials will give speeches, including chair, Janet Yellen.

The week kicks off on Monday with the Markit “flash” estimates of manufacturing activity in US, Japan and Europe.

On Tuesday in the US, new home sales is released alongside the influential Richmond Federal Reserve index. New home sales are expected to have lifted by 1.8 per cent in April after falling by 1.5 per cent in March.

On Wednesday the preliminary reading of the Markit services sector index is released in the US together the Federal Housing Finance Agency home price series and the usual weekly data on home purchase and refinancing. Annual growth rate of home prices may have edged up from 5.7 per cent to 5.8 per cent in March.

On Thursday, estimates on durable goods orders – a proxy for business investment – are released together with the usual weekly data on new claims for unemployment insurance (jobless claims) and pending home sales. And just like new home sales, pending sales may have lifted by around 1 per cent in April.

And on Friday in the US, the second (preliminary) estimate of economic growth is released with personal income, consumption data and consumer sentiment. US economic growth may have lifted at a 0.8 per cent annual rate in the March quarter, up from the “advance” reading of 0.5 per cent. The Federal Reserve's preferred inflation estimate is contained in the personal income release.

Also on Friday Federal Reserve Chair, Janet Yellen, participates in a panel titled “Building an economy for prosperity and equality.” Sharemarket, interest rates, currencies & commodities"

There has been a lot of interest in the recent slide of the Australian dollar. The Aussie dollar was near US77.2 cents just over a fortnight ago, ahead of the Reserve Bank interest rate decision. And given the surprising rate cut and change in Reserve Bank inflation forecasts, the Aussie dollar fell to lows near US72.35 cents earlier this week.

The question is where to for the currency from here? CBA currency strategists have released updated currency forecasts – lowering end 2016 forecasts from US78 cents to US73 cents. Expectations of a further two rate cuts in Australia and a lower forecast profile for the US federal funds rate – with only one rate hike now expected in 2016 – were the drivers of the lower Aussie dollar forecast.