Eureka's Week: Defensive stocks, 'full assets', CBA results

- {{x.value}}

{{ twilioFailed ? 'SMS Code Failed to Send…' : 'Enter verification code' }}

{{ completedStep1 ? 'Authentication & Security' : content.trialHeading.replace('{0}', user.FirstName) }}

{{ content.upgradeHeading.replace('{0}', user.FirstName) }}

The email address you entered is registered with InvestSMART

Please login to continue

We have sent you an email with the details of your registration.

Looks you are already a member. Please enter your password to proceed

{{ upgradeCTAText }}

Updating information

Please wait ...

Your membership to InvestSMART Group recently failed to renew.

Please make sure your payment details are up to date to continue your membership.

Having trouble renewing?

Please contact Member Services on support@investsmart.com.au or 1300 880 160

You've recently updated your payment details.

It may take a few minutes to update your subscription details, during this time you will not be able to view locked content.

If you are still having trouble viewing content after 10 minutes, try logging out of your account and logging back in.

Still having trouble viewing content?

Please contact Member Services on support@investsmart.com.au or 1300 880 160

Please click on the ACTIVATE button to activate your Intelligent Investor 15-day free trial

Please click on the ACTIVATE button to finalise your membership

Unsuccessful registration

Registration for this event is available only to Eureka Report members. View our membership page for more information.

Registration for this event is available only to Intelligent Investor members. View our membership page for more information.

- You are already registered for this event.

- This event is already full.

- Please select a quantity for at least one ticket.

- {{ i }}

Forgotten password

Please enter your email address below to request a new password

- Verify your email address by clicking on the link we sent to {{user.Email}}

- You now have free access, we look forward to helping you on your financial journey.

Eureka's Week

John Addis

Getting your defences right

It's often a warning sign if you can easily get stock in an Initial Public Offering. The best floats are the ones where most investors can't get an allocation – another reason to pass on most IPOs.

But floats are useful in one respect: opportunistic sellers rush to market when they know they can get a good price. IPOs are a financial beauty parade, a signifier of what's hot. And what's hot right now are the most boring, easily-analysed stocks imaginable.

In the last four years about 20 Australian Real Estate Investment Trusts (AREITs) have hit the boards, of which Viva Energy Real Estate Investment Trust is the most recent. Viva owns 425 service stations and was sold at a 10 per cent premium to its $2 per share net tangible asset backing, a forward yield of 5.9 per cent. Yesterday, it closed at $2.52, pushing the current forward yield down to 5.7 per cent.

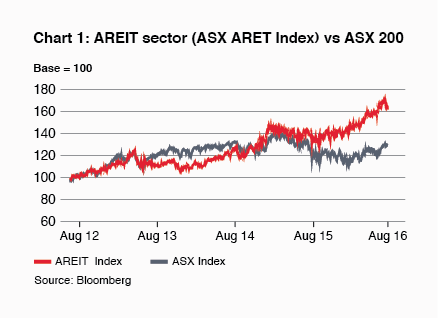

Viva is not an exception. The AREIT sector has been a ripper performer over the past four years, at this chart shows:

It's not hard to see how we got here. After the Global Financial Crisis central banks loaded up on government bonds by the trillion and, trying to reboot economies, pushed interest rates down. The more nothing happened the lower rates fell. So income investors fled the bond market in favour of equities that offered a semi-respectable yield.

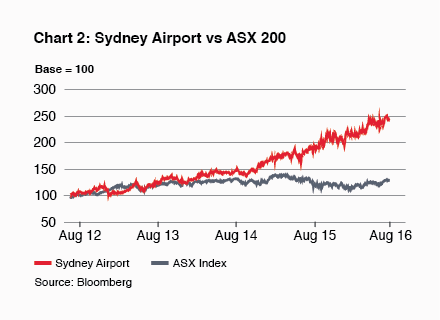

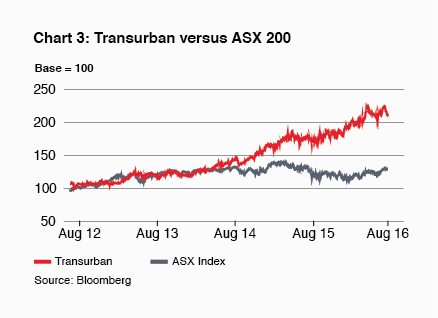

They found it not just in AREITs but also in 'bond proxies' like utilities, consumer staples and infrastructure stocks (they used to be called 'defensives' but no matter). This has led to some quite astounding share price rises, especially in highly leveraged stocks like Sydney Airport and Transurban, which have also benefited from lower debt financing costs.

Sydney Airport shares have doubled in three years while Transurban's have risen 80 per cent (see our latest reviews here and here). Great businesses both, but I can't for a moment comprehend such price rises without interest rates at historical lows. Should they start rising you'd imagine a reverse of some kind.

Not many commentators dispute that; the issue is when. The pervasive popularity of 'lower for longer' suggests investors in bond proxies need not panic sell. But if they do opt out, their problems may only multiply. Attractive alternatives are thin on the ground. Famed value investor Howard Marks told the AFR this week: "Asset prices are full today. I don't think we're in a bubble. But I view them as on 'the high side of fair' which means nothing is a bargain - nothing is available at laughably cheap prices."

That's pretty right. This is a difficult, demanding environment. We're finding some good opportunities in smaller companies but our Buy List features only 13 stocks, four of which are speculative. It's the shortest list I can remember.

Still, it's not the absence of opportunity that worries me. Attractive situations pop up if one is patient and looking in places where others aren't. My biggest concern is that too many investors are mistaking defensive businesses for defensive investments, and they are not the same thing.

Just because a company has a history of stable profit growth and sports a dividend yield that would embarrass a bond trader (not easily embarrassed, that lot) does not mean it's worth 50 per cent more than the rest of the market. A defensive company on a high multiple and a low dividend yield can still suffer a substantial price fall even when earnings are increasing.

If you own stocks that are structurally linked to declining bond yields - AREITs, infrastructure firms and utilities, for example - and those that are highly leveraged, please ensure your portfolio allocations are sensible (we publish recommended maximum portfolio weightings for this very reason). This is one risk best managed through allocation rather than a straight hold-or-sell decision.

Finally, and for the record, I sold out of Sydney Airport - which has both debt and bond proxy characteristics - in November last year when the price was $6.46. Our current recommendation is Hold. More fool me.

New faces at Eureka Report

On another note, one welcome and one departure. This will be editor Emma Koehn's last week at Eureka Report. In fact, she's probably tucking into a relaxing Saturday morning café breakfast right now with not a care in the world. She's done an amazing job under sometimes trying circumstances. Best of luck in your future journalistic endeavours Emma, and thank you from everyone for all your efforts.

In her place returns a familiar face. For many years Tony Kaye was Eureka's editor and has been a regular contributor for over a decade. A skilled writer and editor, it's lovely to have him aboard. Welcome Tony.

Readings & viewings

'Following the smart money [i.e. billionaires' money]' is a long pursued strategy - but sometimes isn't that smart.

Here's the best social media could muster from #CensusFail.

Capitalism, or at least the contemporary globalised version of it, may have pulled hundreds of millions out of poverty but it's also turned us into raving narcissists.

News Corp has been on the Intelligent Investor Buy List for over three years. This article argues the alleged indiscretions of Roger Ailes could be the best thing that ever happened to the company's cash cow, Fox News.

A whip-smart analysis of why Walmart beat Sears, and Amazon is likely to beat Walmart. (It looks like the Bezos no-profit strategy is about to pay off)

We missed this one from satirical news site The Onion last week: 'Trump campaign considers going negative'.

It has the fifth-largest economy and the sixth-strongest military but, post-Brexit, can Britain still be a powerful force in the world?

The Age's talented sports writer Greg Baum on Rio's "cut-price" opening ceremony.

Investopedia on how, historically, the stockmarket has performed over previous Olympics. (Sydney was a letdown.)

And here's an investment return that's really outperformed, largely thanks to Elvis Presley and some keen restoration experts.

Will the banks ever learn from their mistakes? In the US, bad credit lending is making a comeback.

Chinese investors are rediscovering fine art in investment, sales in the first half passing $US2bn. And what they're buying is different to the stereotype.

Meet one of the members of the ICC's Refugee Olympic Team: Yiech Biel, previously of South Sudan.

We've long been told that regular exercise can extend one's life. But new research shows that reading books will help you to live longer.

The world was on the brink of nuclear war 50 years ago, and it had little to do with humans. The culprit was a powerful solar storm.

Mitchell Sneddon's recipe of the week: "There have been calls for me to bring back the meat but that will have to wait until next week because here's a crowd pleaser for all."