Eureka's Week: Brexit fallout, mega caps, investing behaviours

What investing behaviours are you teaching? | Eureka's Week | Brexit | Mega Caps | Readings & viewings | Last week | Next week

Last night

Dow Jones, down 3.39%

S&P 500, down 3.59%

Nasdaq, down 4.12%

Aust. dollar, $US0.74.7c

British pound, $US1.37c

Paul Clitheroe

What investing behaviours are you teaching your kids?

Over the past few weeks I have been looking at some key truths about money. This is really interesting subject matter because so much said on this is complete rubbish.

How my family shaped my approach

As I look back over my 35 years working in the world of money, and the money discussions heard at home during my formative years with grandparents, parents, relatives and friends, there has certainly been a lot of dross. But at least family and friends were well meaning. One truth is that our own experiences shape our opinions on this topic. To be fair, my family's views on money were really pretty sound.

My grandparents were products of the Great Depression of 1929 to 1934, so their main view on money was not to spend it. Mind you, it was actually so conservative it was dangerous to my financial future. The kind of messages I received were your standards like: “Don't buy a house until you have saved all the money”, “debt is bad”, “shares are dangerous”, “get a job at the bank as soon as you finish school” and one very good idea that I have dismally failed to apply (and our kids are even worse on this): “Turn off the light switch as you leave a room”.

There are a lot of truths in the above, but they are too far left of the bell curve. I would not own a house today and if I had not left my job in 1983 to start my business, ipac securities, and I suspect I would be looking towards an age pension as I rapidly head towards 65. Dad, a country doctor in Griffith NSW, along with my Mum were, I think, pretty typical of their generation. Dad had just finished medicine and his hospital internship in England and his first job was volunteering to join the British Navy and spend the last couple of years of the war as a Surgeon Lieutenant on a British destroyer in the Atlantic, defending supply convoys against German U Boats. This was rarely spoken about, but from what little he said, it was not a good experience. War never is. He and my Mum, a nursing sister, met in a hospital after the war, and I think in trying to shake the war off, we moved to Australia. This was a wonderful decision for both myself and my four year old sister.

Doctors are certainly intelligent people, but generally not known, now or then, for terrific financial skills. But Dad's job as a country doctor was very secure, so he did borrow to buy a home. I remember him keenly paying down the mortgage each month. Back in the late 1960s, the tax rate hit 66 per cent as you earnt above $35,000. So as far back as I can remember Dad and his friends - doctors, lawyers, farmers and businessmen - only discussed money as it related to tax. Thank heavens he paid the house off, because investment was something done to reduce tax. And the rubbish they invested in! Dad had film schemes, not to mention nut farming and helicopters tax schemes. He seemed particularly pleased with a farm owned with his doctor partners that lost large amounts of money. HIs tax bill was never large, but he and his mates seemed to miss the point that while their taxes were low, they were making no financial progress, as these schemes were all a financial disaster.

Leading by example

You will realise by now that we are talking about our “behavioural shaping” when it comes to investing. A truth about money is that we will tend to handle it based on this shaping. In fact it is very hard for any of us to act outside our personal money zone, be that wrong or right. Luckily for me, my parents did chose to invest in shares. Even more importantly, they bought a small quantity of shares each year for my sister and I. This was really important behavioural shaping, because it got me interested in the share market. Incidentally, I should say that once my Dad gave up on tax schemes and started buying shares, his finances improved quickly. An learning moment for me was when he bought into the float of Commonwealth Serum Laboratories (CSL). As country doctors did in those days, he did part time anaesthetics so he knew how important blood serum was and would become. He bought CSL at about 67 cents a share. Today the share price is over $110. That showed me a lot about investing in what you understand.

A final piece of behavioural shaping that sits with me is that my Dad really loved his job, and always said he hoped to retire in the year he died. In fact, this is what did happen, in his 81st year.

So I got some pretty good lessons here:

1. Borrowing is OK to buy a house – but pay it off.

2. Tax schemes are rubbish.

3. Shares are good if held long term.

4. You should invest in what you understand.

5. Working well past normal retirement age (if you enjoy it) makes for few money worries.

Today's investing environment

Obviously, the environment is going to develop our money behaviour. My parents, thankfully, expanded upon the narrow finance beliefs of my grandparents, and I like to think I have expanded on my parents' beliefs too.

Some of these “experiments” have worked and some have not. With three young adult kids, my wife and I are greatly enjoying many conversations about money. We know our behaviour will have already shaped much of our childrens' lives, now and in the future. But today the environmental factors are so much more powerful. My grandparents could basically buy a house and open a bank account. They they only had their first credit card in 1980, quite late in life. The proliferation of investment ideas promising all sorts of often spurious returns did not really exist back then the way it does now.

Even Vicki and I ran into the last vestiges of a financial system that strongly regulated debt. In 1984 we trotted off (given no internet) to the bank for a loan to buy our first home, a little semi-detached house valued at $90,500. Thanks to Dad and Mum buying a few shares for me, and money we had put aside, we had a decent deposit. But I was starting my business, which horrified the bank manager. Vicki was a teacher with a secure job, but we were rejected by the bank, because: “Your wife could get pregnant any day”. Goodness. And this was 1984, not 1784. Thankfully competition had introduced these things called Building Societies – and the St George Building Society was more than happy to provide a mortgage. Off we went on our wealth creation journey.

Regular readers will know that last week I said we would be delving into the mysterious world of leverage and uncovering its truths and untruths. I have done badly here. My opening paragraph was meant to lead us straight into the world of leverage, but our money behaviour is so critical to how we handle leverage and debt, I've banged on for too long. Next week I'll get stuck straight into the murky world of debt. Believe me, the money behaviours you have absorbed to date play a big role in success or failure with leverage.

- Paul Clitheroe

Eureka's Week

Brexit is a buying opportunity

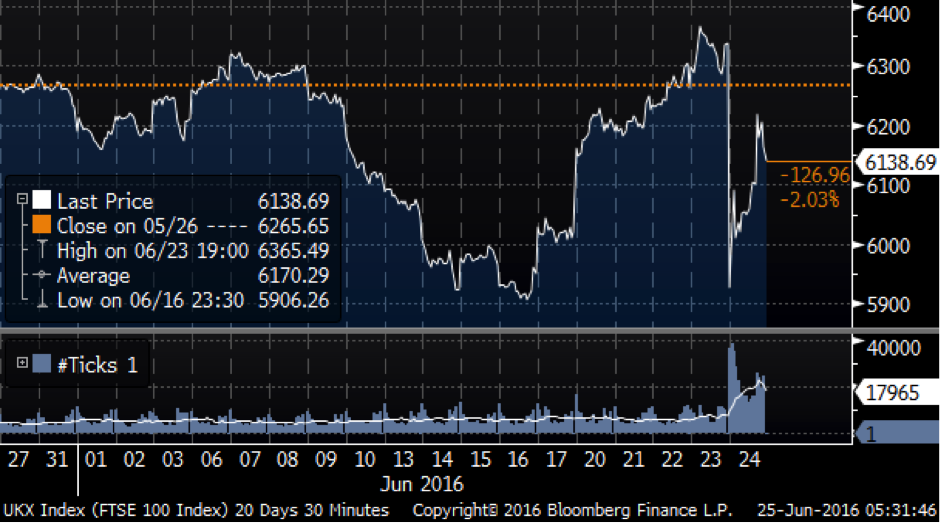

Alan Kohler here, staring at Bloomberg screens early Saturday morning. And it's been a wild 24 hours, that's for sure. Here's a three-day chart of the Australian All Ordinaries, which dropped three per cent yesterday:

As for Europe overnight, interestingly the markets in continental Europe did far worse than London: Madrid down 12.4 per cent; Milan 12.5 per cent; Athens 13.4 per cent; Paris 8 per cent; Frankfurt 6.8 per cent.

London fell only 3.2 per cent by the close, although at its low point for the session it was down 8.7 per cent. The buyers came back into UK stocks in the afternoon, which they didn't do in the European exchanges.

Here's a one month chart of the UK FTSE100, and you can clearly see that what's happened to the London stockmarket is that it has merely taken out the rally that followed the murder of Jo Cox a week ago, which caused the polls to swing back to “Remain”. Last night's action was just a correction of that.

The same cannot be said of the pound, however. It is still 2.5 per cent below the pre-rally level, but that's all it is. The talk about a 10 per cent devaluation are rubbish – that was the intra-day peak to trough, but the pound, too, rallied after that, and much of the fall was a correction of the rise that occurred after the murder of Jo Cox.

So where does all this leave us?

Well, obviously Britain has some challenges ahead. One of the three men I admire most (to quote American Pie), the Financial Times economist Martin Wolf, wrote this morning that “the UK is now at the beginning of an extended period of uncertainty that, in overwhelming probability, foreshadows a diminished future.”

He went on to say that this is could mark a significant moment in the West's retreat from globalization, and that it is, above all, a victory of the disappointed and fearful over the confident.

In short, Martin isn't happy. Nor is anyone in London really.

My daughter lives there at the moment and told me last night that her boyfriend's parents – both of them – were in tears yesterday.

I spent a lot of yesterday watching the BBC, and there was real anger towards Boris Johnson as he emerged from his house and climbed into a car. How ironic if he becomes Prime Minister: Boris is the quintessential Londoner, but he would come into office without London behind him, and with the support of Midlands, North and the South (and not Scotland).

Thanks to this referendum taking place, there are now divisions in UK between the young and old, rich and poor, London and the rest, which will remain open and unsettling for some time.

Britain's vote also destabilises Europe as a whole, which is why the stockmarkets on the continent fell so much last night: people in other countries will obviously start to agitate for the same thing.

In fact Eurozone stocks have underperformed ever since the GFC because of constant fears, usually caused by Greece, of a break-up of the EU, apart from a year after Mario Draghi's “whatever it takes” statement.

And the truth is that two decades of the EU and its attempt to cram such different peoples and cultures into the same lederhosen have simply not delivered on the promises that were made. As a result a large and growing minority feel duped by the EU, understandably – they were!

More generally there clearly is, as Martin Wolf wrote, a backlash in the West against globalisation and capitalism, which finding its most dangerous expression in Donald Trump. But it's much more widespread and complex than that: there's Beppe Grillo's Five Star movement in Italy, Marine Le Pen's National Front in France, the right wingers in Australia and Germany – all gaining traction.

The Brexit could be the beginning of the end for the EU, but that doesn't particularly worry me. The shining ideal of a United States of Europe that many hold to is not only no closer than it was 20 years ago, it is impossible, and would be no great thing anyway.

And the half-way house of an unelected and unaccountable European Commission is dreadful, and shouldn't survive, so it probably won't.

But all this will take a long time and the end result is very uncertain. Countries that are in the EU, but also signed up for the euro, are in an entirely different position to the UK: for them, exit from the EU and the Eurozone would likely be catastrophic because their banking systems would collapse.

That's why there was such a panic in Athens, Milan and Madrid last night.

But overall I think Brexit is another buying opportunity.

With all scary economic and market events that are known about ahead of time, the doomsayers always overstate their case.

It happened with Y2K, the US debt ceiling panic, various Greek loan repayment emergencies, and peak oil, to name a few. The only times the future negatives aren't exaggerated are “black swans” that no one sees coming, and then markets just catch up, by overreacting afterwards.

As a result, virtually every negative market shock is a buying opportunity, and I don't think this one will be an exception. (The only exception I can remember was the UK's emergency nationalisation of Northern Rock in February 2008, which resulted in panic which was initially taken as a buying opportunity, so the market spiked in March. But it was actually a time to run for your life.)

With the UK referendum, both sides have overstated their cases. Brexit is unlikely to be a disaster for either the UK, Europe or the global economy, and remaining in the EU, especially by a narrow vote, would have solved nothing.

Markets panicked yesterday and last night, but the fact that the vote is non-binding, the process of exiting will take a long time, that the result will depend entirely on the exit arrangements, and will end up being nowhere near as damaging as the Remainers have predicted is beside the point: volatility itself is the game.

Short term volatility is both upsetting for the public and profitable for traders who set marginal asset prices and exchange rates.

If the volatility lasts beyond a few days and sends the US dollar significantly higher for longer than a few days, it could have some fairly profound effects, such as ruling out a Fed rate hike for the rest of this year.

If the pound stays down then British industry will become more competitive and perhaps start taking market share off the Germans. The idea that the UK will lose European trade if it's not part of the EU is absurd – just ask China. They know that trade is all about price, not treaties and alliances, and price is mostly about the exchange rate.

The UK Treasury and the OECD have estimated that the cumulative impact on British GDP of exiting the EU would by five per cent over 15 years – that is it might be five per cent lower in 15 years than it would have otherwise been.

That implies the impact on annual GDP growth would be minus 0.3 per cent, which is not nothing, but hardly recessionary and likely to be swamped by other factors – especially if the pound depreciates and stays down.

In any case, the effect would depend entirely on the exit deal that the British Government actually negotiates, if it does.

Under the Lisbon Treaty if a country notifies the European Commission of its intention to leave, then a withdrawal agreement has to be negotiated. This can take up to two years, at which point membership of the EU simply lapses, and it's likely that the British Government will take all of the two years.

The negotiation would revolve around the trade relationship the UK would have with Europe. Would it be part of the European Economic Area with Iceland and Norway, and therefore continue to enjoy free trade access to Europe?

Probably not, since the UK would still have to accept the free movement of people and contribute to the EU budget, without having any say at all in the rules.

Or perhaps the relationship will be like Switzerland's, which is based on a series of mutually dependent bilateral agreements that effectively mirror the EU treaties, but give at least the feeling of sovereignty.

In 2014 the Swiss actually exercised that sovereignty by passing a referendum imposing quotas on the free movement of people, which will theoretically collapse the whole house of cards of Swiss-EU treaties. The referendum gives the Government three years to impose quotas on immigration, so that has a year to go.

In any case, the impact of Brexit on the UK economy will depend entirely on the deal that is negotiated over the next two years or so, and then it will take a while for the effect to be felt.

As for the rest of Europe, will this be like Grexit, and lead to an eventual break-up of the Eurozone, or the EU?

The answer is: possible, but unlikely. Britain kept the pound, it didn't go with the euro. Its exit from the EU would only affect the Eurozone if other countries decide to follow it and exit both the EU and the Eurozone.

But Greece has shown why that will not happen - after all if any country was ever going to flee the euro, it would have been Greece.

It didn't, and nor would Italy, Spain or France, because bank debt would remain in euros but their assets would be in the, much lower, reborn national currency. The banking system would promptly collapse and deep recession would ensue.

In fact it's hard to think of any serious long term harm from Brexit, and certainly nothing that justify selling BHP Billiton at a price that's eight per cent below Thursday's close, as some idiots were doing yesterday afternoon, or knocking nearly five per cent off Westpac's price.

Yesterday and last night was a wild, indiscriminate risk-off moment for global traders, but these are almost always wonderful moments for the serious long term investor. For a while yesterday you could pick up BHP for less than $18 again, and Westpac for a yield of 6.7 per cent. Beautiful.

Mega Caps, mega bad

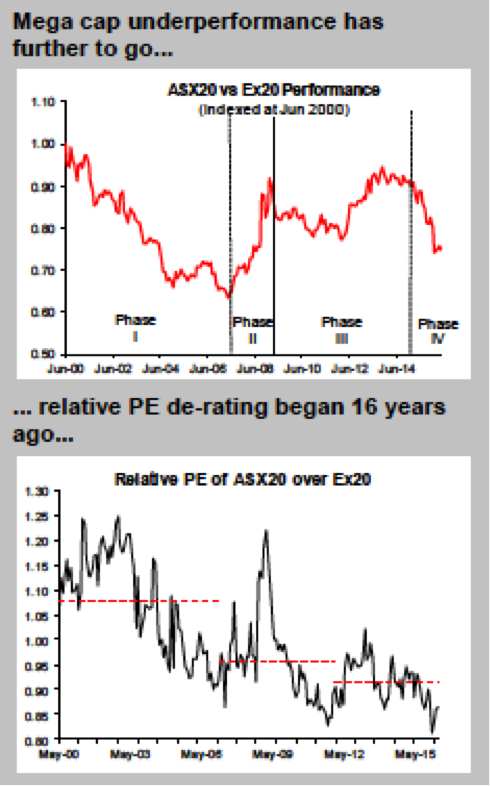

Macquarie Equities put out an important piece of research this week showing that the ASX 20 – what they call the “Mega Caps” – has underperformed the “Ex20” index (the rest of the ASX200) by 30 per cent over the past two years.

What's more they argue that this is not just a cyclical thing: fundamentals suggest it will become more drawn out.

Here are two of Macquarie's charts:

The big problem has been the performance of the banks and the big miners, and it's probably not news to you that they have done pretty poorly over the past couple of years.

So you could actually just focus on the individual stocks within the 20 leaders index, rather than look at “Mega Caps” as a group. In fact a few of them have done relatively very well indeed – Transurban, Westfield and CSL.

But there are five factors that tie the mega caps together and help explain their underperformance:

1. Mega Caps (primarily banks but including insurance and miners) are under strong regulatory and political (litigation) pressures. More stringent regulatory oversight will continue to push operating costs higher and return on capital structurally lower for banks as well as potentially slowing funds under management for self managed superannuation and limiting industry profitability for wealth managers (AMP). Also BHP and the banks are facing litigation risk as well (i.e., Samarco and BBSW rigging).

2. They operate in a number of saturated markets (Banks, Insurance, Miners, Staples, Telecoms) competing against each other for share and in some cases requiring high levels of capital expenditure for defensive rather than offensive strategies. This is most prevalent in food retailing (WOW and WES) but cuts across very nearly every consumer facing end market.

3. Mega Caps are substantial under earners. This cohort remains capitalised at a significantly higher level than the value of their earnings (approximately seven per cent). Value stocks tend to over-earn (trade on low PEs) and growth stocks tend to under-earn (trade on high PEs).

4. Australian Mega Caps are not conglomerates (outside of WES) which provide diversification and/or relative earnings stability.

5. Mega Caps are more likely to be pushed into pursuing acquisitions to support and/or drive market share (i.e. Insurance), offset declining domestic revenues (i.e. TLS) and to help drive industry consolidation (i.e. BHP and RIO). The track record of value accretive acquisitions and capital expenditure has been mixed (WES, WOW and WPL) and the risk of over paying to offset growth inertia will rise rather than decline given a weak growth and pricing backdrop.

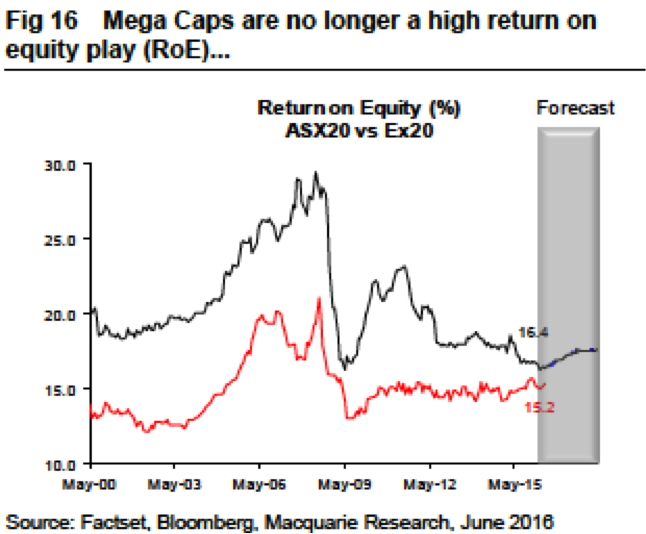

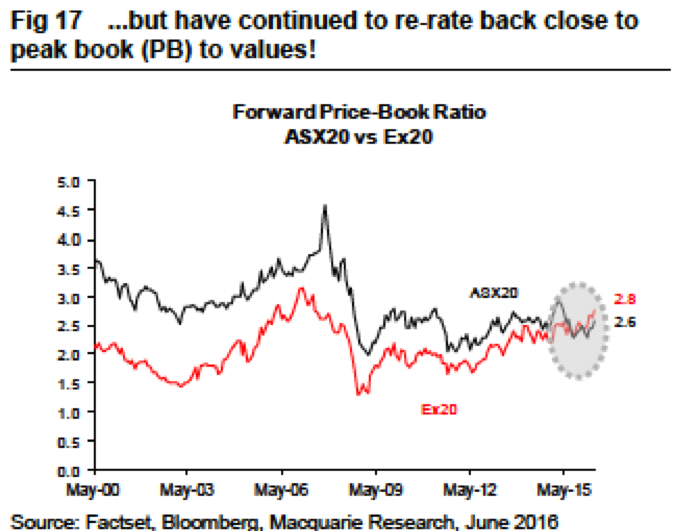

So for various reasons, the return on equity of the top 20 stocks has declined from 29.4 per cent before the financial crisis to 16.4 per cent now. This has been primarily driven by the banks and resources, but all of them have faded. Despite that, their share prices haven't fallen on a “price to book” basis (share price to book value of assets).

That suggests they have further to fall – in relative terms, that is. Macquarie's analysts reckon it could be another 15 per cent.

The point is that blue chips are not necessarily the safest place to have your money. They are perhaps less likely to go broke, and go to zero (like Dick Smith for example), but they have their own risks due purely to size and they are certainly not immune from mismanagement.

The thing is, by plonking your money into the market through an index fund you are, by definition, seeking relative performance, not absolute performance, by skewing your portfolio towards the mega caps.

But as Macquarie has shown, this strategy only works if you ignore what the rest of the market is doing and only watch the performance relative to the market as a whole. It would be like owning nothing but CBA shares and then comparing the performance of your portfolio against CBA's share price!

Readings & viewings

26 Brexit tweets guaranteed to make you laugh, cry, or probably both.

Here's Martin Wolf's piece in the FT ($) this morning, although I'm not sure you'll be able to read it. Sorry if you can't.

This piece helps explain the divide between young and old ingherent in the Brexit vote: To young people in the UK, Brexit is a door closing—and a sign that hate is winning.

What Brexit means for the City of London.

Here's a good summary of all the issues from Bloomberg.

Here is David Cameron's resignation speech in full. I thought it was pretty good.

With or without the EU, there are still many ways Europe is tied together (a really good set of infographics).

Best video of the week: Icelandic football commentator goes totally troppo when Iceland kicks second goal against Australia (it's half way down this story).

A very nice Clarke and Dawe segment, with Bryan interviewing a croaky Malcolm Turnbull (John).

Artificial intelligence – it's actually the return of the machinery question.

“To be a Trump supporter is to enter an unending psychodrama in which the country is alive with sedition.”

Trump's recent behavior demands consideration of what on earth he is doing.

How American politics went insane.

This is sort of an alternative view to that - America's middle class is shrinking not because people are getting poorer, but because they're getting richer. At least that's what this piece says.

The banality of election cynicism.

The British are suffering from national psychosis: post-imperial stress disorder.

In depth report on the state of solar power in Australia.

Maybe America should treat guns like alcohol.

Apple is the primary platform where software and services innovation is going to happen.

Genetically enhancing our children could raise interest rates.

Amazing video of a manned drone. Is this the future?

Janet Yellen has made uncertainty a new mantra.

China must overcome the politics of debt.

Great investigation, and long read, by novelist Andrew O'Hagan on the Satoshi Nakamoto affair and Bitcoin. It turns out that the “unmasking” of Craig Wright as Nakamoto was a PR stunt.

Wonderful video by Toby Young of The Spectator about why Britain should exit the EU.

Amazon is just beginning to use robots in its warehouses and they're already making a huge difference.

Last week

Shane Oliver, AMP

Investment markets and key developments over the past week

Britain votes to Leave the European Union. The past week has been dominated by first the anticipation that Britain would vote to Remain within the European Union followed by an abrupt reaction in financial markets as the referendum saw the Leave vote win by 52 per cent to 48 per cent.

Of course there will be a fair way to go before Britain actually leaves the EU – up to two years of negotiation once Britain puts in its formal notification and this will determine the terms of its leaving and hence the ultimate economic impact on the UK. If the UK negotiates free trade access like Switzerland or Norway has with the EU it will have to allow the free movement of people, agree to EU rules and regulations and contribute to its budget so it's unclear as to whether it will want to agree to that.

However, as we have seen already markets won't wait to see the final terms of the exit and are already reacting sharply. The main concern globally is not the impact on the UK economy but rather whether Brexit will kick of a round of contagion to exit amongst Eurozone countries which would then see the Eurozone unravel. It's doubtful that it will because the hurdle to leave the Eurozone is high as it will mean adopting a new currency, paying higher interest rates, etc. Just think of Greece despite its woes over the last few years consistently deciding to stay in the Eurozone. However, the risk is there, with Italy perhaps being most at risk, and markets will likely fear the worst in the short term.

Reflecting the worries about the impact on the UK and more significantly Europe financial markets have already reacted sharply in “risk off” fashion with the British pound (-8 per cent), British share futures (-8 per cent), the Euro (-3 per cent) and Eurozone share futures (-11 per cent) down sharply and this seeing global share markets down generally along with the Australian dollar. Safe haven assets such as bonds, the $US, Yen and gold have all benefitted. The likelihood is that this will all have further to go in the short term as the dust settles. A concern is that a rising $US will weigh on the Renminbi, commodity prices and emerging countries taking us back to the global growth fears we saw earlier this year.

I am not so confident about British assets given the long period of uncertainty the UK will now face both economically and politically with Scotland likely to request another independence referendum and PM Cameron weakened. However, the global bout of “risk off” now underway is likely to provide a buying opportunity as Europe is likely to hang together as it did through its sovereign debt crisis and central banks led by the Bank of England and European Central Bank are likely to run easier monetary policies than otherwise (led by liquidity boosting measures immediately) fearing an adverse financial and economic outcome.

Given that a Leave victory is unlikely to plunge the UK or Europe into an immediate recession the main impact on Australia will be on financial markets. This could affect short term confidence and may add to the case for the RBA to cut interest rates again particularly if banks increase their mortgage rates out of cycle due to higher funding costs flowing from an increase in lender caution. That said we expect the RBA to cut rates again anyway.

The key for investors is to either look through the short term noise caused by the Brexit decision or look for investment opportunities that it throws up as investment markets become oversold.

Not that it got a lot of attention given the Brexit fixation, but the German constitutional court basically approved the validity of the ECB's Outright Monetary Transaction (OMT) program, which partly underpins Draghi's 2012 commitment to do "whatever it takes" to preserve the Euro. This is a big relief because its rejection would have put a cloud over the ECB's ability to respond to any turmoil in peripheral bond markets that may flow from the Brexit vote.

Now on to other things!

In Australia, the big event in the week ahead will be the Federal election (Saturday). Each side of politics is offering very different visions for the size of government:

Labor is focussed on spending more on health and education and in the process allowing the size of the public sector to increase, funded by tax increases on higher income earners (retention of the budget deficit levy and cutbacks in access to negative gearing, the capital gains tax discount and superannuation). The ALP would also undertake a royal commission into banking and intervention in the economy is likely to be higher than under a Coalition government.

By contrast the Coalition is focussed more on containing spending, and encouraging economic growth via company tax cuts and mild reforms. Despite the Coalition's tilt to “fairness” with its super reforms it's committed to keeping taxes down. It does plan to reinstate the Australian Building & Construction Commission but even with the double dissolution election it's unclear whether it will get enough votes to do this.

At this stage the polls suggest the Australian election is too close to call. But it's a big ask to see the ALP become the first opposition in 85 years to regain government after just one term as it will need to win 19 seats. As such betting agencies have the Coalition as favourite. However, the big issue may be what happens in the Senate with there being a good chance that the Greens and minority “parties” control the balance of power again acting as a huge constraint on the government, which would mean another de facto minority government, ie more of the same. Which in turn mean poor prospects for getting government spending under control over the next three years and for implementing serious productivity enhancing economic reforms.

Over the 7 weeks since the election was called the Australian share market has tracked sideways. The next table shows that 8 out of 12 elections since 1983 saw shares up 3 months later with an average gain of 4.8 per cent. This may partly reflect relief at getting the election out of the way.

Australian shares before and after elections:

Election | Winner | Aust shares, per cent chg 8 weeks up to election | Aust shares. per cent chg 3 mths after election |

Mar 1983 | ALP | -0.6 | 19.8 |

Dec 1984 | ALP | 0.0 | 5.4 |

Jul 1987 | ALP | 3.7 | 15.9 |

Mar 1990 | ALP | -7.0 | -3.5 |

Mar 1993 | ALP | 9.0 | 3.2 |

Mar 1996 | Coalition | 2.3 | -2.0 |

Oct 1998 | Coalition | -2.6 | 11.1 |

Nov 2001 | Coalition | 5.9 | 5.4 |

Oct 2004 | Coalition | 5.9 | 9.9 |

Nov 2007 | ALP | -2.9 | -11.7 |

Aug 2010 | ALP | 0.5 | 5.7 |

Sep 2013 | Coalition | 4.6 | -1.0 |

Average | 1.6 | 4.8 | |

Jul 2016 | ? | -3.1* | ? |

* Last 7 weeks. Based on All Ords index. Source: Bloomberg, AMP Capital.

Major global economic events and implications

Fed Chair Janet Yellen's congressional testimony didn't really add much. The key is that the Fed is “proceeding cautiously” to give it time to assess whether the US economy and inflation is on track with its expectations and given global uncertainties. There was certainly no attempt by Yellen to push up market expectations for Fed hikes. Uncertainty and market turmoil flowing from the Brexit outcome is likely to further delay the Fed in terms of raising rates again. US economic data was good with the June manufacturing PMI rising, home prices up, existing home sales at their highest since 2007 and new home sales down but after a very strong result in April, jobless claims falling sharply and home prices continuing to rise. And the US's top 33 banks passed a Fed stress test indicating that they have enough capital to withstand a severe economic shock (involving unemployment doubling to 10 per cent.)

The Eurozone composite business conditions PMI fell slightly in June with a decline in services (on Brexit fears?) offsetting a gain in manufacturing. It remains at a level consistent with moderate growth though.

Japan's manufacturing conditions PMI rose just 0.1pt to a still weak 47.8 in June indicating that growth in June quarter is still struggling.

A couple of Chinese business conditions surveys moved in opposite directions for June with one up solidly and a small business PMI weakening. So bit of a wash there.

Australian economic events and implications

In Australia, the minutes from the last RBA Board meeting added little that was new with the RBA neutral and on the sidelines for now. However, our view remains that lower inflation and a too high $A on ongoing Fed delays will still see more easing ahead with the next cut likely in August. Meanwhile Australian economic data over the last week was uneventful. March quarter house prices fell slightly according to the ABS but more timely private sector data suggests a renewed pick up since then particularly in Sydney. While population growth has slowed from its 2 per cent peak late last decade to 1.4 per cent last year it's still contributing to solid underlying demand for housing. NSW and Victoria are the top states for population growth, and flowing partly from this house price growth. Which in turn partly explains the good state of their budgets. Finally, skilled vacancies continue to see reasonable growth telling us that the labour market remains solid.

Next week

Savanth Sebastian, CommSec

The financial year draws to a close

The 2015/16 financial year ends on Thursday and there will be the usual retrospective look on the year's results. There is also a healthy schedule of economic data over the week.

In Australia, the week begins on Tuesday when ANZ and Roy Morgan issue the weekly consumer sentiment reading. At present households are in a happy place, with consumer confidence at a 21⁄2-year high. Lower interest rates, cheap petrol prices and improved job security are all freeing up a few more spending dollars. However while confidence levels are solid and household budgets are looking more attractive than in the past, the focus on the upcoming Federal Election will keep a lid on spending. Encouragingly the measure on whether it is a good time to buy a major household item continues to lift – suggesting that once the election is out of the way activity levels should lift.

On Wednesday, the Housing Industry Association releases the figures on new home sales. In April new home sales declined by 4.7 per cent. The decline reflected a fall in both detached house sales and sales of multi-units. However the falls were from 7-month highs and it is likely that the low.

Interest rate environment will continue to support housing activity over the medium term

On Thursday, the Bureau of Statistics (ABS) releases two publications. The first ‘Job vacancies' provides insights into the strength of the job market. And the second, ‘National Regional Profile' (2010-14) includes ‘big picture' regional economic data.

Also on Thursday, the Reserve Bank releases the financial aggregates publication that includes data on lending (private sector credit) and the money supply. In April private sector credit (lending) rose by 0.5 per cent to stand 6.7 per cent higher than a year ago – the strongest growth in seven years. And it is likely that credit rose by a further 0.5 per cent in May once again driven by owner- occupied housing and business lending.

Friday ushers in the start of a new month and as such the focus will be on the CoreLogic release of home prices for the month of June. Interestingly home prices surged by 3.3 per cent over April and May – marking the best back-to-back gains in 10 months.

The higher home prices in Sydney and Melbourne are causing more owner-occupiers and investors to consider other markets, lifting prices in other capital cities. Hobart home prices are up by 6.1 per cent over the year, just shy of the fastest annual rate in almost six years.

The May rate cut would not have filtered through to mortgage rates till late May, and as such it is likely that home prices will continue to lift in coming months. Based on daily observations, home prices probably rose by 0.4 per cent in June.

Also on Friday, the Australia Industry Group will release the Performance of Manufacturing Index. Manufacturing activity has eased in the past couple of months but still remains in expansion territory having remained above 50 for 11 months – the longest period of expansion since September 2006. The lower Australia dollar will continue to support the sector.

US home prices and Chinese manufacturing activity dominates interest

In the US the highlight in the coming week is the release of manufacturing activity and home prices. And in China, gauges on manufacturing are also released.

The week kicks off on Monday in the US with data on advance goods trade balance – an early version of the trade data excluding services. Also on Monday the Dallas Federal Reserve manufacturing index and the Markit services index is slated for release.

On Tuesday, the CaseShiller data on home prices is released together with the third read on US GDP, consumer confidence, and the influential Richmond Fed survey. Home prices are up 5 per cent on a year earlier while confidence may have edged higher from 92.6 to 93.1. The final reading on March quarter economic growth should show that the US economy grew at a 1 per cent annualised pace.

On Wednesday, pending home sales and personal income/spending data is released. Economists tip a near 2 per cent fall in pending home sales in May after the 4.6 per cent surge in April. Some believe a housing shortage exists with the inventory of existing homes for sale down 3.6 percent in April compared with a year ago. There are signs new listing have been slowing as potential sellers worry they won't be able to find another home to buy.

On Thursday, the Chicago purchasing managers index (PMI) and the weekly initial jobless claims figures are released.

And on Friday, US vehicle sales, construction spending and the ISM manufacturing index are set for release. Total vehicle sales should hold around 17.3 million while the manufacturing index may have eased from 51.3 to 51.0 in June

In China, the official statistician (National Bureau of Statistics) releases data on industrial profits on Monday. While the purchasing managers' indexes for both the manufacturing and services sector are set for release on Friday. The Caixin variant of the manufacturing index is also issued on Friday.