ER fund manager series: Lazard Global Listed Infrastructure Fund

Summary: The Lazard Global Listed Infrastructure fund (LAZ0014AU) has $1 billion of funds under management and is one of the most established managed funds for global infrastructure exposure. Managers look for companies based in the OECD that own physical infrastructure and sustain stable revenue returns through user-pays arrangements. The fund focuses on roads and utilities, particularly in Europe where toll roads have boomed over the past five years. |

Key take out: Investors should be patient with this asset class and have a five year time frame in mind in order to get the most out of the investment – for international markets, it could be worth consulting an expert who can advise how the risks and returns will fit in your overall portfolio. |

Key beneficiaries: General investors. Category: Managed funds. |

Infrastructure is often overlooked by investors, despite the fact that it provides essential services, like electricity to our homes, roads and public transport networks. These are assets that are often immune to the fickle nature of the economic cycle, which can wreak havoc on companies that need business conditions to be as favourable as possible.

This week we introduce the Lazard Global Listed Infrastructure Fund (LAZ0014AU). An impressive track record and a whopping $1 billion funds under management makes it one of the most established managed funds specialising in infrastructure.

For domestic investors, a global infrastructure fund can be far more appealing than one focused on Australian assets only. Locally there are only a handful of listed infrastructure assets and the way in which these companies are run is often very different to their international counterparts.

It's customary for local infrastructure companies, the likes of Sydney Airport and Transurban, to pay out the majority of their profits to shareholders as dividends each year, in part succumbing to the pressures of yield-hungry investors. Many international companies don't share all of their cash with investors, leaving some money in the bank to fund maintenance expenses and upcoming projects.

In turn, this can lead to domestic companies having greater amounts of debt, potentially leaving them with less flexibility in the future. Alternatively, they need to raise capital from shareholders every few years to meet their expenses. Those who don't participate in such offerings end up having their stake in the business diluted.

While there are nuances between the way companies in different regions are run, comparatively the Australian listed infrastructure market is relatively smaller, leaving fewer investment opportunities. To get a truly diversified exposure to the asset class, a managed fund with a mandate to invest globally will help you along.

Why infrastructure?

Infrastructure assets include airports, utilities, railroads and toll roads. These are usually considered to be essential services, where the user pays for the benefit the asset provides. They also often have a monopoly in the market. For example, a toll bridge isn't likely to face direct competition considering the alternative is likely a much longer trip. And a new bridge can't be just built, either because of regulation or simply the tradeoff of cost versus profitability.

While there are high upfront costs to building infrastructure assets, they often have low ongoing costs relative to revenue collected. Generally, the usage price charged can be increased with inflation, providing a hedge to rising living costs. The user-pays system makes predicting cash flows much easier than some other business models.

Infrastructure assets won't grow earnings at the same pace as a growth company, however they can offer relatively steady and reliable income payments linked to inflation. While listed assets can easily be bought and sold, they are also subject to the same market sentiment that can send the share prices of even the best companies south. This can cause the unit price of the Lazard Global Listed Infrastructure Fund to fluctuate in tandem with wider share markets.

There is plenty of unlisted infrastructure around to be invested in, but the perks of owning listed assets lies in the ability of the fund to sell an investment if they no longer see an acceptable risk-adjusted return. This could come about when the share price trades at a much higher level than estimated valuation, or alternatively if the price is falling for an unacceptable reason.

Some market pundits have touted weak corporate earnings as a reason why the local share market is struggling to pull itself from the depths of a bear market. But infrastructure companies can be more resilient to the fortunes of the economic cycle. Generally speaking, regardless of how well the economy - local or global - is doing, we still need the utilities of infrastructure companies because they provide essential services.

The fund and strategy

The types of investments the Lazard Global Listed Infrastructure Fund likes to own are coined “preferred infrastructure” by the fund, and include those who earn regulated returns based on their cost of capital. The investment universe is comprised of listed companies based in the Organisation for Economic Cooperation and Development (OECD) that own physical infrastructure.

Almost half of the fund is currently invested in toll roads and utilities. This is based on fund's view of the opportunity these assets currently present. The evolution of toll roads means the majority of the fund's exposure to this type of asset is through Europe, where toll roads are more prominent than in the US.

The appeal of transport assets – toll roads and railroads – lies in the fact they generally have a more predictable usage pattern than some other infrastructure assets. It increases the accuracy of projecting future valuations.

In fact, the fund is tipping the future is bright for European toll roads as they have potential for upside of greater than 30 per cent. Despite the strong outlook for the sector, the fund will continue to be selective with the companies it owns by taking a concentrated approach and running a portfolio with around 30 stocks.

Rising interest rates have the potential to impact infrastructure assets negatively and management of the fund is conscious of this, meaning the portfolio is managed with this in mind.

Unlike many other actively managed funds, the fund must have less than five per cent in cash. Being fully invested takes away the option for management to try and time the market by boosting money in the bank if expectations for the short term are weak.

Having recently adjusted the minimum investment to $20,000, the fund will be more accessible to a greater number of self-directed investors. And with a management fee of 0.98 per cent per annum, it's very competitively priced for a niche asset manager.

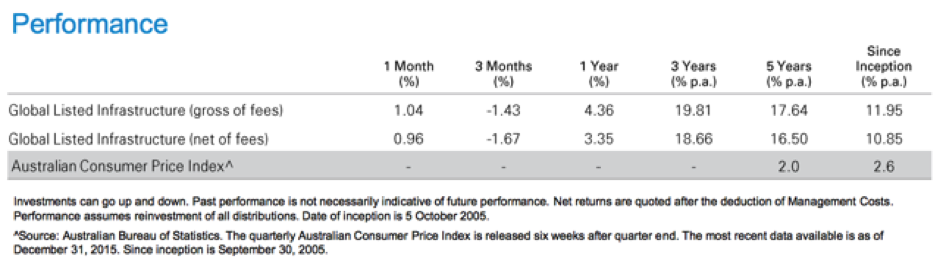

Performance

The Lazard Global Listed Infrastructure Fund has a return objective of the Consumer Price Index, plus five per cent.

The fund has an impressive track record over five years. However, management have started to revise investor expectations lower over the years ahead.

As a sector, infrastructure assets have risen strongly over the past five years, especially those listed in Europe, which was largely an unloved region to invest in at the time following the threat of sovereign default from a number of countries in the currency block.

Although financial troubles still plague some parts of the EU, it's important not to confuse a sovereign balance sheet with the balance sheet of a company. Although there has been cause for concern about the health of the economy, people have still used toll roads and paid their electricity bills.

Your portfolio

While infrastructure has many appealing traits, it should complement an existing exposure to shares, property and fixed income. As with any asset class, it can have its ups and downs and investors need to be patient and have a minimum five year investment time frame to ensure they have time to weather any unfavourable periods.

For reference, a balanced industry super fund allocated somewhere between five and 10 per cent allocated to infrastructure. This range could be a good starting point for any self-funded retiree looking to gain exposure to the asset class.

When investing internationally, it might be better to leave it to an expert. Utilities and some transport assets can operate in highly regulated environments, which means owning these companies can come with the added risk of a change in the way the market works, potentially disrupting future profitability. A manager knows the ins and outs of various regulations in different countries and can decide whether or not the threat of change makes owning the asset worthwhile or not.