Currency, oil and the reporting season

Summary: The reporting season for the first half of FY15 is now underway, with the majority of ASX-listed companies due to release their results in the next four weeks. Even when adopting a "bottom-up" stock picking approach, investors need to be aware of several key macro issues amid the increasingly volatile environment. These include the fall in the Australian dollar, the rapid drop in the oil price, management's ability to cut costs and consumer spending. |

Key take-out: Out of our current small cap recommendations, some of the companies we expect to have positive earnings results include AMA Group, Capitol Health, Vita Group, and Empired, and we expect positive commentary from Brickworks' building products division. |

Key beneficiaries: General investors. Category: Economics and Investment Strategy. |

With the majority of ASX-listed companies soon to release their results for the six months to December 31, 2014, we thought it was timely to discuss a number of the key issues that faced companies during the period.

Even when adopting a “bottom-up” stock picking approach, it is still important to consider the current macro backdrop to ensure that we are aware of some of the key risks in an increasingly volatile environment. In cyclical sectors or businesses involved in commodity or commodity like products, macro factors can have as great of an impact on earnings as stock specific factors.

Broadly we are currently focussing on the following issues:

- The fall in the Australian dollar relative to the US dollar. With further interest rate cuts possible in 2015, this decline may continue. The impacts are more significant than just a translation of earnings as it changes the company's cost and competitive position. Company specific issues such as hedging policies and the ability to pass through cost inflation are critical.

- The effects from the rapid decline in the oil price, which has followed the downturn in iron ore and other commodities.

- The ability of management teams to remove costs to combat the difficult economic environment. With numerous cost-out programs underway in recent years there has been, as yet, limited apparent improvement in margins in aggregate.

- The impact of the consumer. Despite positive consumer benefits from cheap fuel, and low interest rates vs increasing unemployment and low wages growth traditional consumer businesses appear to be struggling. Both Oroton (ORL) and Kathmandu (KMD) have recently had material share price weakness after soft trading updates.

It can be dangerous to make general macro-based assumptions without looking into detail of how the changing environment affects an individual company. Far too often we see commentators provide blanket generalisations around the impact of highly visible events, whether it be a depreciating AUD, cost of debt or oil prices. Clearly, these factors will impact different sectors in different ways – even within a sector made up of seemingly comparable businesses.

The currency effect

Despite the media coverage, the fall in the Australian dollar will have limited impact on first half FY15 results. It will, however, impact outlook comments.

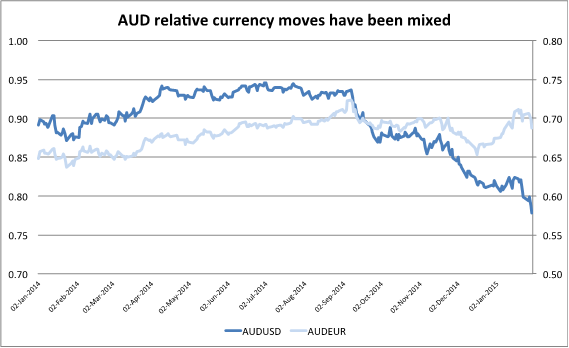

The widely anticipated capitulation of the AUD relative to the USD commenced in September 2014.

The decline is having a transformative effect on the local economy with a boost to trade exposed sectors, and exporters. Non-resource beneficiaries such as tourism and domestic manufacturing desperately need this tailwind in the current challenging environment.

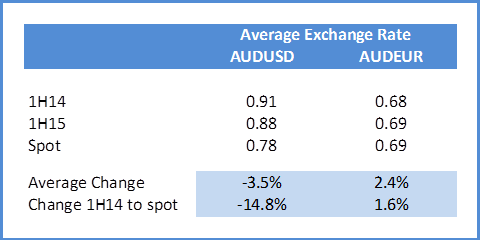

While the recent decline does have important implications for earnings and valuations going forward, there will likely be modest impact on 1H15 earnings releases with the AUD/USD declining just 3.5% on average when compared to 1H14.

Consistent with the decline in the AUD/USD, many ‘offshore' earners have re-rated in recent times.

However, it is important to note that the AUD has actually appreciated relative to the euro in 1H15 relative to 1H14 and many of these offshore earners have exposures to currencies other than the USD. They have the potential to disappoint relative to expectations.

One example is Amcor, the Australian listed packaging company. While it generates around 95% of earnings offshore, only about 30% of this is generated in North America. Furthermore, the sudden appreciation in the Swiss Franc may offset some of the overseas earnings benefit for both CSL and Cochlear in the full year result as both have operations in Switzerland.

More to currency than earnings translation

Companies with overseas earnings are obvious beneficiaries of the decline in AUD. In larger cap stocks these include Computershare (CPU), James Hardie (JHX), Aristocrat Leisure (ALL) and healthcare businesses such as Resmed (RMD) and Sonic Healthcare (SHL).

However, currency changes of the magnitude that we have seen since September 2014 have broader implications than simply the translational impacts of offshore earnings. Some such impacts include:

- Input cost inflation. Businesses who have significant input costs denominated in USD or import products acquired in USD will be at a disadvantage. Businesses with AUD denominated costs will be in a relatively favourable position (see Tim Treadgold's article on gold miners).

- Contractual details. The degree to which businesses can pass through foreign exchange led currency inflation will be important, particularly if operating in a soft end market. Some retailers will find this difficult.

- Competitive landscape. Businesses competing against imported products will be in a better relative position than they were last year. An offsetting factor to retailers who import products, and a true benefit for those that don't.

- Hedging. Hedging policies are company specific. With a decline in the AUDUSD as significant as we have seen, we expect to see some negative mark-to-market expenses reported in net interest expense.

- Balance sheet. With many company's issuing offshore debt in recent years, translated period end debt could, in some cases, see meaningful increases in AUD terms.

These are the kind of issues that we will be looking through in detail in the upcoming results. Answers to some of these important questions will not always be made clear in the results presentations and as such it can be important to listen to the analyst conference calls, and wherever possible speak with management and broader industry contacts.

The oil price

Without going into the background of why the oil price has been rapidly declining, the impact so far and on company outlooks will be another key focus.

Australia generally is a net beneficiary of the lower oil price as we are a net importer of oil. But with the LNG companies exporting gas at an oil linked price, the effect on the large pipeline of LNG projects will have an impact on government revenues.

Energy companies such as Santos (STO) have been drastically reducing capital expenditure programs, which is a hit to the mining services industry that were already battling from the iron ore downturn and general adjustment to the post mining capex environment.

Approximately 70% of WorleyParsons (WOR) earnings are exposed to hydrocarbons, with the impact partly responsible for the company's share price fall from a peak of around $54 to the current $9.60.

We currently have sell recommendations on UGL Ltd (UGL) and NRW Holdings (NWH) and generally still avoid the mining services sector despite the discounted valuations.

Rather than looking directly at energy companies and the timing of when to buy them, our focus is instead on trying to model the earnings sensitivity for industrial companies, and therefore know the impact of low oil prices on our earnings forecasts.

Transport and airline companies are obvious beneficiaries. There are also benefits for agriculture companies, manufacturers and miners.

Qantas and Virgin are well documented beneficiaries of lower fuel costs, but it is also worth considering the airport owners such as Sydney Airport (SYD) and Auckland International Airport (AIA).

Many industrial companies that are large consumers of gas have contractual pass through of their energy cost. Often these contracts are structured over long periods (greater than five years) and as a result gas intensive industries are unlikely to see the benefits that the headline decline in oil suggests – just as they didn't wear the burden when prices increased in recent years. Such examples include both Orica (ORI) and Incitec Pivot (IPL)

For the transport companies much depends on whether they pass the cost savings onto customers. In Alan Kohler's recent interview with Kim Lindsay, chief executive of the transport company Lindsay Australia (LAU), he stated that the savings from lower fuel costs are passed onto customers. This means the impact is not so much a direct increase in earnings margins but rather just the fact that their customers have lower costs and will be likely to increase volumes.

The other positive to consider from the oil price decline is the boost to household budgets and how much of this flows through to further benefits from increased discretionary spending. While this may not be a feature of 1H15 results we will be looking out for commentary around recent trading as the lower oil prices flow through to the bowser.

Eureka recommendations

We expect recent currency changes to have limited impact on 1H15 results but will be interested in the nuances on a company specific basis as well as related outlook comments.

We expect that industrial companies with high exposure to the general economy, are likely to be cautious with outlook statements and earnings guidance.

Those that display evidence of being able to grow revenue and profits in the tough economic environment are likely to be supported and see an expansion of their earnings multiple.

Out of our current small cap recommendations, some of the companies we expect to have positive earnings results include AMA Group (AMA), Capitol Health (CAJ), Vita Group (VTG), and Empired (EPD), and we expect positive commentary from Brickworks' (BKW) building products division.