Budget 2016: Why your after-tax salary is falling

Summary: Income tax liabilities for the average Australian worker have increased at nearly twice the rate of inflation over the past four financial years. While there is a misconception that bracket creep only hurts those that move to a new tax bracket, it actually effects all workers, because as wages increase a larger percentage of take home pay is taxed at the top tax bracket. |

Key take out: It's easy to see that governments are on the “getting” end of this situation, making it difficult for bracket creep to be eliminated – and meaning that “income tax reductions” touted as real cuts actually only give back the effects of bracket creep. |

Key beneficiaries: General investors. Category: Tax. |

As investors and savers eye the federal budget for any change to taxes or incentives, it's crucial for investors (and wage earners) to understand that salaries are actually dropping. No matter how hard you may be working, the stark reality is that even with rock- bottom inflation our after-tax salaries are not keeping up – inflation even at these levels is accelerating faster than wage growth.

So when you are doing the numbers around what the budget may mean to you keep this in mind.

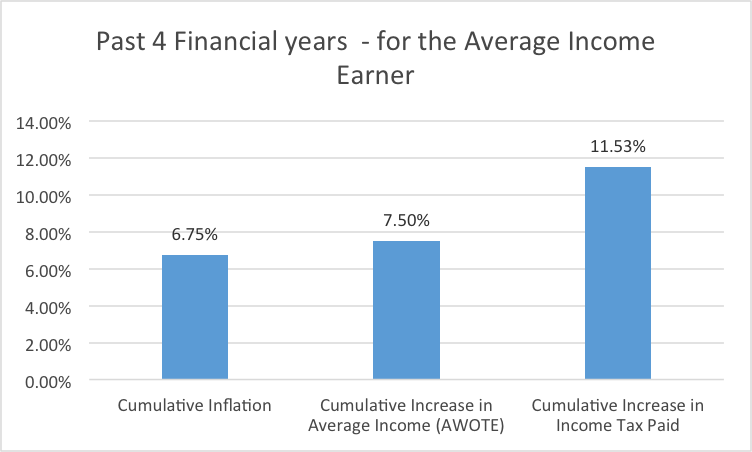

Over the past four financial years, where they have been no changes to the income tax rates or tax brackets. Yet we have seen inflation notch up a cumulative increase of 6.75 per cent. At the same time, cumulative increases in average income were 7.50 per cent and, for the average income earner, there has been an increase in income tax paid of 11.53 per cent. The reason behind income tax increasing at nearly double the rate of inflation? Bracket creep.

There is another calculation around these numbers that highlights the damage of bracket creep. In “pre tax” dollars (before the effect of income tax) a person's average income over this four year period (ending in this current financial year) rose by 7.5 per cent, above the rate of inflation of 6.75 per cent. This is what is generally expected over time – people's income grows a little faster than the rate of inflation, which allows us to buy slightly more goods and services – improving our quality of life. This all seems great until we do another calculation. Four years ago the average income earner's after tax income was $57,451. It has increased to $61,077. This means that after taking into account the impact of income tax, the after tax income of an average wage earner has increased by 6.31 per cent. Less than the rate of inflation. Over a four year period, the after tax purchasing power of an average income earner has decreased. Given that tax and inflation are realities that can't be ignored, this is the most important figure.

While I have focussed on the “average” income earner for these figures, calculations would be similar for people earning different rates of income.

With the amount of discussion around tax and tax reform, it is not surprising to hear the issue of “bracket creep” being raised from time to time – although it does not seem to be a problem that has the political will to implement what would be a fairly simple improvement, increasing the thresholds for the various tax brackets in line with inflation, or the rate of increase in wages.

The problem of bracket creep

The Australian tax system is a “progressive” tax system, meaning the rate of tax increases as a person's income increases. At a big picture level, this means that a person earning a higher income, say $150,000, pays a greater proportion of their income of tax compared to a person earning a more modest income, say $50,000.

This “progressive tax system” causes the problems of bracket creep – if tax brackets don't increase over time, as people's income increases they have more and more of their income being pushed into their highest tax brackets, increasing the proportion of their income paid as tax. For example, the 32.5 per cent tax bracket starts at an income level of $37,000. If a person's income increases from $50,000 to $55,000 they go from having $13,000 of their income taxed at the 32.5 per cent tax rate to having $18,000 taxed at the 32.5 per cent tax rate.

Table 1 – Current income tax rates (constant over the last four financial years)

0 - 18,200 | 0.00 per cent |

18,201 to 37,000 | 19.00 per cent |

37,001 to 80,000 | 32.50 per cent |

80,001 to 180,000 | 37.00 per cent |

Over 180,001 | 45.00 per cent |

A couple of misunderstandings around bracket creep

Many people think that the impact of bracket creep only hurts them if their income increases into a higher tax bracket. While it is true that having income increase into the next tax threshold might increase the impact of bracket creep, even if your income is just increasing within an income tax bracket, more and more of the income is taxed at the rate of that highest bracket.

Another income tax rate misconception that I sometimes come across around tax brackets is that as you move into a higher tax bracket you might actually end up with less take home pay because your income tax increases so much. This misunderstanding comes from thinking that all of the income is taxed at a person's highest tax bracket. However, regardless of how much a person earns the first 18,200 is taxed at a zero per cent tax rate, the next $18,800 is taxed at 19 per cent and so on.

The coming shift for average income earners into a higher tax bracket

While a person's income does not have to move into a higher tax bracket for them to be impacted by

“bracket creep”, the reality is that if they do move into a higher tax brackets the impacts will be even more significant. This is important, as the most recent measure of AWOTE (average weekly ordinary time earnings) reports an annual income of $77,963. This means that it will not be long until the average income earner starts to have some of their income taxed in the 37 per cent tax bracket, as their income increases over $80,000.

If we assume that, over the next four years, tax rates and brackets stay fixed, and the increase in inflation and average income mirror the increases of the previous four years we would expect:

– Inflation to again be 6.75 per cent

– Increase in average wages to again be 7.50 per cent (to an annual figure of $83,810)

– ncome tax paid for the average income earner to increase by an even larger 12.26 per cent, a rate higher than over the previous 4 years. The faster rate of increase in income tax comes about as increasingly more of the income is taxed in the 37 per cent tax bracket (over $80,000).

It is also important to comment on the cumulative impact of these increases over time. Over four consecutive periods the average income earner has had their income tax payable increase by 11.53 per cent and then by 12.26 per cent; well above the rate of increase in wages or inflation. Suddenly, with no appropriate adjustments in tax thresholds, income tax has become another expense (like health insurance and energy) that seems to increase at a rate significantly higher than inflation.

The political challenge

It is not hard to see why politicians don't do anything to change bracket creep – they are on the “getting” end of the significantly higher than the rate of inflation increase in income. Clearly this extra income tax revenue is a great help in the battle to balance the budget. It also means that every so often politicians can announce “income tax reductions”, that in reality often only give back the effects of bracket creep, but allow for an exciting announcement and appropriate fanfare.

Conclusion

Two headline figures stand out for me from these bracket creep calculations. The first is the way income tax liabilities for the average income earner have increased at a rate nearly twice that of inflation. The second is that bracket creep has meant that for the average income earner, their after tax income has failed to keep up with inflation over the past four years. Theoretically, a major improvement can be made by properly indexing tax thresholds. Politically, it seems more likely that politicians will hold onto the increasing income tax streams while occasionally announcing ‘tax cuts' to keep us all appropriately appreciative. However, if ever we did find a political party prepared to address this issue, they might be worthy of at least our interest.

Comments on the calculations

The most recent AWOTE figure is for the period ending October 31 2015. This is the income figure I have used for the current financial year. I have used the October figure for each of the preceding financial years.

I have only used the income tax rates in the calculation of income tax.

The four tax years where income tax brackets have not changed include the current tax year (2015/16), and the three previous years.

Frequently Asked Questions about this Article…

Bracket creep occurs when inflation and wage increases push more of your income into higher tax brackets, resulting in a higher percentage of your income being taxed. This means your after-tax salary may not keep up with inflation, effectively reducing your purchasing power over time.

Even though wages have increased slightly above inflation, the rate at which income tax has increased is nearly double that of inflation. This is due to bracket creep, where more of your income is taxed at higher rates, reducing your after-tax salary's purchasing power.

In a progressive tax system, tax rates increase with income. As your income rises, more of it is taxed at higher rates. Without adjustments to tax brackets for inflation, this leads to bracket creep, where your tax burden increases disproportionately to your income growth.

No, moving into a higher tax bracket does not reduce your take-home pay. Only the income above the new bracket threshold is taxed at the higher rate, while the rest is taxed at lower rates. However, bracket creep can still increase your overall tax burden.

For average income earners, bracket creep means that even if their income increases, their after-tax income may not keep pace with inflation. This results in a decrease in purchasing power over time, as more income is taxed at higher rates.

Adjusting tax brackets for inflation would reduce the government's tax revenue, which is why there may be little political will to make such changes. The extra revenue from bracket creep helps balance the budget, making it a challenging issue to address politically.

Investors and wage earners should be aware of the impact of bracket creep on their after-tax income and consider it when planning their finances. Understanding how tax brackets work and staying informed about potential tax reforms can help in making informed financial decisions.

One potential solution is to index tax brackets to inflation or wage growth, ensuring they adjust over time. This would help maintain the purchasing power of after-tax income. However, implementing such changes requires political will and may face resistance due to its impact on government revenue.