Bond's legacy of misconduct lives on

Tony Kaye

Bond's legacy of misconduct lives on

I've been waiting keenly for the start of the new Channel Nine mini-series The House of Bond.

It's a sort of morbid curiosity I guess, because the last time I saw Alan Bond face to face we parted on fairly bad terms. In fact, he kicked me out of his office.

That was about 25 years ago and I was then the West Australian Bureau Chief of the Australian Financial Review. It was a Sunday afternoon and I'd received a tip-off that receivers had just been appointed to his flagship private company Dallhold Investments.

I'd been told that Bond had been seen going into his building, so I drove down to Dallhold's then HQ on Perth's St Georges Terrace to check things out. As I arrived, the scene in front of me was chaotic. There was Bond standing in the centre of the office foyer, orchestrating a dozen or more of his employees carrying document boxes from one side to the other.

I don't know what was in those document boxes. But I do know they didn't get to the receivers, because I could hear the Bond shredding machines working overtime.

By then I'd been on Bond's case for more than two years, covering his public and private business interests. Large amounts of company money had disappeared and, as his empire crumbled, I had uncovered a network of private trusts and companies controlled by other members of the Bond family owning properties and other investment assets.

I'd estimated them to be worth at least $50 million at the time, and they were effectively untouchable because Alan Bond's name wasn't on any title. He had managed to look after his personal interests extremely well while leaving his loyal shareholders with nothing.

As I stood at the front of the foyer recording the scene, Bond spotted me standing alone. The game was up, and Bond yelled at me to get out. It didn't really matter. I had everything I needed, and another front page story followed – it was one of the sorriest tales in Australian corporate history for all the wrong reasons.

If you were among the many thousands of investors holding shares in Bond Corporation, Bell Resources or others caught in the Bond spider web, I suppose you kissed that money goodbye many years ago.

Fortunately, the laws have changed markedly from the 1990s and there's much closer scrutiny by regulators of the behaviours of executive and non-executive directors on listed and unlisted companies.

Together, the Australian Securities and Investments Commission, the Australian Securities Exchange and the Australian Competition and Consumer Commission are a formidable force in tracking company activities, breaches and monitoring corporate governance practices.

For several years I consulted to a number of the big accounting firms, in conjunction with the University of Newcastle, to produce a detailed annual survey analysing corporate governance standards across Australia. It was a rigorous exercise, recording the performance of ASX-listed companies against key global corporate governance benchmarks.

Australia's largest public companies – the top 50 – pretty much tick all the right boxes. All now have a majority of independent directors on their boards, including the chairperson. They also get top marks in relation to the independence of their audit, remuneration and nomination committees, the existence of a risk management committee, a code of conduct and a share trading policy.

That's not to say they're necessarily always good corporate citizens. They're not, and we've seen plenty of examples of poor conduct and unethical behaviour.

When you look further down the ASX field, it's more evident that the corporate governance net is being stretched. Smaller companies, with limited resources, are often falling short on key measures such as having independent directors. Mining companies, of which there are many, are perennially the worst offenders.

A company I owned shares in was delisted last year, its chairman and chief executive (the same person) banned as a director for five years by ASIC for multiple breaches of the Corporations Act. While at the helm he'd been using the company's cash flow as his personal salary, pulling out $50,000 per month in management fees. And he'd been doing the same with at least four other ASX-listed companies of which he was a director.

I won't see my money again either.

Let's face it, despite all the years that have gone by since the Bond collapse and all the regulatory steps that have been taken here to improve corporate governance standards and continuous disclosure, investors are still highly exposed. And given how easy it is to access global markets these days, the whole issue of governance and misconduct is really a global consideration for Australian investors. Corporate laws are tough in the UK, US and Europe too, but crime is still rampant.

Only recently, we've seen huge cases of misconduct involving the likes of Volkswagen and Deutsche Bank in Germany, Goldman Sachs and Wells Fargo in the US, and dozens of other high-profile corporate scandals that have resulted in huge fines and heavy share price falls. Investors have had to pay the ultimate price, yet again.

This week I noted that ASIC had ordered the former chairman of AWB Ltd, Trevor Flugge, to pay a pecuniary penalty of $50,000 and be disqualified from managing corporations for a period of five years for breaching his duties as a director. This related to his failure to inquire into the payment of around $200 million of transportation fees by AWB, which ultimately fell into the pockets of former Iraqi dictator Saddam Hussein.

Then, on Tuesday this week, law firm Maurice Blackburn, with support from litigation funding giant IMF Bentham, announced a planned class action lawsuit against retailer Woolworths over alleged Corporations Law breaches in relation to a profit warning issued in February 2015. The retailer had upgraded to its 2015 profit guidance in the previous August, but hadn't advised the market until months later that it had identified significant risks to its earnings. The company's shares subsequently dived, costing me and other shareholders dearly.

IMF Bentham has a chunk of investor class actions on its books against Australian corporates, including Spotless Group, Bellamy's Holdings, UGL and others. Maurice Blackburn also has a growing list of class actions, including against Crown Resorts, QBE, Radio Rentals, and rival law firm Slater & Gordon. The latter's list is also impressive, with pending class actions against ANZ, Commonwealth Bank, NAB and many others.

What can we, as investors, make out of this litigation? Is it just a case of law firms wanting to cash in, or is there something inherently wrong with corporate Australia?

I think there's elements of both. Litigation is certainly more prevalent these days and, in many cases, it is warranted. Corporate scandals do keep popping up, and company directors are routinely being booked by ASIC. Likewise, the ACCC has regularly launched court actions against companies for breaching competition rules and for misleading consumers.

Shareholders are still being taken advantage of too, with many directors being paid obscene salaries out of company earnings that simply don't equate with the performance of the companies they manage. Even this week, the Australian Shareholders Association criticised the board of Australia's largest construction group, CIMIC, for paying its top executives more than $1 million each in bonuses despite the deaths of several employees during the year.

I do think things have got much better for shareholders in terms of corporate governance from the days when the likes of Alan Bond could treat their investors with total disdain.

But, call me a cynic, I doubt we ever will totally stamp out corporate misconduct. It's just evident in other, more subtle ways.

I think, from an investing point of view, Warren Buffett summed things up very well in terms of company management.

“I try to buy stock in businesses that are so wonderful that an idiot can run them because, sooner or later, one will,” he once said.

It's a very good tip. I've invested in lots of great companies with excellent fundamentals over time, but some have ended up being run by idiots.

The trick is to pick good stocks that are idiot proof.

Last Week

Shane Oliver, AMP Capital

Investment markets and key developments over the past week

- Investment markets were in "risk off" mode over the last week in response to concerns about North Korea, Syria and the approaching French election. As a result Australian shares gave up most of their gains from earlier in the week and most major share markets declined whereas safe havens like gold, government bonds and the Yen rallied. Apart from safe haven demand bond yields were also pushed lower as President Trump indicated that he likes low interest rates. His comments that the US dollar was too strong also helped push the $US lower which, despite a plunging iron ore price, saw the $A remain move up. Oil strengthened.

- Geopolitics seemed to dominate over the past week with the ramifications of the US' missile strike on Syria still reverberating and tensions around North Korea steadily building. The issues around Syria are likely to settle down assuming US involvement does not escalate, but North Korea is more risky. US naval ships are moving into the area, President Trump has indicated that the US will solve the North Korean problem with or without China and North Korea has threatened nuclear retaliation and there is around this Saturday which is the anniversary of the birth of the founder of North Korea Kim Il-sung and may be an opportunity for North Korea to flex its muscles. Military conflict with North Korea would be risky given its ability to lob missiles into South Korea and Japan, potentially with nuclear warheads. But in thinking about the risks around North Korea it's useful to think in terms of three scenarios as to how it could unfold:

- No war - risks around North Korea have flared up in the past only to settle down again and the same may happen this time with diplomacy aided by China (which is focussed on achieving a peaceful solution) and Trump offering North Korea more trade.

- A brief military conflict - perhaps like the 1991 and 2003 gulf wars proved to be, albeit without a full on ground war or regime change.

- A long drawn out dirty war - eg with North Korean attacks on neighbouring countries. This may have a more negative impact on share markets and risk assets and provide a further boost to safe havens like government bonds and gold given the threat such a war would pose to Japan and a part of the world that is a strong contributor to global growth.

- At this stage it's too early to prognosticate with confidence how it will turn out, but it's hard to see the US committing ground forces so it would no doubt be aiming at just a brief conflict at worst. In terms of the impact of wars on share markets, a naive view would suggest they are universally bad, but history tells us that this is not necessarily the case. The US share market rose by 15.7 per centpa through World War Two (from Pearl Harbour in 1941) and by 8.6 per cent pa through the 1950-53 Korean conflict. While it only rose 0.6 per cent pa though the Vietnam War this reflected high and rising inflation. Shares have tended to sell off initially on the uncertainty of war with safe havens benefiting, but rally once the shooting starts and confidence builds the US will prevail. This was apparent In World War Two and in relation to the two Gulf Wars.

- Of course each conflict is different with a critical aspect in this case being the risk of North Korea using nuclear weapons. And after the share market gains of the last year global and Australian shares are a bit vulnerable to a correction and military conflict with North Korea may be a trigger (whereas going into the gulf wars shares were actually quite cheap). The bottom line though is that while conflict with North Korea will likely cause some volatility in investment markets, a long drawn out negative impact is unlikely.

- Nervousness is also building around the upcoming French presidential election with the first round on Sunday April 23rd. Polls for the first round show centrist pro-Euro Macron and far right anti-Euro Le Pen leading the race on around 23 per cent of the vote each. However, they have dropped a point or two as far left candidate Melenchon has been catching up to centre right Fillon and overtaking him to be on around 18 per cent of the vote. This has added to uncertainty around the election. If Macron and Le Pen make it through to the second round the odds of a Le Pen victory will be low as polls show Macron leading Le Pen by around 20 per cent. Risks would remain – eg a terrorist attack boosting support for Le Pen – but the chance of a Le Pen victory would be low and markets could stop worrying about France destabilising the Eurozone. However, if Melenchon edges out Macron in the first round and goes into the second round facing Le Pen the prospect of either a far left or far right victory would be taken badly by markets as both would threaten the Euro and both advocate policies that would be negative for the French economy. Similarly, Fillon making it through to the second round in a contest with Le Pen would also be a concern given that Fillon is now a weakened candidate. So worries about France and Eurozone break up risks may escalate in the week ahead, although ultimately I still see a Macron victory.

- Policy uncertainties also continue in the US with President Trump indicating that his priority is to resolve reforming Obamacare before tax reform. If successful this will free up budget funding for tax reform but it will likely also delay tax reform till either late this year or early next. That said Trump remains determined to pursue tax reform which provides some comfort. President Trump also indicated that he likes low interest rates and Fed Chair Janet Yellen reversing expectations that he would stack the Fed with hawks. He also said the $US was too strong but that he is not going to label China a currency manipulator further easing fears of a trade war with China. President Trumps "reversals" on Russia, Syria, the Fed and China clearly indicate that Trump the Pragmatist is dominating Trump the Populist.

Major global economic events and implications

- US data was mostly strong with small business optimism hanging on to the huge gains since Trump was elected and job openings, hiring and quits (people quitting their jobs for new ones) remaining strong.

- Chinese inflation data for March showed continuing low consumer price inflation and a slight easing in producer price inflation. In fact, with commodity prices losing momentum after their big bounce, producer price inflation in China (and probably everywhere else) looks like it has peaked. Meanwhile, trade data showed a pick-up in exports and slightly slower but still strong imports.

Australian economic events and implications

- In Australia, the RBA's Financial Stability Review repeated its concerns around household debt, home prices, rising investor activity in Sydney and Melbourne and new unit supply. However, it noted that household financial stress is currently contained helped by low rates and that banks are well placed to manage the challenges. The Bank also seems confident that recently announced macro prudential controls will help contain the risks and that further measures will be considered if necessary. We remain of the view that bank rate hikes, tighter lending conditions, Federal Government measures in the May budget and rising unit supply will lead to a slowing in the Sydney and Melbourne property markets.

- On the data front, March job growth surprised on the upside driven by a big gain in full time jobs. While the jobs data is notoriously volatile month to month and the unchanged unemployment rate at 5.9 per cent suggests caution in getting too excited, it seems that jobs growth is picking up a bit in Australia and this is consistent with leading labour market indicators. Meanwhile, the divergence between business confidence and conditions - which ranges from good to very good - and consumer confidence - which is a bit below average - remains. Quite clearly low wages growth and high levels of underemployment are continuing to weigh on households – which is a key argument against the RBA considering rate hikes at present. Finally, housing finance slowed a bit in February led by a welcome fall back in finance going to property investors.

Shane Oliver is head of investment strategy and chief economist at AMP Capital.

Next Week

Craig James, CommSec

Upcoming economic and financial market events

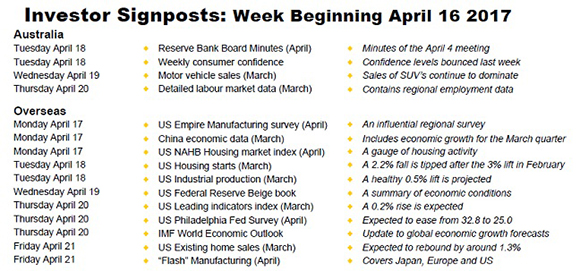

Reserve Bank Board minutes to dominate attention in a holiday-shortened week

- The domestic economic data dries up in a holiday-shortened week. In Australia the Reserve Bank will dominate the calendar and hopefully provide us with more insight on interest rates with the release of the Board minutes. In the US the focus will be on the housing sector. However investors and traders will be more interested in the Chinese economic data (Monday) and “flash” manufacturing data released across the globe (Friday).

- On Tuesday in Australia, the minutes of the April 4 Reserve Bank Board meeting are released – the meeting that decided to leave rates on hold for another month. Investors will be hoping to get a better sense of central bank thinking from the Board minutes – particularly when it comes to the near-term economic outlook. The statement following the ‘no change' decision in early April was more mixed than previous statements, with policymakers a little disappointed that the economy is largely marking time. Interestingly housing dominated the commentary and should no doubt be fleshed out more in the minutes.

- The weekly consumer sentiment reading will be released on the same day (on Tuesday). Confidence levels have fallen for the past four weeks, down by 3.8 per cent. It is pretty clear that the uncertainty surrounding the tensions in the Middle East and North Korea are weighing on confidence.

- On Wednesday, the Australian Bureau of Statistics (ABS) will recast the industry data on new car sales, converting the original data into seasonally adjusted and trend estimates. The Federal Chamber of Automotive Industries has already reported that 105,410 new cars were sold in March, up 0.9 percent on a year ago. Interestingly we may be seeing a mixed picture on consumer spending but the same cannot be said for sales of sports utility vehicles (or four-wheel drive vehicles). It is clear that demand for SUVs is the main driver of vehicle sales, scaling new heights in March to be up almost 8 per cent on a year ago. In fact SUVs outsold passenger cars for a second month.

- On Thursday the NAB quarterly business survey is released alongside the March detailed labour market statistics from the ABS. The industry make-up of employment was released last month, but Thursday's data will have regional and demographic detail on the job market.

China GDP; “Flash” manufacturing data

- Chinese and US economic data compete for top billing in the coming week. The highlight is probably Chinese economic growth data on Monday. The International Monetary Fund will also update its economic forecasts on Thursday.

- On Monday the week kicks off in China when the National Bureau of Statistics releases economic growth data alongside the usual monthly readings on retail sales, production and investment. The Chinese economy expanded at a 6.8 per cent annual pace in the December quarter. Predictably growth will ease further in coming years to reflect maturation of the economy's development.

- Also on Monday in the US, the Empire manufacturing gauge and the National Association of Home Builders (NAHB) index are both slated for release.

- On Tuesday, US industrial production and two key indicators on the housing sector will be released – housing starts and building permits. US annualised housing starts are tipped to have eased from a 1.28 million annual rate to 1.26 million in March. New building permits are expected to have edged higher by 3.6 per cent in the month. Industrial production is forecast to rise by 0.5 per cent in March.

- Also on Tuesday, China releases data on property prices for March.

- On Wednesday, the usual US weekly data on home purchase and refinancing is issued. While the US Federal Reserve releases its Beige Book - anecdotal views on how the economy is tracking across the 12 Federal Reserve districts. The report is likely to be more upbeat given the recent March rate hike.

- On Thursday in the US the usual weekly data on claims for unemployment insurance is released together with the Philadelphia Fed business index and the leading index for March. The leading indicators index is now back at levels last seen before the Global Financial Crisis and for the record is forecast to lift by a further 0.2 per cent in March.

- On Friday, existing home sales data is released and should have remained robust with annualised sales tipped to lift from a 5.48 million annual rate to 5.55 million in March.

- Also on Friday, Markit releases the “flash” readings (or early estimates) of manufacturing activity in the US, Europe and Japan.

Financial markets

- The US earnings season cranks up a notch in the coming week. And hopes are certainly upbeat for a good season of profit results. According to Bloomberg estimates, earnings amongst S&P 500 companies are expected to rise by 9.7 per cent in the March quarter and 12 per cent for the full year. And with equity market valuations at high levels, investors will be hoping that companies don't surprise with negative results.

- On Monday, 18 stocks are expected to report including IBM, Netflix, and Morgan Stanley. On Tuesday there are another 47 companies listed including Bank of America, Goldman Sachs, Intel, Johnson & Johnson, and Harley Davidson. On Wednesday earnings results are expected from 87 companies including American Express, Blackrock, EBay, Las Vega Sands, and Qualcomm. On Thursday 102 companies should issue profit results including DR Horton, KeyCorp, Mattel, Unisys, Visa, and Verizon.

Craig James is chief economist at CommSec.

Readings & Viewings

The week ended on a sour note with the Australian stock market down. We followed the US market, of course, which fell after President Donald Trump said he preferred the Federal Reserve to keep interest rates low, and that he would not label China a currency manipulator.

Oh well, just another day on the markets. But the distribution of returns in the stock market is bizarrely lopsided.

Wall Street's Charging Bull wants the Fearless Girl to get out of his way.

Pot stocks are hitting new highs. Could businesses like this be next in line to ride the high?

Speaking of supply chains and startups, Patagonia is pioneering a new way to try and find the next billion-dollar company.

US stores are closing at record rates, and Amazon is filling the gaps.

NASA and Amazon will broadcast live to any aliens out there on April 22. Pop that date in your calendar if you are an alien and reading this (and feel free to get in touch).

Online sales of second-hand clothing are growing 20x the broader retail market, and VCs are buying up in bulk.

It's a tough life being a ‘bot. Domino's Australia's DRU is reportedly working overtime compared to his friend Marble in Silicon Valley, though.

Mondelez, the company behind Cadbury, Oreo and a string of other global food brands, is looking for a new CEO.

One could term this a lot of bread. JAB Holdings is buying fast casual restaurant chain Panera Breads for $US7.5 billion including $US340 million in debt.

Now, onto scandals. An apparent secret recording of a conversation between two senior bankers at Barclays during the height of the 2008 financial crisis has raised fresh questions over the role the Bank of England played in the Libor scandal.

Fraud knows no boundaries. The US Internal Revenue Service is sending out 100,000 notification letters to student financial aid applicants who could be at risk of identity fraud.

Over in the UK, a million customers of payday loan firm Wonga are being warned that their personal data may have been stolen.

Meanwhile, Facebook and Google reveal how they plan to fight fake news.

Rare new £1 coins could make a big profit online.

A former Snapchat employee has called bull on the company's growth. Naturally, Snap has snapped back.

Instead of selling it, you could just fix it. These Mr Fix It's have created a $21 million business that shows you how to fix (almost) everything. It's probably Apple's worst nightmare.

Do the words mumpreneur and #girlboss send shivers down your spine? It could be the hashtag speak; but anyway, this female journalist is on your side.

Before you decide which movie to watch this long weekend, scan this article by a data scientist.

A Greenpeace investigation has concluded that Coca-Cola sells nearly 3,500 single-use bottles every second, and that's bad for our environment.