Battered and bruised: A new BHP emerges

Summary: We have never seen a BHP with such a pro-shareholder distribution agenda. It has become very much akin to a toll road enterprise or a property trust and is distributing all the cash it generates and sometimes may borrow to pay dividends. But where returns are exceptionally high, it will invest rather than give money back to shareholders. |

Key take-out: We need to think about BHP not as a growth company but as an income stock which makes us uncomfortable – given the money it has to distribute will fluctuate with commodity prices, it certainly is not a secure income stock so that's why the market is giving it a high yield. |

Key beneficiaries: General investors. Category: Mining stocks. |

The current fall in the market – the ASX closed at 5,101.5 today – is perhaps more serious than the earlier falls we saw in recent weeks.

But for most small investors it is all about dividends which was brought home to me in the last few days.

It was a school occasion this week and as I entered the concert hall a long serving science teacher came racing up me to challenge myself and Alan Kohler over BHP Billiton.

The science teacher's argument was that mines had a limited life and therefore as soon as they were up and running the cash they produced should be distributed to the owners and not frittered away on some other project.

In other words the message from the science teacher was: “I am a BHP shareholder and I want dividends because I invested in a mining company.” It so happened that a week earlier I was yarning with BHP chief financial officer Peter Beaven and discovered that stripped of all the complexities, BHP under CEO Andrew Mackenzie has pretty much embraced the same view as our science teacher.

And it is totally different to anything we have seen before from The Big Australian.

Take out all the paraphernalia that comes with every profit result from a large company and you discover that the core of BHP is its cash generation statement. BHP has become very much akin to a toll road enterprise like Transurban or a property trust and is distributing all the cash it generates and sometimes it may borrow to pay dividends.

So let's translate that into raw BHP figures. The company in the year to June 30 produced a free cash flow of $US6.3 billion but it would have been $US17.4bn but for the $US11bn the company spent on capital expenditure and exploration.

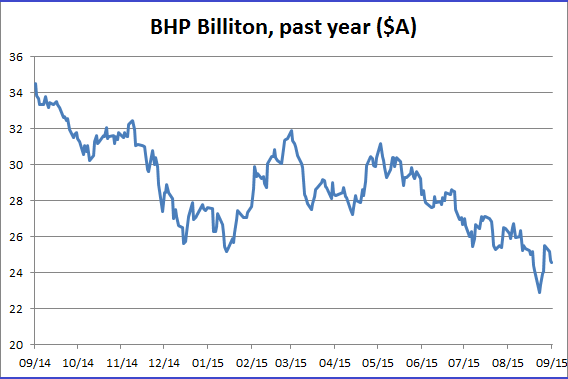

Almost all the $6.3bn free cash flow was distributed as a dividend and as a result BHP shares are yielding more than seven per cent.

Now in the current year the company expects to cut its capital expenditure and exploration by $US2.5bn to $US8.5bn. That means that if its trading stayed the same as last year (unlikely) then the group would have $US8.8bn to distribute to shareholders. Given the decline in the prices BHP receives for its iron ore, coal, copper and other products BHP looks certain to see falling trading profits so it might be stretched to produce a free cash flow of $US6.3bn even though its capital expenditure is set to be reduced.

The company slashed its costs by $US4bn in 2014-15 and expects further big falls in costs in the current year which will also assist it in getting free cash flow back up to US$6.3bn despite the price falls.

If we have a substantial fall in commodity prices from today's level, then the reduction in capital expenditure and costs will not be sufficient. But if the company goes close it will almost certainly borrow to pay dividends because it believes its gearing is conservative.

Source: Bloomberg, Eureka Report

So why does BHP need to spend $US8.5bn in the current year on capital works albeit reduced from 2014-15? About $US2-3bn is necessary simply to keep its mines going and it is really better classified as maintenance. Most of the remainder is bolt-on capital expenditure where the group is removing production bottlenecks.

Beaven says that in many of these de-bottlenecking operations the company is receiving a return of about 40 per cent on the money it is outlaying. And none of the projects returns below 20 per cent. So BHP is saying that where returns are exceptionally high it will invest rather than give money back to shareholders. That means that big long-term projects like Olympic Dam and Canadian potash will need to be extremely profitable to attract today's BHP into committing major funds. In the case of both projects, a limited amount of money needs to be spent to meet governmental laws and to make the most of current operations.

Clearly as long as BHP maintains its current attitudes new projects are going to be very rewarding and that will require much higher product prices. Beaven says that when assessing any major new capital expenditure investment, the company will at all times test the proposed capital expenditure outlays against the returns that come from buying back shares.

In other words if the market does not recognise future BHP returns the company will buy back shares rather than start new projects.

We have never seen a BHP with such a pro-shareholder distribution agenda. The company itself is mildly bullish on the long-term outlook of some of its products. It believes the demand for copper will exceed supply later in the decade and it also believes that over time the current low oil price will reduce American production and other high-cost projects.

When it comes to iron ore the biggest new increase in production will come from Brazil's Vale. Vale has to decide whether to stop its high-cost production in exchange for the low-cost output or simply flood the market which will see the price fall quite sharply.

BHP does not think Vale will flood the market but nobody can be sure. So we now need to think about BHP not as a growth company but as an income stock which makes us uncomfortable.

But it seems this is exactly the attitude the company has adopted. Given the money it has to distribute will fluctuate year on year with commodity prices, it certainly is not a secure income stock so that is why the market is giving it a high yield.

Some of the reports we are getting out of China indicate that it looks like being fairly bumpy during the next few years as the country moves away from exports and high resource investment to consumer goods and services. I suspect if the Chinese economy falls too sharply China will give its infrastructure another boost because the country can't afford major employment disruptions.

The problem China has is that in rescuing its economy from the global financial crisis it created too much unsustainable debt. That makes the transformation of the economy difficult. The stock market now understands this and is adjusting values at a time when the US economy is going well. But a troubled China will affect US profits.

In Australia we are in the front line so our share market is being hit. Meanwhile welcome to the new BHP.