Avoiding the danger zone through active portfolio management

Summary: While a long-term approach to investing is admirable, a set-and-forget portfolio mentality can be dangerous. |

Key take-out: Getting the correct asset allocation is very important for ensuring that you get the best return for the risks you are taking with your investments. |

Key beneficiaries: General investors. Category: Strategy. |

A high percentage of Australian self-managed investors are dicing with danger, simply because they are putting their portfolios on cruise control rather than actively managing them.

Without a proper investment strategy, and using traditional do-it-yourself approaches, many investors are overweight in different asset classes and underweight in others, and are missing out on opportunities to minimise risk and achieve higher investment returns over time.

Below are the consequences of poor portfolio management, and some of the steps and strategies that can be taken to take more control and improve your overall investment portfolio and wealth-creation strategy.

Lack of diversification

Probably the biggest single danger for investors with a set-and-forget portfolio mentality is the risk of over-exposure to a specific asset class.

Alarmingly, a high percentage of Australians managing their own wealth would not pass a financial health test.

Research just completed by InvestSMART, covering almost 25,000 investment portfolios and around $15 billion in assets, shows the majority of Australian investors are heavily exposed to domestic equities and residential property, but are underweight in international equities and fixed interest.

This trend is most evident at the lower end of the investment spectrum, covering investment holdings of up to $50,000, where investors on average have around 55 per cent of their capital tied to direct shareholdings in Australian companies. A further 37 per cent is held in managed funds, and the remainder mostly tied to cash in the form of term deposits.

Those with larger portfolios, ranging from $250,000 up to $10 million, have close to 40 per cent of their assets tied to domestic stocks and about 35 per cent in direct property.

A 2000 study by Yale School of Management emeritus professor Roger Ibbotson, Does Asset Allocation Policy Explain 40, 90, or 100 per cent of Performance?, concluded that “asset allocation explained virtually 100 per cent of the level of fund returns”.

Ibbotson examined the 10-year return of 94 US balanced mutual funds versus the corresponding indexed returns and, after properly adjusting for the cost of running index funds, found that the actual returns of these funds failed to beat index returns.

Having a high exposure to a particular asset class is fine, as long as it matches one's investment goals and time horizon.

Keeping pace with changing conditions

Investment markets are ever-changing and, at any particular point in time, certain investment assets will achieve strong returns while others will languish. So, what may have been a “right” strategy before could be wrong now.

For example, not all that long ago a global boom in commodities prices fed by strong demand meant Australia's resources sector was the place to be for capital growth. Similarly, investors seeking high yields flocked to the banking sector, in the process pushing up bank stocks to record levels. Yet volatile global economic and financial conditions have seen both of those sectors, and many of the stocks within them, lose substantial ground.

By contrast, due to other circumstances and events, demand for technology and healthcare stocks has brought about some spectacular returns. In Australia, returns also have been particularly good from listed property trusts, linked to the strong real returns being generated from the residential and commercial property sectors.

But even investors who make the correct choice when they buy in, investing into the growth sectors of the day, need to be attuned to changing market conditions and their portfolio structure, and need to be ready to take decisive action to reduce, or exit, their exposures to underperforming assets.

Setting your investment goals

Fundamentally, every individual's investment goal is different, but a lot of one's decision-making process is governed by time horizon and risk profile.

Time horizons can broadly be broken down as below, with a shorter time horizon generally warranting a more conservative approach.

InvestSMART's Portfolio Manager calculator recommends the most appropriate asset allocations based on an individual's investment time horizon. A shorter time horizon will have a lower exposure to Australian equities and a higher allocation to fixed interest, while longer time horizons of 10 years or more will warrant higher exposures to both Australian and international shares.

Chart 1. Suggested asset allocation: Conservative vs high growth

Source: InvestSMART Group

Taking a financial health test

In the same way as one should get a physical health check from time to time, the best way to get a financial reality check is to test your investment holdings and allocations.

Entering all your assets (and liabilities) – including shares, super, managed funds, property and cash – will present a clear picture of your overall financial health and net worth.

Doing so will quickly reveal whether you are too heavily weighted to certain shares or sectors or to different asset classes, and underweight in others, based on the type of investor you are and your investments time horizon.

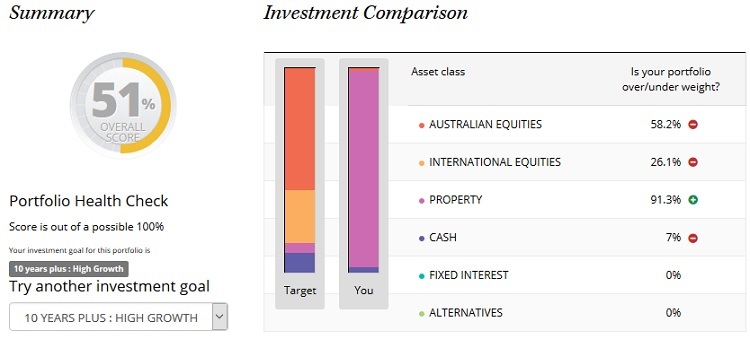

A financial check will give you a Diversification Score, which indicates how closely the allocation of assets within your portfolio is aligned to the target allocation for your chosen risk appetite.

Getting the correct asset allocation is very important for ensuring that you get the best return for the risks you are taking with your investments.

Improving your portfolio

For investors with a lower-than-recommended Allocation Exposure Score, the most prudent course of action is to rebalance one's asset allocation to improve diversification, reduce risk and improve returns.

A good way of doing this is to simulate changes to your current investments and/or add new investments to see how they could affect your overall portfolio's diversification.

But before leaping into any investments, it's vital to undertake comprehensive research. This is an area where many investors fall short, and often either overpay or fail to take into account the underlying dynamics of either the broader market, a sector and, when buying shares, those factors impacting a specific company.

In terms of shares, the level of information available to investors these days is both extensive and readily accessible.

For example, InvestSMART's Portfolio Manager enables investors to quickly tap into Stock Recommendations, a company's expected Price Range, and all written Analysis in order to make informed investment decisions.

Users can also create Alerts to monitor ASX announcements on specific companies, and build Watch Lists containing companies of potential investment interest.

In essence, investors have all the information they need right at their fingertips these days, and can access it from anywhere, at any time.

On InvestSMART, this includes information such as a company's:

- Business and Share Price Risk;

- Full Company Financials;

- ASX Announcements;

- Dividends data;

- Broker Consensus data; and

- Changes in Directors' Interests, to track the buying and selling activity of a company's directors.

Reactive and active go hand in hand

Various tax benefits in Australia provide reasons to hold direct equities and other investments. However, diversification across asset classes is important in minimising risk and potentially improving returns.

The key to successful portfolio management is having, and sticking to, defined investment objectives. Emotion should never come into play, but when circumstances dictate active investors should be ready, and prepared, to respond.

That could mean selling out of a company that has become overvalued, and using the proceeds to reinvest into another stock or asset where there is better return potential. Conversely, it could mean selling a stock that has fallen to minimise losses.

It's all about being in control, using the vast array of information available to build and maintain a well-balanced portfolio of assets and to maximise investment returns over the longer term.

To gauge the overall financial health of your portfolio, it's important to get a regular check-up. Click through to InvestSMART's Portfolio Manager to enter your portfolio details and see whether your investment allocations are well balanced or need some adjusting.