Australia's rates reality is lower for longer

Summary: We have an economy that is creating jobs, but not high-quality or high-wage jobs. Meanwhile, low inflation looks like it has some way to run. |

Key take-out: The data on employment and inflation suggests that Australia is a number of years away from experiencing higher interest rates. |

Key beneficiaries: General investors. Category: Economy, investment strategy. |

The Reserve Bank of Australia appears almost certain to leave interest rates unchanged when it meets on Tuesday. However, recent data on employment and inflation present a compelling case in favour of further cuts next year.

Labour market

The Australian Bureau of Statistics (ABS) released its Labour Force Survey last week and it was a disappointing result for investors, with employment growth falling well short of market expectations.

Employment growth has slowed significantly since the beginning of the year. The Australian economy created just 3800 jobs in September on a trend basis and is on track to grow by 90,000-100,000 people in 2016 (compared with 298,800 people last year).

The chief concern is full-time employment. Full-time employment fell by 7900 people in September – the ninth consecutive monthly decline – which was more than offset by a rise in part-time employment.

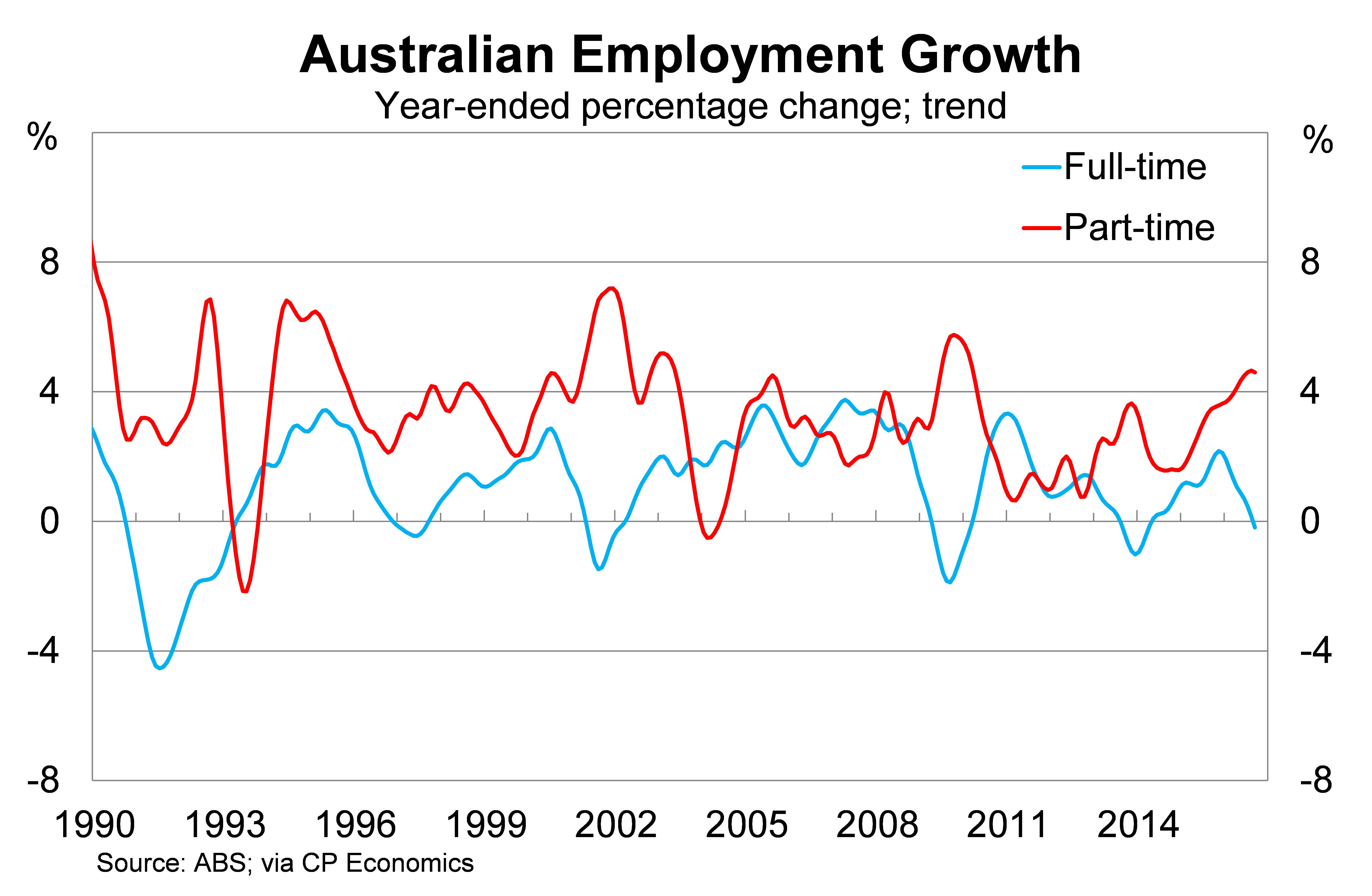

The graph below shows annual growth for full-time and part-time employment. Full-time employment is down slightly over the past year, while part-time employment is growing at more than 4 per cent.

Full-time employment growth is typically a pro-cyclical indicator, meaning that it does well when economic conditions are strong, whereas part-time employment displays some counter-cyclical tendencies. The current zero to 4 per cent divide has historically been a sign of economic hardship. It occurred during our last recession a quarter-century ago, the aftermath of the dot-com bubble and the global financial crisis.

Now I'm not predicting a recession – the mining export boom, which admittedly creates few jobs, will ensure that economic growth remains positive – but it does indicate that many Australian corporates remain cautious while others continue to struggle.

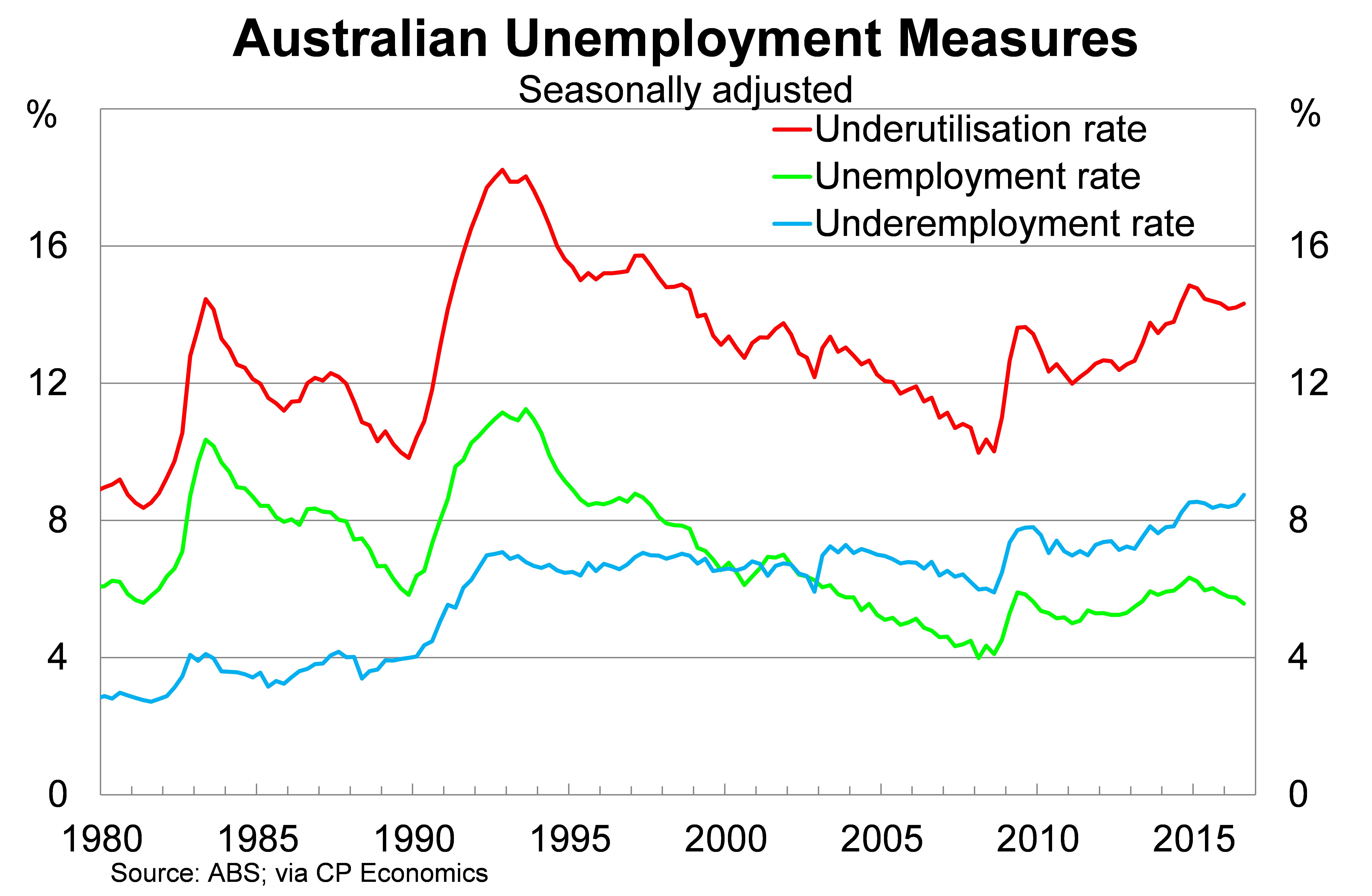

There remains significant spare capacity across Australia's labour market. Hundreds of thousands remain unemployed and many more are underemployed and would, if they could, work more hours.

According to the ABS, the unemployment rate currently sits at 5.6 per cent but the underemployment rate sits at 8.7 per cent. That gives us a total labour under-utilisation rate (unemployment plus underemployment) of 14.3 per cent.

We currently have an economy that is creating jobs but isn't creating the high-quality or high-wage jobs that we have become accustomed to. People have been forced to take on part-time or casual roles because the alternative is unemployment.

None of this is particularly surprising to me. Non-mining investment remains incredibly weak and investment is often the trigger for expansion both physically and in terms of staffing levels. A corporate sector that foregoes investment is a corporate sector that isn't looking to expand or innovate or disrupt their market.

Inflation

A couple of months ago I explained the apparent divergence between what was, at the time, solid employment growth and subdued inflation. That picture has cleared up in recent months as employment growth has eased to a level that is more consistent with a low inflation environment.

The ABS released new data on consumer prices today (Wednesday) and little has changed on the inflation front.

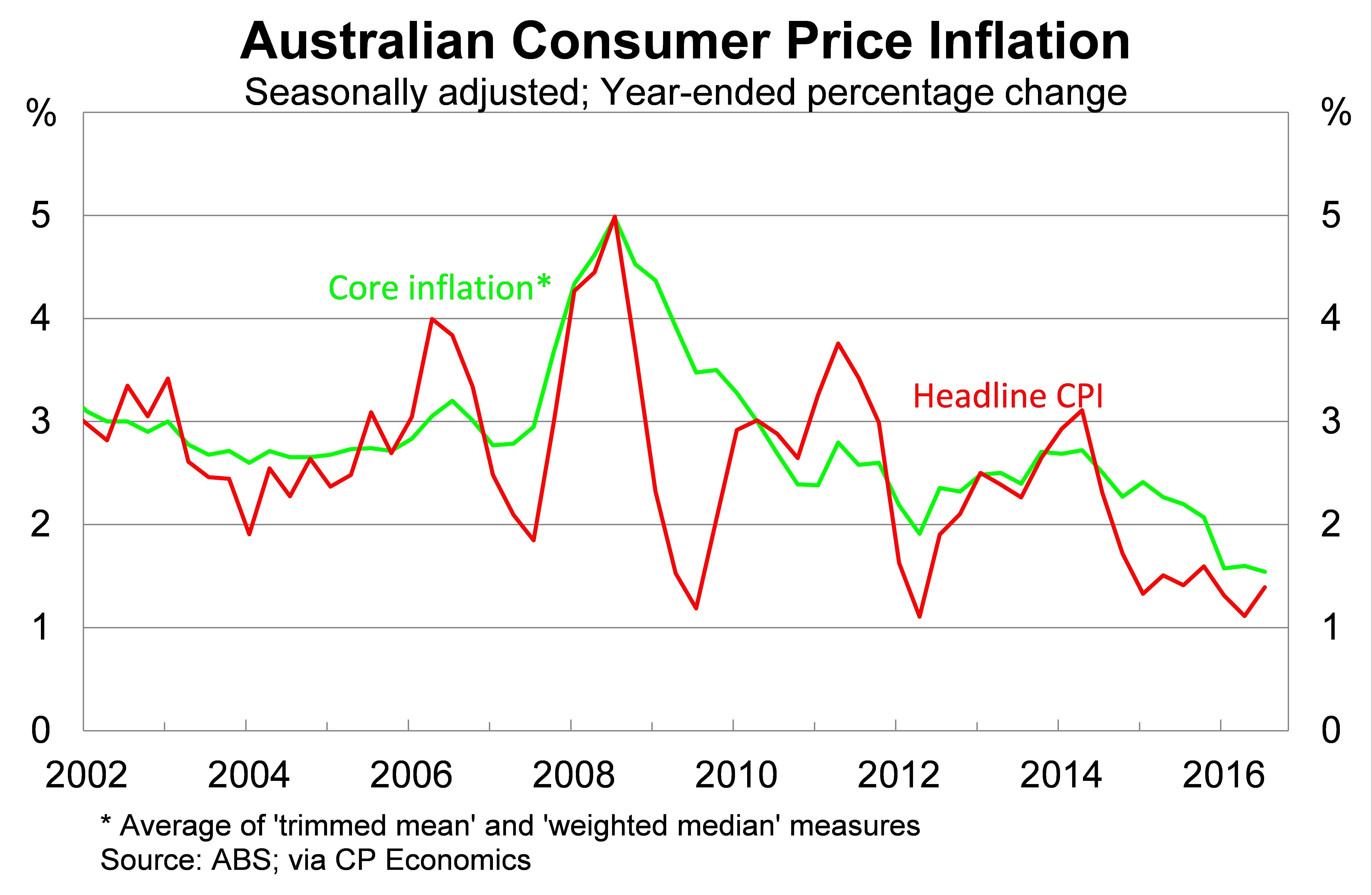

Headline inflation rose by 0.4 per cent in the September quarter, on a seasonally-adjusted basis, to be 1.4 per cent higher over the year. This result follows a relatively soft first-half of the year, which saw prices rise at an annualised pace of just 1.3 per cent.

The measure that the RBA pays the most attention to is core inflation. This measure removes the impact of volatile items and provides a better guide of underlying inflation. By focusing on this measure the RBA avoids overreacting to a big change in, say, oil or fruit prices.

The ABS publishes two measures of core inflation, a ‘trimmed mean' and a ‘weighted median' measure. Both measures take a different approach to removing volatile items but typically provide a similar assessment of inflation. As a result, it is quite common to take a simple average of these two measures.

Core inflation rose by 0.3 per cent in the September quarter, following a soft start to the year, to be 1.5 per cent higher over the year. Core inflation currently sits at its lowest level in over three decades; creating quite the headache for the RBA and monetary policy.

What does Philip Lowe think?

RBA governor Philip Lowe gave a speech last week where he provided some insight into the current low inflation environment.

The first point is that low inflation is a global phenomenon and Australia is one of the last advanced economies to suffer. The initial cause varies – for most it is a product of elevated unemployment following the global financial crisis – but in our case low inflation is a product of falling commodity prices. This led to a decline in national income growth that first hit corporate incomes, then wages and finally inflation.

Lowe cites three main reasons for the global low inflation environment.

- “The first … explanation is that the low inflation reflects economic slack in the global competition,” he said. “Economic growth has generally disappointed since the global financial crisis, weighed down by an overhang of debt.”

As I showed in an earlier graph, there remains a high level of labour under-utilisation in Australia. More people competing for job vacancies means that corporates can afford to be a little frugal and drive a tougher bargain. The end result is weaker wage growth that puts downward pressure on consumer spending and inflation.

- “The second factor is a self-reinforcing dynamic originating from the decline in headline inflation caused by the fall in commodity prices, including oil prices,” Lowe said.

According to Lowe, many employees have agreed to smaller wage increases than they have in the past because existing inflation is low. This creates a feedback loop whereby low inflation creates persistently low inflation. This refers to what economists call ‘inflation expectations' and the biggest concern for Lowe and the RBA is that households and corporates will begin to expect low inflation and price that into wage negotiations. If that happens the task of returning inflation towards target becomes more difficult.

- “The third factor is that there has been a shift in the perceived pricing power of many workers and businesses,” he said.

Lowe believes that this goes above and beyond the rise in the unemployment and underemployment rates. Globalisation, for example, has reduced the bargaining power of many employees and that has led to weaker wage gains.

For decades, workers in the manufacturing sectors across most advanced economies have felt pressure from globalisation and international trade. These days many workers in the service sector are experiencing a similar phenomenon due to improved technology that has created greater competition and lower prices.

From a market perspective, the main benefit of a low inflation environment has been historically low interest rates. Low interest rates will persist until such a time as inflation returns towards more normal levels.

The main downside is that low interest rates reduce the number of high-quality assets that offer a sufficient return. The end result has been a global ‘search for yield' that has arguably led to risk-taking that wouldn't otherwise have occurred. Risk has arguably been under-priced across many asset markets.

The data on employment and inflation suggests that Australia is a number of years away from experiencing higher interest rates. Core inflation is likely to remain below the RBA's 2-3 per cent target band until at least 2018. If this is correct then markets appear to be under-pricing the possibility of further rate cuts next year.

There will be less pressure on the RBA to cut if the Federal Reserve hikes US rates by the end of the year. Nevertheless, it is clear that the processes that led to low inflation in Australia and abroad still have some way to run and the RBA may be forced to bring the cash rate in line with monetary policy in other advanced economies.