A reality check for the current construction 'boom'

Building approvals rebounded in October but the indicator is likely to moderate further in the coming months. Nevertheless, residential construction should head higher, supporting GDP growth, over the next 12 to 18 months.

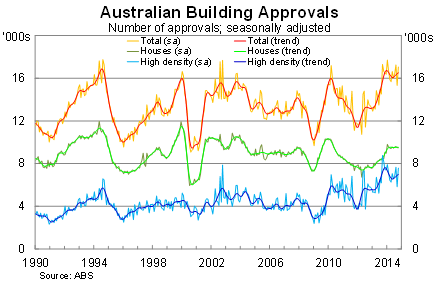

Building approvals rose by 11.4 per cent in October, beating market expectations, to be 2.5 per cent higher over the year. At first glance that seems like a pretty good result but it largely offsets last month's 11 per cent decline. Furthermore, the pick-up was narrowly based -- concentrated in Victorian apartments -- which suggest that approvals will ease again over the next few months.

On a trend basis, approvals peaked in December last year but have picked up recently following considerable volatility. Given that, even the trend estimates will fluctuate somewhat over the next few months and it may be difficult to get a solid read on the fundamentals until early next year.

Approvals for housing -- which have historically been less volatile -- have eased somewhat in recent months but overall activity has been relatively stable. The recent volatility has been concentrated within the higher-density apartment sector, which rose by around 30 per cent in October (after falling by almost 25 per cent in the previous month) to be 7.4 per cent higher over the year.

Much of that was driven by Victoria, where approvals for apartments rose by a staggering 67 per cent in October. To put this into perspective, that rise accounted for around two-thirds of all growth in national building approvals for October.

In all likelihood this reflects a few large projects that were granted approval during October and the number of apartment approvals for Victoria will fall sharply in November. On that basis, the market will almost certainly price in a significant fall for next month's release.

Growth in the other states was more moderate. In New South Wales, the number of approvals rose modestly on a trend basis -- the first increase this year. Both Queensland and Western Australia were up slightly, while approvals declined moderately in South Australia.

But we should also remember that this data is for approvals and not completions or construction and some projects may not go ahead. Construction in Western Australia and Queensland might be the most at risk, given the current state of the resource sector, but increasingly it appears as though there may be an overbuild in Victoria.

We shouldn't understate the risk that some of these projects don't go ahead, particularly if prices begin to ease over the next six months. Given the high level of vacancies in Melbourne's inner city, there's good reason to be pessimistic about the outlook for Melbourne apartment prices.

Recent research by Prosper Australia, for example, found that over a quarter of properties in the Docklands sit idle. Furthermore, 12.7 per cent of properties in Carlton South and 11 per cent of properties in West Melbourne are vacant.

Those numbers, particularly in the Docklands, could surge further over the next couple of years as more supply comes online and is purchased by investors who are interested in capital gains and not particularly fussed by earning low rental yields.

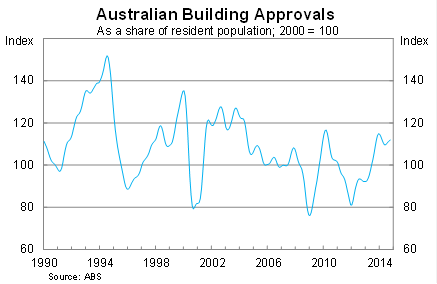

Finally, it is also worth putting the current construction boom in some context. While approvals have been and remain elevated, the upswing has not been as significant as during previous construction booms.

The 2010-11 ‘boom' -- during which approvals tracked awfully similar to current trends -- saw residential investment rise only modestly as a share of GDP. This episode should last longer -- mostly due to the high number of apartment projects -- but the boom is unlikely to be as pronounced as earlier upswings during the mid-1990s and early 2000s.

Nevertheless, the boom still has some way to run and residential investment is likely to peak towards the end of next year or even early 2016. But it's important to remember that residential investment accounts for only 3.2 per cent of real GDP and, boom or no boom, is unlikely to offset much of the drag created when mining investment collapses.