A deflationary trigger for the ECB

Currency markets have their eyes on Europe this week, with both the Bank of England and the European Central Bank due to meet. Attention will be keenly focused on the accompanying central bank policy announcements.

UK likely to stick with policy stance

Inflation in the UK remains soft, wage growth is minimal and greater European growth is stagnating. Because of this, the Bank of England is expected to maintain its current policy stance.

The expectations surrounding a Bank of England rate hike have instead been extended, with investors now looking to Quarter 3 2015 as the likely point the Monetary Policy Committee will increase interest rates. The outward revision has been the primary driver in the sterling's downward correction over the past two months.

Europe inflation drops

Deflation is the primary concern facing the ECB. Eurozone inflation fell back to five-year lows on Friday, writing in a 0.3 per cent increase in prices through November. Markets are looking for signals the central bank will look to implement further quantitative easing and step up the purchase of government bonds.

The European Central Bank is also expected to leave rates on hold this week, with the primary focus on President Mario Draghi and the accompanying rate statement.

Investors currently expect an increase to the current pace of easing in the 1st quarter of 2015, with markets seeking firmer guidance from the ECB on Thursday. An amplified dovish stance could see support broken at 1.2400.

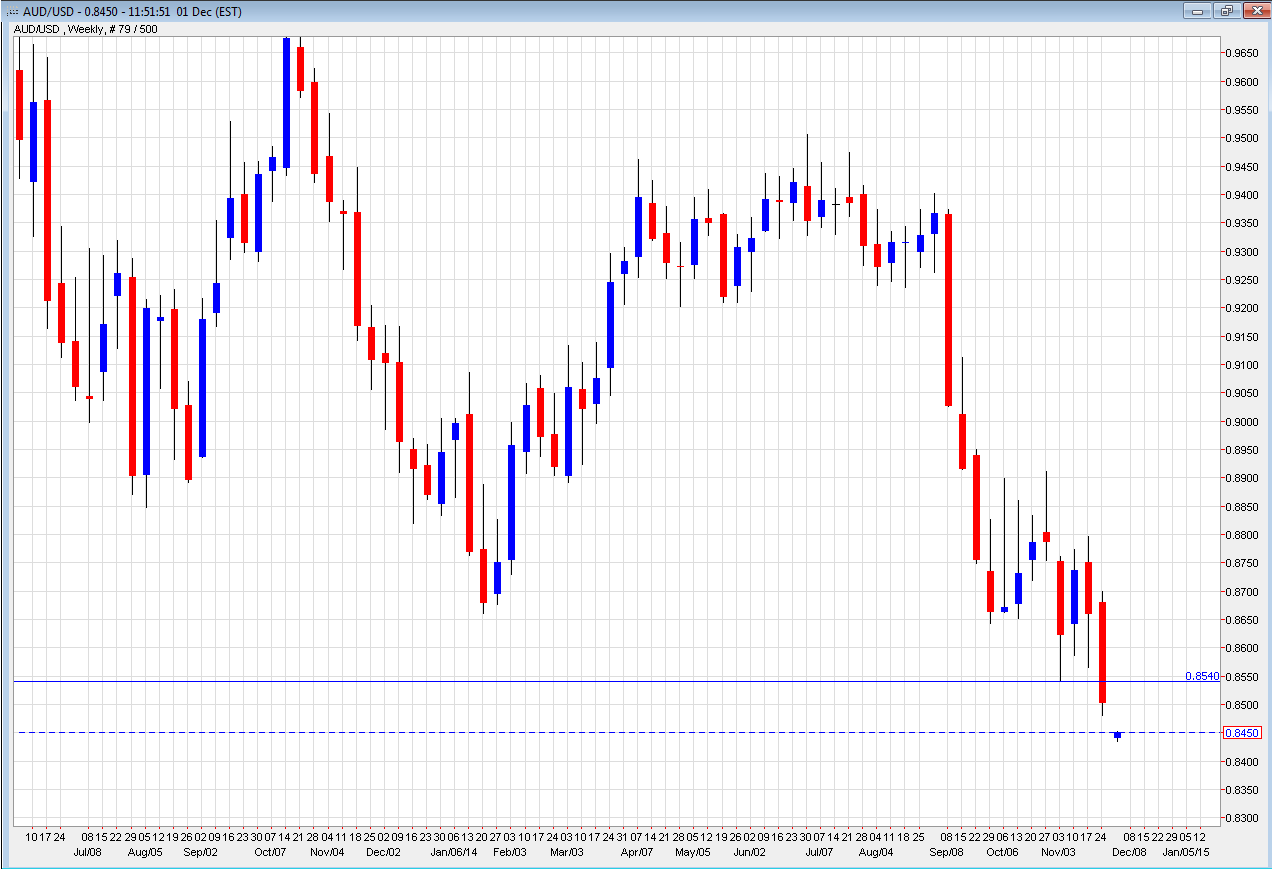

Gloom for the Aussie

The Australian dollar touched four-year lows last week and was the worst performer across major currencies. Despite a quiet domestic macroeconomic calendar, increasing volatility, a deteriorating yield advantage, stagnating global growth and falling commodity prices led by Iron Ore forced an Australian dollar sell off, breaking support levels at 0.854.

The question is: where to from here? We have a busy week ahead headlined by the RBA rate announcement, 3rd quarter GDP, retail sales and trade balance reports.

We expect the Reserve Bank will stand by its neutral policy stance preferring to maintain the advantage of a rate cut as a stimulatory tool moving into the new year. Focus subsequently shifts to the accompanying rate statement. Deputy Governor Philip Lowe last week highlighted the central bank's tendency to jawbone the currency lower, reiterating the need for further depreciation if balanced growth within the broader economy is to be maintained.

Markets will eye quarter GDP on Wednesday, with retail sales and trade balance on Thursday. Offshore stimuli in form of US non-farm payrolls will drive direction into the weekly close.

Should local data fail to meet market expectations and US employment reports add further support to the overall recovery, we could see the Aussie move closer to 0.8320 -- a level last seen in July 2010 as new levels of support and resistance are established.

Matt Richardson is Corporate Foreign Exchange Dealer at OzForex, a global supplier of online international payment services and a key provider of Forex news. OzForex Group Limited is a publicly listed entity with shares traded on the Australian Securities Exchange under the code "OFX".