Getting a seat on the China bus

- {{x.value}}

{{ twilioFailed ? 'SMS Code Failed to Send…' : 'Enter verification code' }}

{{ completedStep1 ? 'Authentication & Security' : content.trialHeading.replace('{0}', user.FirstName) }}

{{ content.upgradeHeading.replace('{0}', user.FirstName) }}

The email address you entered is registered with InvestSMART

Please login to continue

We have sent you an email with the details of your registration.

Looks you are already a member. Please enter your password to proceed

{{ upgradeCTAText }}

Updating information

Please wait ...

Your membership to InvestSMART Group recently failed to renew.

Please make sure your payment details are up to date to continue your membership.

Having trouble renewing?

Please contact Member Services on support@investsmart.com.au or 1300 880 160

You've recently updated your payment details.

It may take a few minutes to update your subscription details, during this time you will not be able to view locked content.

If you are still having trouble viewing content after 10 minutes, try logging out of your account and logging back in.

Still having trouble viewing content?

Please contact Member Services on support@investsmart.com.au or 1300 880 160

Please click on the ACTIVATE button to activate your Intelligent Investor 15-day free trial

Please click on the ACTIVATE button to finalise your membership

Unsuccessful registration

Registration for this event is available only to Eureka Report members. View our membership page for more information.

Registration for this event is available only to Intelligent Investor members. View our membership page for more information.

- You are already registered for this event.

- This event is already full.

- Please select a quantity for at least one ticket.

- {{ i }}

Forgotten password

Please enter your email address below to request a new password

- Indepth analysis of ASX listed shares

- BUY, Hold and Sell Recommendations

- Ideas Lab

- Special Reports

- Alan Kohler’s Weekend Briefing

- Interviews with CEO’s & top influencers

- Money Cafe and Talking Finance

- Super Advice and Q&A with Ask Alan

It's a mere 265 kilometres from Colombo on Sri Lanka's west coast to the east coast port of Trincomalee. In the mid-1990s the bus trip could take a day. The suicidal drivers and meteor-sized potholes were bad enough, but it was the army roadblocks that got you in the end.

The country was in the midst of a civil war and ‘Trinco' was a base of the Tamil Tigers. By the time the fifth roadblock came into view, overcome by sweat and tedium, I was ready to pay anything for a fresh t-shirt and a beer.

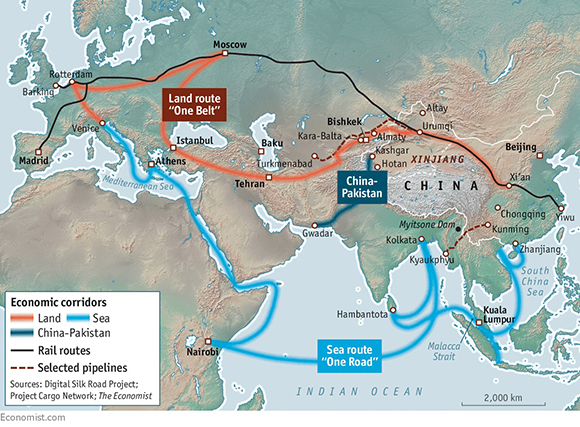

The memory returned this week whilst reading the media's paranoid-tinged coverage of China's One Belt, One Road (OBOR) initiative. The program is new to us but not to Sri Lanka or other countries in the region, many of which have been beneficiaries of massive Chinese investment for almost a decade.

During the 30-year Sri Lankan civil war, defence spending went as high as 6 per cent of GDP (the equivalent Australian figure is 2 per cent). Seemingly not much, although this research paper says it represented a near-100-fold increase in per capita defence expenditure, from $US0.89 in 1975 to $US87.55 in 2013.

That figure gives the lie to the notion of a “peace dividend” – GDP kept growing throughout the war. In the words of the paper's authors, there was “a unidirectional causality from defence spending to economic growth.” Yes folks, war can be good for business. When China moved in, much to India's chagrin, the pace of change accelerated. Three years after the war's end in 2012, Sri Lanka's GDP growth hit 9 per cent.

China's housesitting began not in Trinco, where colonial powers have traditionally put their feet up, but Hambantota in the island's south. The town now hosts a $US1.4bn deep-sea port, an international airport, multi-lane highways and a cricket stadium, many of which remain under-used (this Forbes story covers the white elephant airport's tracks).

That might not worry China, or former president Mahinda Rajapakse, a man not short of self-regard. Born in the town, many of its glittering trinkets bear his name. As The Economist map below shows, Hambantota is a port of strategic significance. About 80 per cent of China's oil moves through the Malacca Strait. Should the US ever choose to block it, China's oil supply from the Middle East can be routed to Kunming via the pipeline that begins at Kyaukphyu, perhaps with a meal stop at Hambantota to enjoy some idli and string hoppers – two of the world's great breakfasts in my view.

Call it serendipity, but the Chinese play a long game, an entwining of the commercial and the strategic over timeframes that Western politicians can't hope to comprehend because, you know, elections. Then there's the money. OBOR encompasses 75 overseas economic and trade cooperation zones in 35 countries, plus a $US1.3 trillion investment in projects already underway, with more to come.

US policymakers might recognise the template from the Marshall Plan, a $US13bn investment (in 1948 money) in the rebuilding of Europe, which created goodwill and a post-war international market for US consumer goods, plus the rationale to contain the USSR with US airbases dotted across the continent. The Marshall Plan laid the foundation for an incredible period of post-war economic growth.

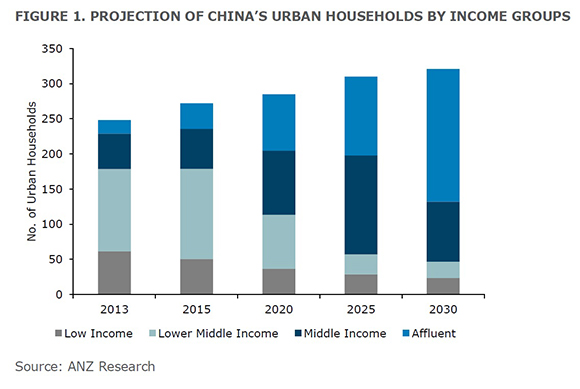

Will OBOR do likewise? Perhaps. China is a huge country with growing economic wealth and power. By 2030, ANZ Research indicates that most Chinese will be affluent, with disposable incomes in urban areas averaging $US30,000 a year in purchasing power parity terms, three times the current level.

The country is also moving up the value chain, as it must, building a high-speed rail for the Indonesians using finance from the China Development Bank. It also has burgeoning hi-tech sector that includes biotech, aircraft and huge enterprises like Tencent and Alibaba.

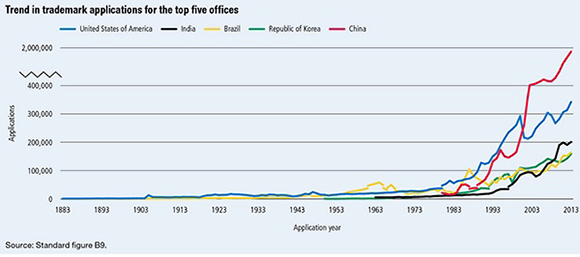

Source: World Intellectual Property Organization

Chinese companies, despite a well-known disregard for intellectual property rights, are also lodging trademarks, patent applications and industrial designs in unprecedented numbers (see above). Why not see poorer neighbours as potential new markets, and help them to get richer so they can buy your stuff? It's not as if this hasn't be tried before.

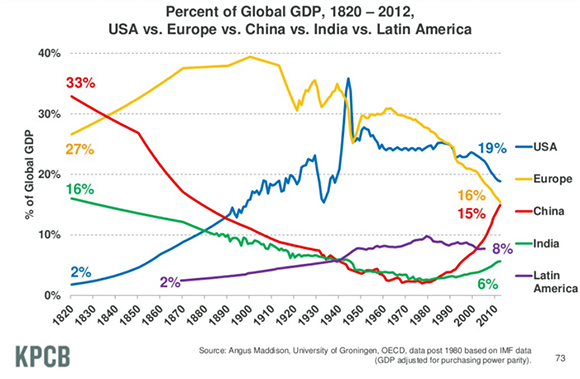

These factors are already helping China snare a growing share of global GDP, a trend that is likely to continue. One of the interesting things about this isn't just the recent growth but also the long term historical trend. Two hundred years ago China was a dominant force in global trade. We might see growing Chinese influence as something new but many Chinese see it as a rightful return of influence and muscle.

Why am I telling you this? Well, it's a fascinating turn in geopolitical power, not a passing of the baton but, in the way of these things, a gradual taking of it. As the US retreats from the world China is pushing into it.

Already, this has had profound implications for the region and Australia's economy. But this is only the beginning. For one, I expect to see more media coverage of the potential “opportunities” this shift will bring to Australian investors. There will be more wave-riding stocks like A2 Milk and Bellamy's, almost all of which will dump investors into a deep water port of their own making.

As Intelligent Investor's research director James Carlisle said a few years back in response to a member question, “Rather than focusing on growing markets, focus on companies that produce products that add value in a sustainable way and that have competitive advantages. If a company ticks those boxes it's likely to do well, whether it's selling its wares to China, Chile or Chad.”

This is a point often lost on the theme-loving funds management industry, which is undergoing a structural shift of its own. A few years ago, an ‘adviser' from MLC drove 180km to offer advice on my wife's superannuation fund. The sum wasn't huge and I couldn't understand his commitment, until I saw the 4 per cent management fee on her statement.

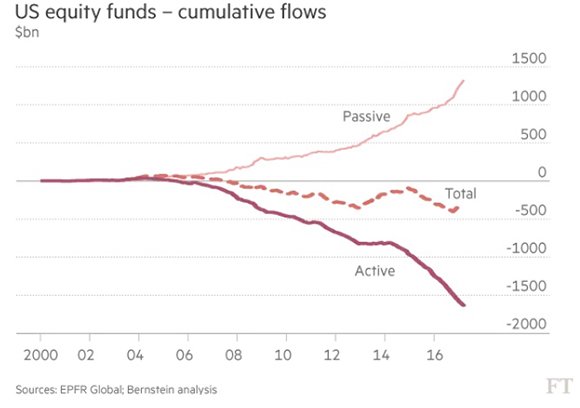

Those days are over. The rise of passive investing, via the popularity of low-cost index trackers and ETFs, is hitting active managers hard, to the point where their future is being questioned.

This is an unqualified good thing. For too long terrible managers have been paid too much to do an awful job. The AFR reported recently that, “the majority of Australian active funds in most categories fail to beat the index over three and five years”.

Investors are waking up to the fact they're being ripped off, especially by bank-run retail funds and active managers that can't deliver on their promises. Once you understand that a 2 per cent fee on a fund earning market returns of 6 per cent is a 33 per cent commission, an industry fund or index tracker with negligible fees and market returns seems rather attractive.

Genuine stockpickers have nothing to fear and much to gain from this trend. In the way that a rugby union player leaving to play league raises the intelligence of both codes, ridding the industry of dud active managers lifts the intelligence of the industry. If you're happy with market returns there are more cheaper options to get them. And investors seeking outperformance have more chance of finding it because there's less competition for cheap stocks.

It's all good in my view, except for the banks' iron grip on distribution in the sector, preying on unsuspecting clients that think Count Financial, Godfrey Pembroke and BT Financial are independent advisers. For a bit of weekend fun, check out Count's website and see if you can find the solitary mention of Commonwealth Bank, its owner. Or NAB on Pembroke's. There's a free consultation with one of their advisers up for grabs for the first correct entry.

I have no sympathy for the banks moaning about a new tax, especially when you consider this chart, via Macrobusiness.

That said, a genuine move to increase competition in the sector, as opposed to a Government-led attempt to skim money off the banks that the banks have skimmed from us, would be welcome. Forcing them to divest their financial planning arms and a level funding playing field would be a start. Bank account portability would be even better.

So please Ian, Andrew, Brian and Shayne, stop your whinging. If you're not on a bus to Trinco you have no idea how lucky you are.